The global commodity markets are entering what could be the most significant structural shift since the China-driven supercycle of the 2000s. But this time, the dynamics are fundamentally different, and the opportunity lies not in chasing individual metals, but in understanding how diversified commodity exposure can capture the multi-year trend while managing concentration risk.

Source - G&R

Table of Contents

- Understanding the Current Cycle

- The Case for Broad Commodity Index Exposure

- The Energy Complex: Next in Rotation?

- Risks and Considerations

- Investment Implications

- Conclusion: The Cycle Remains Intact

- About Paasa

Understanding the Current Cycle

Commodity supercycles are rare, multi-decade phenomena driven by structural demand shifts that outpace supply responses. Historically occurring every 50-70 years, these cycles are characterized by prolonged periods where prices trend upward despite temporary volatility. The last major supercycle, spanning 2000-2011, was fueled by rapid industrialization in China, India, and other emerging markets.

Today's emerging cycle is built on three distinct pillars:

1. The Energy Transition Imperative

The global shift toward decarbonization isn't a future possibility, it's happening now. Electric vehicle sales have exploded from near-zero in 2010 to over 50% of new car sales in China and 11.4% in the United States by 2024. Each EV requires approximately four times more copper than a traditional internal combustion vehicle. When you factor in charging infrastructure, grid modernization, and renewable energy installations, the metal intensity of our economy is fundamentally changing.

The International Energy Agency projects that demand for copper from energy transition applications alone could grow at a compound annual rate of 10.7% through 2034. This includes 14.3% growth from EVs, 9.3% from wind power, and 5.6% from solar installations. Compare this to traditional copper demand growing at just 1.4% annually.

2. The AI and Data Center Revolution

The artificial intelligence boom has created an unexpected commodity demand driver. Data centers, which are proliferating to support AI workloads, are extraordinarily metal-intensive. A single hyperscale data center can require thousands of tons of copper for wiring and cooling systems, along with significant amounts of aluminum for infrastructure.

BloombergNEF estimates that global copper demand is growing at seven times the rate of traditional industrial uses, with AI-related infrastructure being a primary catalyst. This demand vector emerged suddenly in 2022-2023 and shows no signs of slowing.

3. Supply Constraints and the 17-Year Problem

Perhaps most critically, the supply side of the equation is severely constrained. Bringing a new copper mine from exploration to production takes an average of 17 years. We're now facing the consequences of a decade of underinvestment in new mining capacity.

Between 2017 and 2022, mining companies prioritized debt reduction and shareholder returns over capital expenditure. Annual spending on new projects stalled even as dividends rose. The result: a capex shortfall that translates directly into a supply shortfall between 2025 and 2030.

Recent supply disruptions have only intensified the problem. Freeport-McMoRan's Grasberg mine in Indonesia (one of the world's largest copper producers) faced major operational issues in late 2025, forcing the company to declare force majeure and cut 2026 production guidance. First Quantum's Cobre Panama mine has been offline since November 2023 following the cancellation of its mining contract. These two operations alone previously supplied approximately 2% of global copper demand.

The Case for Broad Commodity Index Exposure

This brings us to a critical investment question: how do you capture this structural trend without taking on excessive concentration risk?

The Bloomberg Commodity Index Advantage

The Bloomberg Commodity Index (BCOM) offers a thoughtfully constructed approach to commodity exposure. Rather than betting exclusively on precious metals or a single commodity thesis, it provides diversified access across the entire commodity complex:

Current Index Composition (2025):

- Energy (Primary & Distillates): ~30%

- Precious Metals (Gold, Silver, Platinum, Palladium): Contributing significantly to 2025's 64% gain in this sector

- Industrial Metals (Copper, Aluminum, Zinc, Nickel): Up 13% in 2025

- Agriculture (Grains, Softs, Livestock): Mixed performance

- Natural Gas and other energy derivatives

Performance Context:

The index has delivered strong results in the early 2020s: +27.11% in 2021, +16.09% in 2022, -7.91% in 2023, and +5.38% in 2024. Through November 2025, the index was up approximately 9%, with precious metals driving much of the outperformance. This demonstrates the value of diversification—while energy and grains faced headwinds, metals more than compensated.

