Investors who hold (or are looking to invest in) US stocks or ETFs often overlook one critical risk: the US Estate Tax. US-situated assets exceeding $60,000 are subject to an inheritance tax of up to 40% upon the owner's death.

For example, if you have $200,000 in US stocks and ETFs, the IRS will charge a $36,000 tax upon your death.

UCITS ETFs solve this by offering US market exposure through a European domicile (Ireland or Luxembourg), which legally exempts them from US estate taxes.

Beyond asset protection, they offer superior tax efficiency: "Accumulating" UCITS funds reinvest dividends internally rather than distributing them, and are subject to lower withholding taxes. This structure avoids immediate taxation in India, allowing your capital to compound uninterrupted until you decide to sell.

This guide explains how UCITS work and how Indians can invest in UCITS while remaining compliant with tax regulations.

Table of contents

- What are UCITS ETFs?

- Are UCITS ETFs as liquid as US ETFs?

- Why are Indian investors choosing UCITS ETFs?

- Top UCITS ETFs by Category

- Why Indian professionals from MAANG are opting for UCITS

- Invest in UCITS ETFs with Paasa

- Conclusion

- Frequently Asked Questions

What are UCITS ETFs?

UCITS (Undertakings for Collective Investment in Transferable Securities) are investment funds that comply with EU (European Union) regulations and therefore can be traded across the EU.

A UCITS ETF is an Exchange Traded Fund (ETF) that is domiciled in Europe and strictly adheres to these UCITS regulations. While these funds are legally based in Europe (typically Ireland or Luxembourg), they are often used to invest in global assets, including US stocks like the S&P 500 or Nasdaq 100.

An ETF (Exchange Traded Fund) is a basket of securities (like stocks or bonds) that you can buy and sell on a stock exchange, just like a single share.

Are UCITS ETFs as liquid as US ETFs?

Yes. UCITS ETFs are highly liquid and function almost identically to their US counterparts.

Here is why you can buy and sell them instantly:

- Mandatory Liquidity: By EU law, all UCITS funds must be open-ended. This guarantees that you have the legal right to redeem your money at any time.

- Institutional Volume: Major funds managed by giants like BlackRock (iShares) or Vanguard trade billions of dollars daily on the London Stock Exchange (LSE).

- Instant Execution: Just like in the US, professional market makers operate continuously to ensure there is always a buyer or seller. This allows you to enter and exit positions instantly during market hours with tight spreads.

Paasa helps you buy and sell UCITS instantly and provides tax compliance support.

Why are Indian investors choosing UCITS ETFs?

Indian investors are shifting to UCITS ETFs not just for access to global markets, but for advantages that directly impact net returns.

1. Safeguarding against the US Estate Tax

This is the primary driver for Indian investors. If you hold US-domiciled assets (like US-listed stocks or ETFs) worth more than $60,000, you are subject to up to 40% US Estate Tax upon your death.

Since UCITS funds are legally domiciled in Europe (typically Ireland), they are not considered US-situated assets. This completely exempts your portfolio from the US estate tax risk, ensuring your wealth is passed on intact.

Use our US Estate Tax Calculator to find the exact tax you will have to pay.

2. Tax deferral via accumulating structures

US-listed ETFs distribute dividends to shareholders. For an Indian investor, this payout triggers a taxable event every quarter, taxed at your income slab rate.

UCITS ETFs offer "Accumulating" classes. These funds automatically reinvest dividends internally without paying them out. This prevents a taxable event in India, allowing your capital to compound tax-free until you eventually sell the ETF.

3. Lower withholding tax

US ETFs deduct a 25% withholding tax on dividends before paying you.

However, Ireland domiciled ETFs only have a 15% withholding tax at the fund level, leading to better compounding and growth.

Example: Consider an Indian investor who wants exposure to the S&P 500. Here is the difference between buying the standard US ETF versus its Irish equivalent.

Option A: The US ETF (e.g., SPY)

- Estate Tax: You are exposed to the US Estate Tax on assets above $60,000.

- Distributing class of dividends: Dividends are distributed, leading to taxation in India.

