The United Kingdom is home to several leading blue-chip companies, including Unilever, BP, HSBC, Shell, and Diageo.

For Indian investors looking beyond, the UK offers something different: a mature and transparent market that values discipline and dependable yield. It is one of the few markets where long-term investing still means patience, dividends, and trust in fundamentals, rather than speculation.

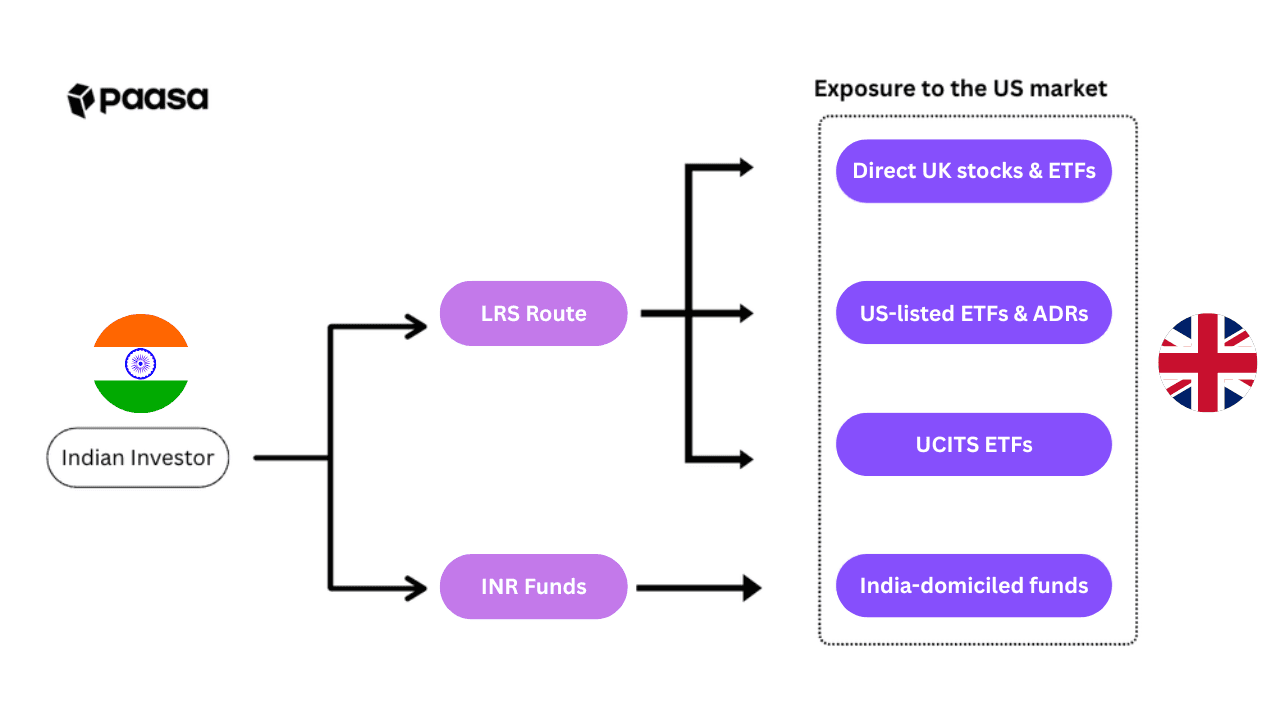

This guide outlines how Indians can invest in the UK stock market, the available routes under RBI’s Liberalised Remittance Scheme (LRS), and practical ways to build exposure through LSE-listed stocks, ETFs, REITs, and ADRs.

Table of contents

- Can Indians invest in the UK directly?

- Directly buy London-listed stocks

- US-listed UK ETFs & ADRs

- UCITS ETFs with UK exposure (Europe-listed)

- India-domiciled funds & ETFs with UK exposure

- Taxation: How Your Returns Are Treated in India

- Why consider investing in London?

- Platforms that help Indians invest in London

- Conclusion

- FAQs

Can Indians invest in the UK directly?

Yes. Indians can invest directly in London Stock Exchange (LSE)–listed stocks, ETFs, and REITs through the Liberalised Remittance Scheme (LRS), which allows up to USD 250,000 per person per financial year to be invested abroad.

The simplest route is to use a global brokerage platform that supports trading on the London Stock Exchange, such as Paasa or Interactive Brokers (IBKR). These platforms handle all compliance under LRS and let you invest in companies like Unilever, HSBC, Shell, BP, or AstraZeneca, all part of the FTSE 100 index.