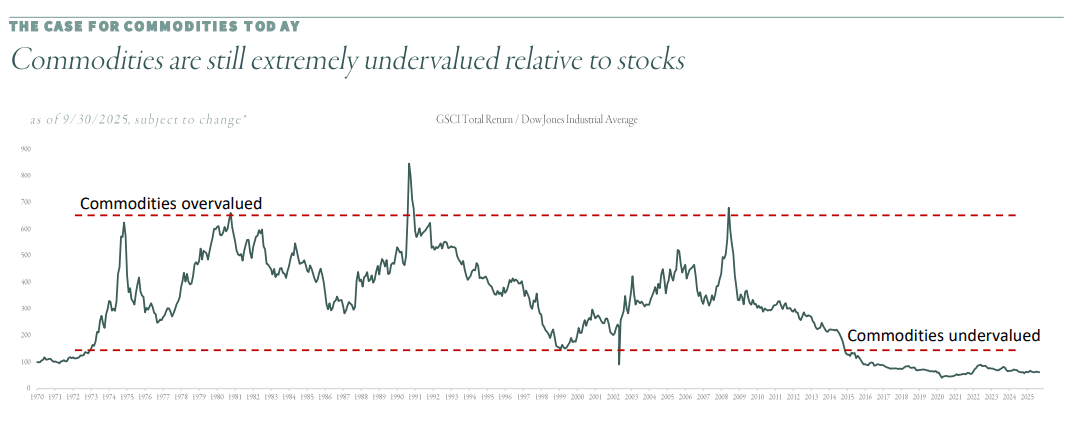

Why Diversification Matters: The Replicability Factor

Here's a contrarian but important point: higher commodity prices are rarely welcomed long-term. Apart from gold's unique status as a monetary safe haven, most industrial metals are ultimately replicable or substitutable.

Consider copper. While demand is surging, sustained high prices create powerful incentives for:

- Substitution: Engineers have already begun revisiting aluminum for certain wiring applications when copper trades at significant premiums

- Increased recycling: High prices draw more scrap material into circulation

- Innovation: Industries develop copper-light designs and alternative materials

- New supply: Marginal projects become economically viable at elevated prices

The same logic applies to silver, platinum, and other industrial metals. When prices surge too high for too long, markets respond.

This is why index exposure is superior to concentrated bets. The Bloomberg Commodity Index allows internal rotation;as capital flows from one commodity to another based on relative valuations and supply-demand dynamics, the index automatically captures these shifts.