- High Dividends WHT: Withholding tax of 25%.

Option B: The UCITS ETF (e.g., CSPX)

- Estate Tax: You are exempt from US Estate Tax.

- Accumulating class of dividends: Dividends are reinvested into the fund, no tax liabilities are triggered.

- Low Dividends WHT: 15% withholding tax.

For a deep dive into the advantages of UCITS, read our guide on Why Indian Investors Should Choose UCITS Over US ETFs.

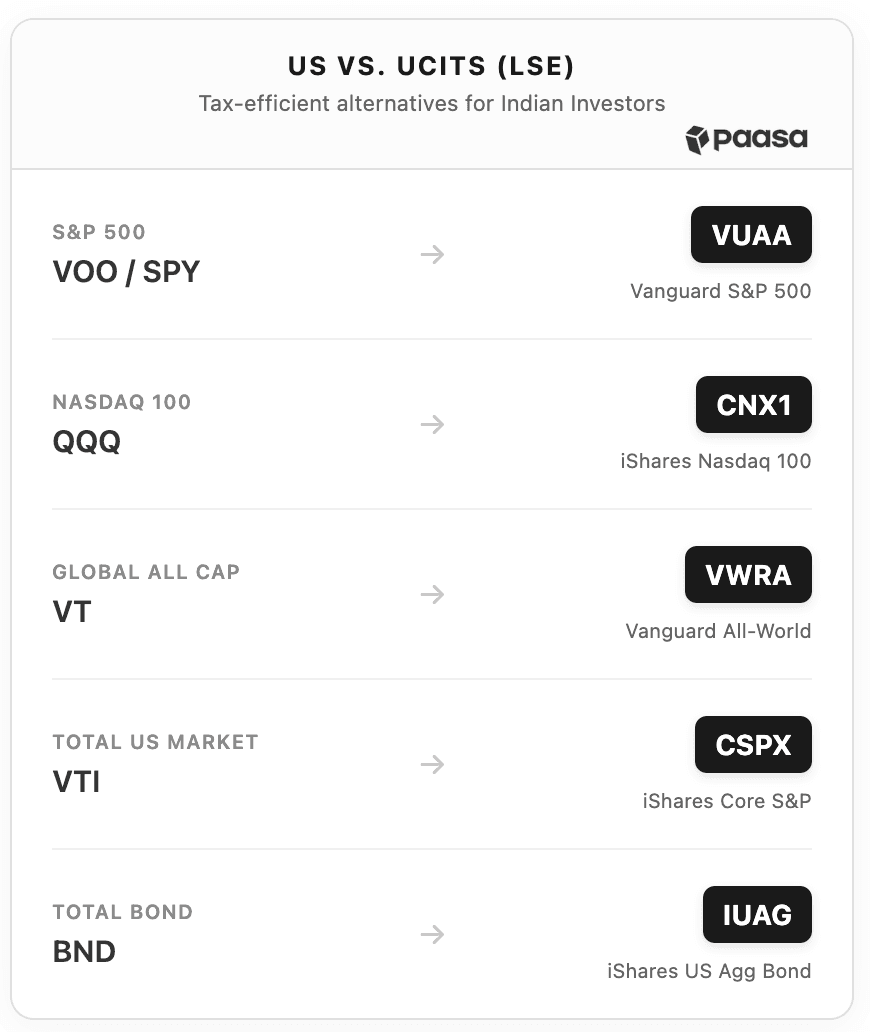

Top UCITS ETFs by Category

Here is a curated list of the most popular Accumulating (Acc) UCITS ETFs available to Indian investors.

These funds are domiciled in Ireland, exempt from US Estate Tax, and automatically reinvest dividends to defer taxes in India.

