For Indians with global investment portfolios, repatriation is an important but oft-ignored topic.

Whether you are bringing money back to India for investments, personal expenses, or because of FEMA regulations, clarity around the rules is a must.

Understanding the regulations around repatriation and foreign remittance can help you stay compliant in India, avoid surprises from the Income Tax Department, and get better returns from your investments in the long term.

Table of contents

- What is repatriation?

- How can I bring back money from abroad?

- How is the repatriated income taxed in India

- Can I keep my income abroad in USD without repatriating back to India?

- What exchange rate is applicable when converting money back to INR?

- Tax compliance and documentation in India

- Types of bank account for repatriation

- What happens to unrepatriated foreign assets in case of death?

- How can people moving back to India manage their overseas assets

- How Paasa helps in repatriation

- FAQs

What is repatriation?

Repatriation is the process of bringing money back to your home country from overseas.

For Indian investors with global portfolios, this means transferring funds from an external source, such as a US brokerage account or a foreign bank, into an Indian bank account.

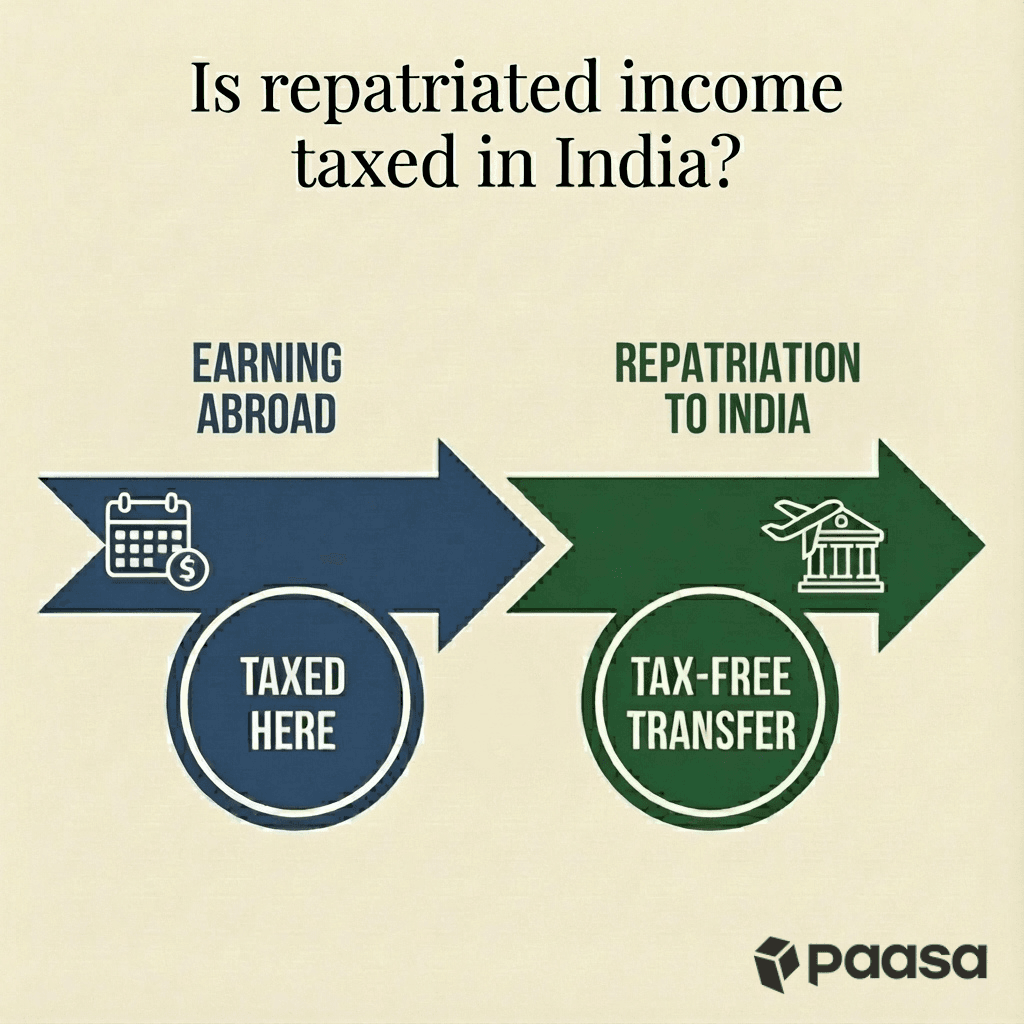

It is important to note that repatriation itself is not a taxable event. The tax liability arises the moment you earn the income (e.g., when you sell a stock for a profit or receive a dividend), regardless of where the money sits.

Once you have settled the tax on that income, the money is yours, and you are free to transfer it back to India without incurring any additional tax.

Here is how repatriation fits into the investment cycle:

Action | Is this Repatriation? | Tax Implication | |

Step 1: Investment | You send money from India to a US Brokerage to buy Apple stocks. | No. This is Outward Remittance (LRS). | None. You are just moving capital. |

Step 2: Selling | You sell the stocks for a profit. The cash sits in your US brokerage wallet. | No. The money is still abroad. | Tax Triggered. You have realized a gain. You must pay tax on this. |

Step 3: Transfer | You wire the cash from your US brokerage to your Indian bank account. | Yes. This is Repatriation. | None. You are simply moving your own tax-paid money home. |

Your tax liability occurs in Step 2 when you sell the stock and make a profit. Step 3 is purely a banking transaction. You are simply moving your own money from the US to India.

How can I bring back money from abroad?

Bringing money back to India is a standard banking process that typically does not require any extra steps.

You can simply initiate a wire transfer or SWIFT transaction from your overseas bank to your Indian bank.