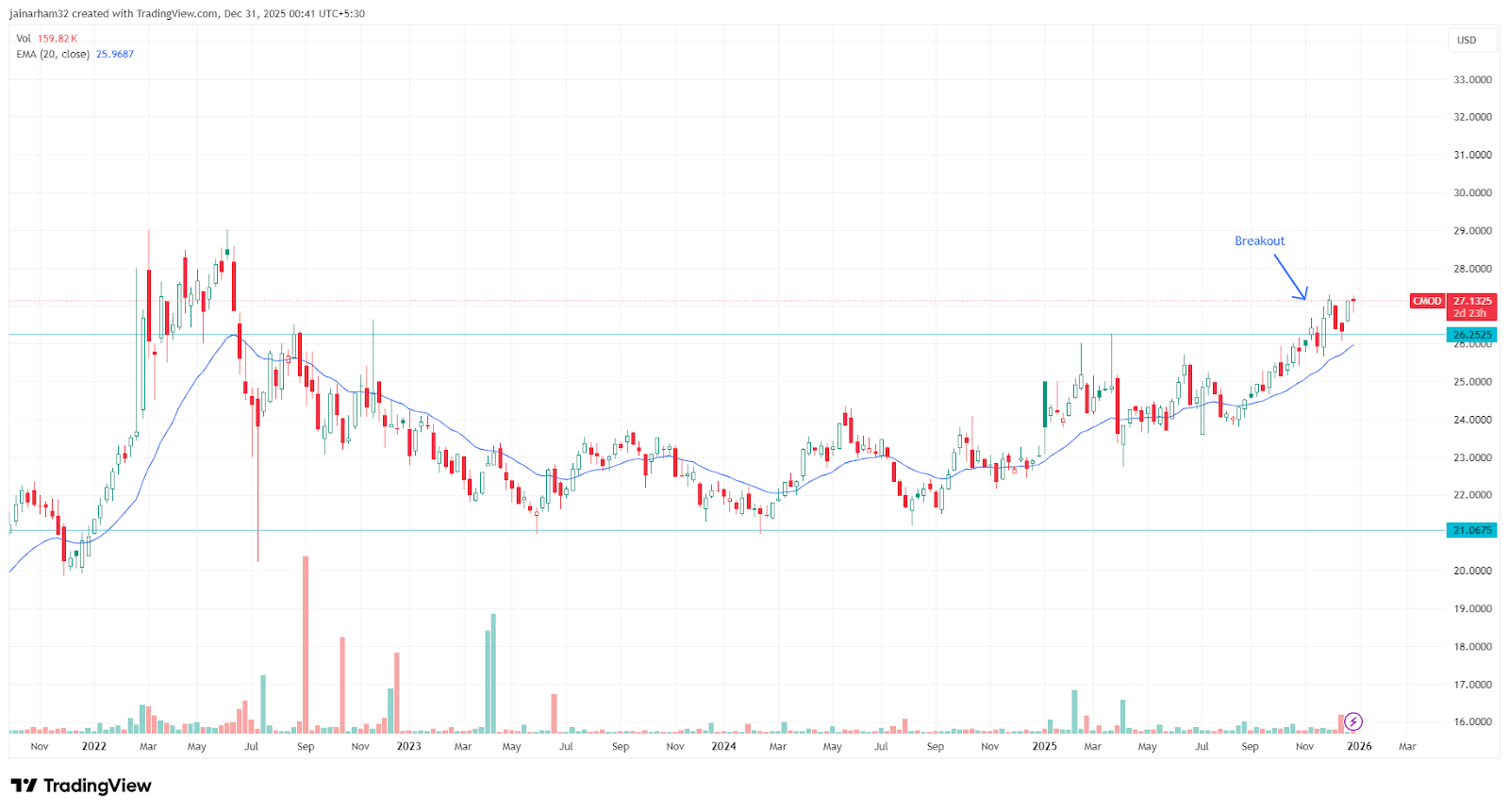

The Current Technical Setup

The technical picture is compelling. The Bloomberg Commodity Index has recently broken above its previous highs, suggesting the beginning of a new leg higher. Over the past 12 months through December 2025, the index has gained approximately 9.8%, with the 52-week range spanning from 96.13 to 112.83.

This pattern suggests we're in the early stages of a broader commodity re-rating. Historically, energy and base metals cycles can lag precious metals by 6-18 months. The next phase could see Brent crude and refined products rally while precious metals consolidate gains, exactly the kind of rotation an index captures naturally.

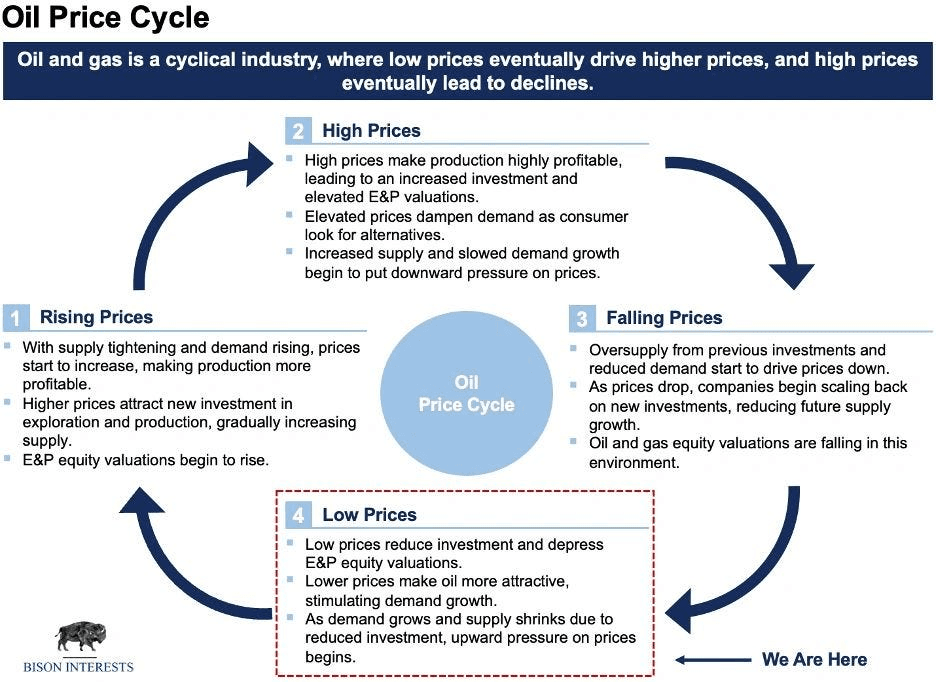

The Energy Complex: Next in Rotation?

Speaking of energy, there's a compelling case that Brent crude and energy products could be the next beneficiaries of the commodity cycle rotation. Current oil prices around $57-58 per barrel appear to discount significant demand weakness. Yet several factors could support a rebound:

Supply-Side Tightness: Despite concerns about oversupply, geopolitical risks remain elevated. Venezuela's situation, Middle East tensions, and OPEC+ production management all create potential for supply disruptions.

Inventory Dynamics: While crude inventories have been adequate, refined product inventories show more vulnerability, particularly for diesel and heating oil.