Category | Ticker (LSE) | Fund Name |

S&P 500 | VUAA | Vanguard S&P 500 UCITS ETF (Acc) |

CSPX | iShares Core S&P 500 UCITS ETF (Acc) | |

SPXS | Invesco S&P 500 UCITS ETF (Acc) | |

Nasdaq 100 | CNX1 | iShares Nasdaq 100 UCITS ETF (Acc) |

EQAC | Invesco Nasdaq-100 UCITS ETF (Acc) | |

Global Equities | VWRA | Vanguard FTSE All-World UCITS ETF (Acc) |

SSAC | iShares MSCI ACWI UCITS ETF (Acc) | |

Developed Markets | SWDA | iShares Core MSCI World UCITS ETF (Acc) |

VHVE | Vanguard FTSE Developed World UCITS ETF (Acc) | |

Emerging Markets | EIMI | iShares Core MSCI EM IMI UCITS ETF (Acc) |

XMME | Xtrackers MSCI Emerging Markets UCITS ETF (Acc) | |

Technology | IITU | iShares S&P 500 Info Tech Sector UCITS ETF (Acc) |

XDWT | Xtrackers MSCI World Information Tech UCITS ETF (Acc) | |

Semiconductors | SMH | VanEck Semiconductor UCITS ETF (Acc) |

SEMI | iShares MSCI Global Semiconductors UCITS ETF (Acc) | |

Artificial Intelligence | XAIX | Xtrackers Artificial Intelligence & Big Data UCITS ETF |

AIAI | L&G Artificial Intelligence UCITS ETF | |

Healthcare | IUHC | iShares S&P 500 Health Care Sector UCITS ETF (Acc) |

XDWH | Xtrackers MSCI World Health Care UCITS ETF (Acc) | |

Financials | IUFS | iShares S&P 500 Financials Sector UCITS ETF (Acc) |

XDWF | Xtrackers MSCI World Financials UCITS ETF (Acc) | |

China Exposure | ICHN | iShares MSCI China UCITS ETF (Acc) |

XCS6 | Xtrackers MSCI China UCITS ETF (Acc) | |

Japan Exposure | IJPA | iShares Core MSCI Japan IMI UCITS ETF (Acc) |

VJPN | Vanguard FTSE Japan UCITS ETF (Acc) | |

Global Small Cap | WSML | iShares MSCI World Small Cap UCITS ETF (Acc) |

WLDS | SPDR MSCI World Small Cap UCITS ETF (Acc) | |

Real Estate (REITs) | IPRP | iShares Developed Markets Property Yield UCITS ETF (Acc) |

DPYA | iShares Asia Property Yield UCITS ETF (Acc) | |

Gold | SGLD | Invesco Physical Gold ETC |

IGLN | iShares Physical Gold ETC | |

Commodities | ICOM | iShares Diversified Commodity Swap UCITS ETF (Acc) |

CMOD | Invesco Bloomberg Commodity UCITS ETF (Acc) | |

Global Bonds | AGGG | iShares Core Global Aggregate Bond UCITS ETF (Acc) |

VAGU | Vanguard Global Aggregate Bond UCITS ETF (Acc) |

Pro Tip: Look for "(Acc)" in the name. This stands for "Accumulating," meaning the fund recycles your dividends to buy more shares for you, keeping your tax bill at zero until you sell.

Dividend paying UCITS ETFs have a withholding tax 15%. But accumulating UCITS ETFs do not pay dividends, and therefore create no tax liabilities. This leads to the following advantages:

- No Tax Event: Since you receive no cash, you pay zero tax in India annually.

- Compounding: The money that would have gone to the taxman stays in the fund and grows.

- Lower Final Rate: When you eventually sell (after 24 months), the profit is taxed as Long Term Capital Gains (12.5%).

For a deeper dive into accumulating vs. distributing UCITS ETFs, visit UCITS ETFs: Accumulating vs Distributing.

Common Questions

Which provides a lower dividend withholding tax: US ETFs or UCITS ETFs?

Irish-domiciled UCITS ETFs are more efficient, incurring only a 15% withholding tax due to the US-Ireland treaty, compared to the 25% tax deducted immediately by US ETFs. Furthermore, accumulating UCITS reinvest these dividends, avoiding immediate Indian income tax and allowing the capital to compound tax-free until you sell.

Do I need to convert INR to Euro to buy UCITS ETFs?