This means an Indian investor can open an account with a global broker like Paasa, remit funds abroad using the correct purpose code for equity investment, and legally purchase London-listed equities, ETFs, or REITs.

The four practical routes to gain exposure to the UK market are:

- Directly buy London-listed stocks

- US-listed UK ETFs & ADRs

- UCITS ETFs with UK exposure (LSE / Xetra / Euronext)

- India-domiciled funds & ETFs with UK exposure

Important to know:

- The annual LRS limit is USD 250,000 per individual.

- Remittances above ₹10 lakh per financial year attract TCS (Tax Collected at Source), tracked PAN-wise and collected by your bank when you remit.

- All foreign assets must be disclosed in your Indian Income Tax Return (ITR) under the foreign-asset schedule.

Directly buy London-listed stocks

The London Stock Exchange (LSE) is the UK’s primary stock market, and includes blue-chip companies like Unilever, HSBC, BP, Shell, AstraZeneca, and Diageo. Indian investors can use global brokers like Paasa or IBKR under the RBI’s LRS to buy UK-listed equities directly in British pounds.

Key points:

- Dividends: The UK does not levy withholding tax on dividends paid by UK-resident companies to non-residents.

- Capital gains: Non-residents are not liable for UK capital gains tax on disposals of listed shares. Gains are taxable only in India as short- or long-term capital gains depending on the holding period.

- Currency: Shares trade in British pounds (GBP), providing diversification from INR and USD exposure.

- Stamp Duty: Most direct share purchases attract a 0.5% Stamp Duty Reserve Tax (SDRT). This is a transaction tax charged when shares are bought electronically through the London Stock Exchange. ETFs listed on the LSE are exempt from this levy.

- Compliance: Investments must be funded under the LRS limit of USD 250,000 per individual per financial year using the correct purpose code for equity investment abroad.

Pros:

- Direct ownership of UK blue-chip companies.

- No dividend withholding on regular equities and no UK capital gains tax for non-residents.

- Strong governance and transparent settlement under the Financial Conduct Authority (FCA), the UK’s financial regulator overseeing markets and investor protection.

- Fully compliant and recognised under FEMA / LRS.

Cons:

- A 0.5 % stamp duty applies on most share purchases.

- Liquidity can be lower in mid-cap or niche REIT counters compared to US markets.

US-listed UK ETFs & ADRs

Another practical way for Indian investors to gain exposure to UK equities is through ETFs and ADRs listed in the United States.

US-listed UK ETFs track the performance of the British equity market while trading on American exchanges such as the NYSE or Nasdaq. The most popular examples include the iShares MSCI United Kingdom ETF (EWU) and the Franklin FTSE United Kingdom ETF (FLGB), which provide exposure to large and mid-cap UK companies across sectors such as banking, energy, consumer goods, and healthcare.

ADRs (American Depositary Receipts) represent shares of UK-based companies traded in the United States. These instruments give indirect access to the UK’s largest corporates, such as AstraZeneca (AZN), Unilever (UL), BP (BP), HSBC (HSBC), and Diageo (DEO), without trading directly on the London Stock Exchange or converting INR to GBP.

For Indian investors, US-listed ETFs and ADRs offer a simple, liquid, and USD-denominated way to participate in the UK market under the Liberalised Remittance Scheme (LRS).

Popular examples include:

ETFs:

- iShares MSCI United Kingdom ETF (EWU)

- Franklin FTSE United Kingdom ETF (FLGB)

ADRs:

- Unilever (UL)

- HSBC (HSBC)

- Shell (SHEL)

Key points:

- Regulation: US-domiciled ETFs and ADRs are regulated by the U.S. Securities and Exchange Commission (SEC) and trade in USD on major American exchanges.

- Accessibility: Available through most global brokerage platforms such as Paasa, Interactive Brokers (IBKR), or Vested; no need for GBP accounts or LSE access.

- Dividends: Subject to 30% U.S. withholding tax, reduced to 25% for Indian residents under the India–U.S. Double Taxation Avoidance Agreement (DTAA) when the W-8BEN form is submitted.

- Capital gains: Not taxed in the U.S. for non-resident investors; taxable in India as short-term or long-term capital gains depending on the holding period.

- Currency: All trades, dividends, and settlements occur in USD, simplifying cross-border management.

Pros:

- High liquidity and global recognition on U.S. exchanges.