The Energy Transition Paradox: Ironically, the transition away from fossil fuels may create medium-term supply constraints. Underinvestment in new oil and gas projects, driven by ESG considerations, could lead to shortages before renewables fully scale.

The Bloomberg Commodity Index's energy weighting of approximately 30% means it's well-positioned to benefit if energy prices firm up in 2026. This is precisely the value of diversified exposure, you don't need to time the rotation perfectly.

Risks and Considerations

No investment thesis is without risks. For commodities in 2026, several factors warrant attention:

Macroeconomic Headwinds: Global GDP growth is projected at just 3.2% for 2026, a deceleration from prior years. Commodity demand responds to acceleration, not absolute levels. Slower growth could temper price gains.

China's Property Sector: Chinese residential real estate remains weak, with home prices expected to fall 3.7% in 2025 and continue declining into 2026. Historically, this sector has been a major copper consumer. However, China's pivot toward high-tech manufacturing, EVs, and grid infrastructure is providing an offset.

Trade Policy Uncertainty: Tariff threats, particularly from the United States, have created volatility. Copper prices spiked in 2025 partly due to traders rushing to import material ahead of potential tariffs. When refined copper was temporarily exempted, prices corrected sharply. This political risk layer adds complexity to fundamental analysis.

Investment Implications

For investors constructing portfolios for 2026 and beyond, several principles emerge:

1. Favor Index Exposure Over Single Commodities

Unless you have strong conviction and deep expertise in a specific commodity market, broad index exposure is the optimal approach. The Bloomberg Commodity Index provides:

- Diversification across 24 exchange-traded commodity contracts

- Automatic rebalancing based on liquidity and production data

- Protection against concentration risk in any single commodity

- Participation in sector rotation as the cycle evolves

2. Understand This Isn't "One Size Fits All"

The commodity space in 2026 won't see uniform gains. Performance will accrue to specific scarcity mechanisms:

- Gold as a reserve asset driven by central bank demand

- Silver as both a precious metal and supply-constrained industrial input

- Copper driven by energy transition fundamentals

- Uranium facing long-lead-time supply constraints

- Energy products experiencing regional divergences

An index captures these differentiated dynamics better than trying to pick winners individually.

3. Think in Multi-Year Time Horizons

If this is indeed a structural supercycle, it could extend well into the 2030s or even toward 2045. However, volatility will be significant. Corrections of 20-30% are likely even within a long-term bull market. The Bloomberg Commodity Index dropped 7.91% in 2023 despite the longer-term uptrend being intact.

Position sizing should reflect this volatility. For most portfolios, commodity exposure of 5-15% provides meaningful diversification without excessive risk.

4. Monitor the Rotation

Stay attuned to which commodities are leading and lagging. Right now, precious metals have led while energy has lagged. History suggests this could reverse. The beauty of index exposure is you don't need to time this perfectly, the index composition adjusts to reflect changing market dynamics.

Conclusion: The Cycle Remains Intact

The fundamental thesis for a multi-year commodity upcycle remains compelling. Supply constraints developed over a decade of underinvestment are colliding with structural demand growth from energy transition, AI infrastructure, and emerging market development.

However, the path forward won't be linear. We're not looking at the speculation-fueled frenzy of 2007-2008. Instead, expect a more measured advance punctuated by sector rotation, macroeconomic setbacks, and periodic consolidation.

As we discussed, the next run could come in Brent crude and other energy names while precious metals consolidate their 2025 gains. Or copper could surge again on supply disruptions. Or silver could explode on industrial demand.

The point is: you don't need to know which one. Let the index capture the cycle while managing the risks.

About Paasa

Paasa is the platform used by global Indian Investors, NRIs, and family offices to diversify their wealth across global markets using equities, commodities, UCITS ETFs, are more. What sets Paasa apart is its India-facing compliance layer:

- FEMA and LRS compliance embedded into every transaction.

- Tax reporting and analytics built for Indian investors (LTCG, STCG, dividend tax, TCS tracking).

- End-to-end support for remittance structuring, reconciliation, and compliance queries.

Whether it’s commodities, equities, UCITS funds, managed strategies, or even helping you protect your RSUs from estate tax, Paasa provides a single transparent platform for global portfolios with the confidence that India-specific compliance is taken care of.

Disclaimer

This article is intended for information only and does not constitute investment, tax, or legal advice. The material is based on public sources and our interpretation of current regulations, which may change. Investing in global markets entails risks, including currency risk, political risk, and market volatility. Past performance does not predict future outcomes. Please seek advice from qualified financial, tax, and legal professionals before acting.