No. Even though these funds are domiciled in Ireland, they trade on the London Stock Exchange (LSE) in US Dollars (USD). When you use Paasa, you remit funds in USD just like you would for a standard US brokerage account. There is no double currency conversion.

Are UCITS ETFs more expensive than US ETFs?

Slightly, but the tax savings far outweigh the cost. For example, a standard US S&P 500 ETF might charge 0.03% per year, while a UCITS equivalent might charge 0.07%. However, by avoiding the 25% dividend tax drag every year and eliminating the 40% estate tax risk, the slight difference in expense ratio is negligible compared to the massive value in tax efficiency.

Why Indian professionals from MAANG are opting for UCITS

For many tech professionals in India (working at companies like Google, Microsoft, or Amazon), a significant portion of their net worth is tied up in Restricted Stock Units (RSUs).

While RSUs are a great wealth generator, keeping them held in your US brokerage account creates two major risks:

- Concentration Risk: Your salary and your savings are tied to the performance of a single company. If the company struggles, you risk losing both your income growth and your asset value.

- Estate Tax Risk: Since RSUs are US-situs assets, holdings above $60,000 are subject to up to 40% US Estate Tax.

That is why many Indian tech professionals are reinvesting their RSU wealth into UCITS ETFs.

For in-depth information, visit our guides on How Indian professionals can protect RSUs from estate tax and UCITS ETFs vs US ETFs for RSUs.

Common Questions

Can I directly convert my US RSUs into UCITS ETFs?

No. You cannot "swap" a US stock (like Google or Amazon) for a UCITS ETF unit directly. You must first sell your vested RSUs to generate cash, and then use that cash to buy the UCITS ETF.

Pro Tip: You can transfer your existing RSUs from your employer’s broker (e.g., Fidelity, E*TRADE, Schwab) to Paasa via ACATS (a free, digital transfer process) and then execute the sell/buy strategy all within one platform.

Do I need to bring the money back to India before reinvesting?

No. Under RBI regulations (Overseas Portfolio Investment), if you sell a foreign asset (like RSUs), you are allowed to reinvest the proceeds into another foreign asset (like UCITS ETFs) without repatriating the funds to India, provided the reinvestment happens within 180 days of the sale. This saves you significant money on Forex conversion fees and transfer charges.

Invest in UCITS ETFs with Paasa

Indian residents can invest in UCITS ETFs under the RBI’s Liberalised Remittance Scheme (LRS), which allows you to remit up to $250,000 per financial year overseas for permitted investments.

Paasa is currently the only India-facing platform that offers UCITS access with end-to-end handling of FEMA compliance, INR remittance tracking, and tax-ready reporting, removing the operational burden from the investor.

Paasa also offers you the best FX rates, ensuring that your returns are not eaten up by platform fees.

Use our UCITS Screener to discover and compare UCITS-compliant investment instruments.

Conclusion

For Indian investors, UCITS ETFs are the optimal structure for US market exposure. By choosing Irish-domiciled accumulating funds, you effectively immunize your portfolio against the 40% US Estate Tax while deferring dividend taxes to maximize compounding.

About Paasa

Paasa is an Indian investor’s gateway to global investing, trusted by HNIs, family offices, and institutions to diversify into markets across the US, Europe, China, Japan, and beyond.

What sets Paasa apart is its India-facing compliance layer:

- FEMA and LRS compliance embedded into every transaction.

- Tax reporting and analytics built for Indian investors (LTCG, STCG, dividend tax, TCS tracking).

- End-to-end support for remittance structuring, reconciliation, and compliance queries.

Whether it’s equities, ETFs, UCITS funds, managed strategies, or even helping you protect your RSUs from estate tax, Paasa provides a single transparent platform for global portfolios with the confidence that India-specific compliance is taken care of.

Disclaimer

This blog is for educational purposes only and should not be construed as tax, legal, or investment advice. RSU taxation, estate tax exposure, and cross-border investment rules are subject to change and may vary based on your personal circumstances.

Investing in global markets involves risks, including currency risk and market volatility. UCITS ETFs, RSUs, and other securities referenced here are used for illustration and do not constitute recommendations. Past performance is not indicative of future results.