- Simplified access for Indian investors already participating in U.S. markets.

- ETF diversification, covering broad UK indices without direct LSE exposure.

Cons:

- 25% dividend withholding tax reduces effective yields.

- Expense ratios of ETFs slightly lower net returns over time.

- Indirect exposure: Some funds may underrepresent mid-cap or REIT components of the UK market.

UCITS ETFs with UK exposure (Europe-listed)

Another practical way for Indians to gain exposure to the UK market is through UCITS (Undertakings for Collective Investment in Transferable Securities) ETFs domiciled in Ireland or Luxembourg.

UCITS ETFs are Europe-domiciled funds that allow investors to access international equities while being regulated under the UCITS framework. They trade on major exchanges such as the London Stock Exchange (LSE), Xetra (Germany), and Euronext (France/Amsterdam), and are designed specifically for global investors seeking diversified, tax-efficient exposure.

For Indian investors, UCITS ETFs are often the cleanest and most tax-efficient way to invest in UK equities.

They sidestep U.S. estate tax, automatically handle underlying UK dividend taxation within the fund, and provide broad exposure through single-country UK ETFs or regional Europe-focused portfolios that include British blue chips.

Popular examples include:

- Vanguard FTSE 100 UCITS ETF (VUKE) – tracks the FTSE 100 Index; GBP and USD share classes available.

- iShares Core FTSE 100 UCITS ETF (ISF) – one of the most liquid UK ETFs listed on LSE and Xetra.

- SPDR FTSE UK All Share UCITS ETF (SPUK) – provides broader exposure across large, mid, and small-cap UK stocks.

To understand why UCITS funds can be a smarter choice for Indian investors, read our detailed guide: Why UCITS Funds Work for Indian Investors

Key points:

- Domicile and regulation: Typically domiciled in Ireland or Luxembourg, regulated under the UCITS Directive, and listed on LSE/Xetra/Euronext in USD, GBP, or EUR.

- Availability on Paasa: UCITS ETFs are accessible under the RBI’s LRS via Paasa, with seamless onboarding, consolidated reporting, and custody under top-tier European exchanges.

- Underlying UK dividends: The UK does not impose withholding tax on most company dividends. Any withholding from REIT income is handled inside the ETF, not at the investor level.

- Tax in India: Dividends received from UCITS ETFs are taxable at the investor’s slab rate, while capital gains are taxed in India based on the holding period (short-term or long-term).

- Estate tax: No U.S. estate-tax exposure, since UCITS ETFs are EU-domiciled, not U.S.-situs assets.

Pros:

- Tax efficiency: UCITS structures avoid U.S. estate tax and minimise withholding tax drag.

- Broad availability: Major issuers like iShares, Vanguard, and SPDR offer UK-specific UCITS ETFs.

- Regulatory credibility: UCITS funds follow strict EU investor-protection standards.

Cons:

- Accessibility: Platforms like INDmoney and Vested currently focus on U.S. markets and don’t provide direct access to European-listed UCITS ETFs. Paasa, on the other hand, enables Indian investors to invest in UCITS ETFs with full compliance and consolidated reporting.

- Liquidity: On-exchange liquidity can be lower than U.S.-listed ETFs, especially on Xetra and Euronext.

- Currency exposure: UCITS ETFs trade in GBP, USD, or EUR, so FX fluctuations can influence returns.

India-domiciled funds & ETFs with UK exposure

A fourth route for Indians to gain exposure to the UK market is through India-domiciled international mutual funds and ETFs that invest in overseas master funds holding UK or Europe-listed equities. These schemes are SEBI-regulated and denominated in INR, meaning investors can participate without using the RBI’s Liberalised Remittance Scheme (LRS).

The Indian Asset Management Company (AMC) collects investments in rupees and channels them to a foreign “feeder” or “master” fund, which then invests in underlying UK or European securities.

For many investors, this is the simplest, fully domestic route to participate in developed-market equities while remaining within India’s regulatory system.

Popular examples include:

- Edelweiss Greater Europe Offshore Fund – invests in the JPMorgan Funds – Europe Dynamic Fund (includes large UK exposure).

- ICICI Prudential Global Stable Equity Fund – feeder fund investing in a global portfolio with meaningful allocations to UK companies.

- Nippon India ETF Hang Seng BeES and similar regional funds – provide partial UK exposure through diversified Asia-Europe holdings.

Key points:

- Structure: SEBI-registered feeder or fund-of-fund schemes that invest in overseas master funds under RBI’s overseas investment limits for AMCs.

- Currency: Investors subscribe and redeem in INR; the AMC manages all FX conversion and cross-border compliance internally.

- Taxation: Returns are taxed in India as domestic mutual funds—capital gains depend on holding period (long-term > 36 months = 20 % with indexation; short-term = slab rate). Dividends, if any, are taxed at slab rate.

- Convenience: No LRS paperwork, no foreign-broker account, and eligibility for SIP/STP investment modes.

- Exposure: Underlying allocation to the UK may vary by fund—most “Europe” or “Global” schemes typically hold 15–40 % in UK equities.

Pros:

- No LRS remittance or foreign-broker setup required.

- Rupee-denominated; easier tax reporting and SIP flexibility.

- SEBI oversight and Indian investor-protection framework.

Cons:

- Indirect exposure: Fund managers allocate dynamically; UK weighting may change over time.

- Higher expense ratios due to dual management layers (domestic + master fund).

Taxation: How Your Returns Are Treated in India

When investing in the UK from India, returns are subject to two layers of taxation: Foreign-side taxes, which include any withholding or capital gains taxes levied by the UK (or the fund’s domicile country), and Indian taxation, which is the final tax liability when filing the Income Tax Return (ITR) in India.

This structured comparison breaks down the tax and estate implications across the four practical routes available to Indian investors.

For how the double tax treaty taxes dividends, interest, and gains, read India–UK DTAA.

Foreign-side taxes

Route | Asset Domicile | Dividend WHT at Source (Foreign) | Capital Gains Tax at Source | Estate Tax Exposure |

Direct LSE stocks | United Kingdom | 0% (UK generally does not withhold tax on dividends paid to non-resident shareholders) | None (0%) for non-residents on disposals of ordinary listed shares | Yes. UK Inheritance Tax (IHT) applies to UK-situs assets above the nil-rate band of £325,000 |

US-listed UK ETFs & ADRs | United States | ETFs: 25% WHT on dividends for Indian residents with W-8BEN (otherwise 30%).

ADRs: typically 0% US WHT on pass-through foreign dividends; depositary fees may apply | None for non-resident aliens (US does not tax capital gains on marketable securities in most cases) | |

UCITS ETFs with UK exposure (LSE / Xetra / Euronext) | Ireland / Luxembourg | 0% Irish/Lux WHT on fund distributions to properly documented non-residents; any underlying UK WHT is handled inside the fund | None at source (no Irish/Lux CGT for non-resident investors on fund disposals/redemptions, subject to standard declarations) | None. EU-domiciled (no US estate tax; not UK-situs) |

India-domiciled funds / FoFs with UK exposure | India | None at investor level (any foreign WHT is handled within the scheme; not withheld from the unitholder) | None at foreign source (units are redeemed in India; India-side rules apply) | None abroad (units are domestic Indian assets) |

Indian Taxation and Compliance

Assuming the investor is a resident individual in India (FY 2025–26 rules):

Route | Dividend/Distribution Income (India) | Capital Gains (Sale in India) | Foreign Tax Credit (FTC) |

Direct LSE Stocks | Fully taxable in India under “Income from Other Sources” at your individual slab rate. | STCG: slab (if held ≤ 24 months).

LTCG: 12.5% (no indexation) if held > 24 months. | Not applicable (0% UK WHT). |

US-listed ETFs/ADRs | Taxable in India under “Income from Other Sources” at your applicable income-tax slab rate.

U.S. payer withholds 25% after submission of Form W-8BEN (India-U.S. tax treaty, Article 10); 30 % if the form is not filed. | STCG: slab (if held ≤ 24 months).

LTCG: 12.5% (no indexation) if held > 24 months. | FTC available for the 25% US WHT; file Form 67 on time to claim. |

UCITS ETFs (Accumulating Class) | None received (dividends are automatically reinvested inside the fund). Tax arises on sale. | STCG/LTCG same as above (12.5% LTCG if > 24 months; STCG slab). | No FTC, as Ireland/Luxembourg UCITS funds do not levy withholding tax on reinvested income or capital gains. |

India-domiciled Funds | • Taxed at your income-tax slab rate.

• AMC deducts 10 % TDS if total dividends exceed ₹5,000 per FY | All gains taxed at slab rate (treated as short-term) since most global / international schemes qualify as Specified Mutual Funds under post-July 2024 rules. | No FTC (Foreign tax is adjusted at the fund level, not visible to the investor). |

Why consider investing in the UK?

Dividend market

The UK is known for its dividend-paying culture. Companies like Unilever, BP, HSBC, Shell, and Diageo maintain steady payout ratios, with yields often in the 3–5% range.

Stability

The UK operates under a strong regulatory framework led by the Financial Conduct Authority (FCA), with transparent corporate governance and low political risk.

Tax clarity

Non-residents face no UK capital gains tax on listed shares and 0% dividend withholding on most company payouts.

Global access

London remains a global financial hub, offering access to world-class companies, ETFs, and currency exposure through the British pound (GBP).

For Indians

A mature, income-oriented developed market that complements high-growth Indian portfolios with steady dividends and diversification.

Platforms that help Indians invest in the UK

There are multiple platforms through which Indian investors can access UK-listed stocks, ETFs, and REITs. Some provide direct trading access to the London Stock Exchange (LSE), while others offer indirect exposure via US-listed ETFs/ADRs or UCITS ETFs listed in Europe. Below is a comparison of the leading options available to Indian investors.

Direct access to London Stock Exchange (LSE) | ✅ | ✅ | ❌ | ❌ | ✅ | ❌ | ❌ |

UCITS ETFs (LSE / Xetra / Euronext) | ✅ | ✅ | ❌ | ❌ | ❌ | ❌ | ❌ |

US-listed UK ETFs & ADRs | ✅ | ✅ | ✅ | ✅ | ✅ | ❌ | ❌ |

ADRs of UK Companies | ✅ | ✅ | ✅ | ✅ | ✅ | ❌ | ❌ |

India-domiciled funds & ETFs with UK exposure | ✅ | ❌ | ✅ | ❌ | ❌ | ✅ | ✅ |

FEMA compliance support | ✅ | ❌ | ❌ | ❌ | ❌ | ❌ | ❌ |

Tax reporting support | ✅ | ❌ | ❌ | ❌ | ❌ | ❌ | ❌ |

INR-based analytics | ✅ | ❌ | ❌ | ❌ | ❌ | ❌ | ❌ |

Conclusion

For Indian investors, the United Kingdom offers a combination of stability, income, and global credibility. It brings together the reliability of a developed economy, deep and liquid markets, and a long tradition of consistent dividend payouts and transparent governance. From blue-chip names such as Unilever, BP, and HSBC to diversified opportunities through UCITS funds and ETFs, the UK remains a steady destination for long-term, income-focused portfolios.

Investing in the UK has also become simpler than ever. Whether through London Stock Exchange listings, UCITS ETFs, US-listed ADRs, or India-domiciled international funds, each route is clearly defined and fully compliant under RBI’s Liberalised Remittance Scheme (LRS). The key is choosing an approach that fits your goals while balancing tax efficiency, currency exposure, and ease of management.

Paasa helps investors do this seamlessly. With end-to-end FEMA compliance, tax-ready INR reporting, and a platform designed to combine global access with India-specific regulation, Paasa makes investing across the UK and Europe both effortless and compliant.

About Paasa

Paasa is India’s bridge to global investing. It is used by HNIs, family offices, and institutions to diversify across markets in the US, Europe, China, Japan, and beyond.

What makes Paasa different is its India-facing compliance layer that operates behind every transaction:

- FEMA and LRS rules are built in, ensuring that all cross-border investments remain compliant.

- Tax reports and analytics are tailored for Indian investors, covering LTCG, STCG, dividend tax, and TCS tracking.

- Remittance support and reconciliation are handled end to end, with dedicated help for compliance questions.

From global equities and ETFs to UCITS funds, managed portfolios, and RSU estate planning, Paasa provides one transparent platform that helps investors build international portfolios while staying compliant in India.

Relevant Reads

Compare routes, costs, and taxes across markets with these quick reads.

- Invest in US from India

- Invest in Ireland from India

- Invest in Switzerland from India

- Invest in China from India

- Invest in Japan from India

- Invest in Singapore from India

- Invest in Poland from India

- Invest in Germany from India

Disclaimer

This blog is for informational purposes only and should not be construed as investment, tax, or legal advice. The content is based on publicly available information and Paasa’s understanding of current regulations, which are subject to change. Investing in international markets involves risks, including currency fluctuations, regulatory changes, tax implications, and market volatility. Past performance does not guarantee future results. Investors should consult their financial, tax, and legal advisors before making any investment decisions.