While the backend compliance is handled by the banks, you should keep proofs of income, such as salary slips or investment statements, handy in case your bank requests them to verify the source of funds.

When the funds hit your Indian account, you must request a FIRC (Foreign Inward Remittance Certificate) or a "Remittance Advice" from your bank.

Without a FIRC, the Income Tax Department may treat unexplained high-value credits as "unexplained cash credits" or "black money," leading to severe penalties.

Always archive your FIRC for at least 8-10 years.

How is the repatriated income taxed in India

In India, tax is levied on the accrual of income (when you earn it), not on the receipt of funds (when you bring it back).

If you have already declared your foreign income in your annual IT Return and paid the applicable tax, the actual transfer of funds to your Indian bank account is tax-neutral.

Note: The tax regulation applicable will depend on your residential status at the time when you earned the income, not on your tax residential status at the time of repatriation.

Example

Suppose you are a software professional who lived and worked in the US for 5 years, invested in stocks, and later moved back to India.

- 2018 – 2023 (US resident): You lived in the US, earned salary, and invested $200,000 in US stocks.

- 2023 (Move to India): You return to India permanently.

- 2025 (Indian resident): You sell $50,000 worth of US stocks and repatriate the money to an Indian bank account.

Here is how the taxation applies at each stage:

Tax Residency Status | Tax Implication | |

Earning Salary (2018–2023) | US Tax Resident | Taxed in the US. You pay US taxes on your salary when you earn it. India does not tax this because you were an NRI/US resident during this period. |

Selling Stocks (2025) | Indian Tax Resident | Taxed in India. Since you are now an Indian resident, the profit (Capital Gains) from this sale is taxable in India in the current financial year. |

Repatriating Funds (2025) | Indian Tax Resident | No Tax. The act of transferring the $50,000 to your Indian bank account is not taxable. |

You are taxed based on when you earn the money (or realize the gain) and where you live at that moment. The movement of money back to India (repatriation) creates no extra tax liability, provided you have settled the taxes on the income itself.

For detailed information on how foreign investments are taxed, visit our guide on How Global Stocks and ETFs Are Taxed for Indian Investors.

How repatriated capital gains are taxed?

Capital gains are taxed in the year you sell the asset, regardless of whether you bring the money back or keep it abroad. The rate of tax depends on your tax residency status.

If you are an Indian tax resident with a global portfolio, capital gains from foreign stocks and ETFs are taxed at these rates:

Holding Period | Capital Gain Classification | Tax Rate |

≤ 24 Months | Short-Term (STCG) | Slab Rate (Added to your income) |

> 24 Months | Long-Term (LTCG) | 12.5% (Flat rate without indexation) |

Example

Suppose you are a C-suite executive in an India-based company with a globally diversified portfolio.

You decide to sell $70,000 worth of UCITS ETFs that you have held for over 3 years. From this sale, you make a profit (Long-Term Capital Gain) of $10,000.

You then repatriate the entire $70,000 proceeds to your Indian bank account.

Here is how the taxation applies:

Amount | Tax Implication | |

Capital Gain | $10,000 | Taxed in India. Since you held the asset for >24 months, this profit is taxed at 12.5% (LTCG). |

Principal Amount | $60,000 | No Tax. This is your original invested capital. |

Repatriation | $70,000 | No Tax. The act of transferring the full $70,000 to India is not a taxable event. You only pay tax on the $10,000 profit. |

Your tax bill is calculated on the $10,000 gain. The remaining $60,000 is your own principal coming back, and the movement of the total funds (repatriation) creates no extra tax liability.

For an in-depth explanation (with examples) of how foreign capital gains are taxed, visit our guide on Capital Gains Tax on Foreign Stocks and ETFs.

How repatriated dividend income is taxed?

For Indian tax residents, dividend income is taxed in the year it is credited to your foreign account. Again, your dividend income is not taxed when you repatriate it, rather it is taxed when you actually earn the income.

India classifies dividend income as income (income from other sources to be specific) and taxes it according to your income tax slab.

Example

Suppose you are a businessperson based in India with a globally diversified investment portfolio. You receive $15,000 as dividend income from your US stocks.

You decide to use $10,000 of this amount to buy more stocks, and you send the remaining $5,000 back to India because you are approaching the 180-day FEMA deadline for holding idle foreign cash.

- Income event: You receive $15,000 as dividend income from your US stocks.

- Usage: You use $10,000 of this cash to buy more stocks immediately.

- Repatriation: Since you cannot hold the remaining idle cash indefinitely, you send the balance $5,000 back to your Indian bank account to meet the 180-day FEMA deadline.

Here is how the taxation applies:

Action | Tax Implication | |

Dividend Income | You earn $15,000 in dividends. | Taxed in India (as you are an Indian tax resident). You must pay tax on the full $15,000 in India (under 'Income from Other Sources') according to your slab rate. |

Reinvestment | You use $10,000 to buy new stocks. | No Tax. Reinvesting the cash is a valid usage of funds. It does not trigger a new tax, nor does it reduce your tax liability on the original dividend. |

Repatriation | You transfer $5,000 to India. | No Tax. The act of transferring this $5,000 to your Indian bank account is not taxable. You have already paid tax on the income itself; bringing the cash home is tax-free. |

You are taxed on the total income you earned ($15,000), not on the amount you brought back ($5,000). Whether you reinvest the money abroad or bring it home, the tax liability remains the same because it is based on earning, not moving.

For an in-depth explanation (with examples) of how dividend income is taxed in India and abroad, visit our guide on How Foreign Dividend Income is Taxed for Indian Investors.

Can I keep my income abroad in USD without repatriating back to India?

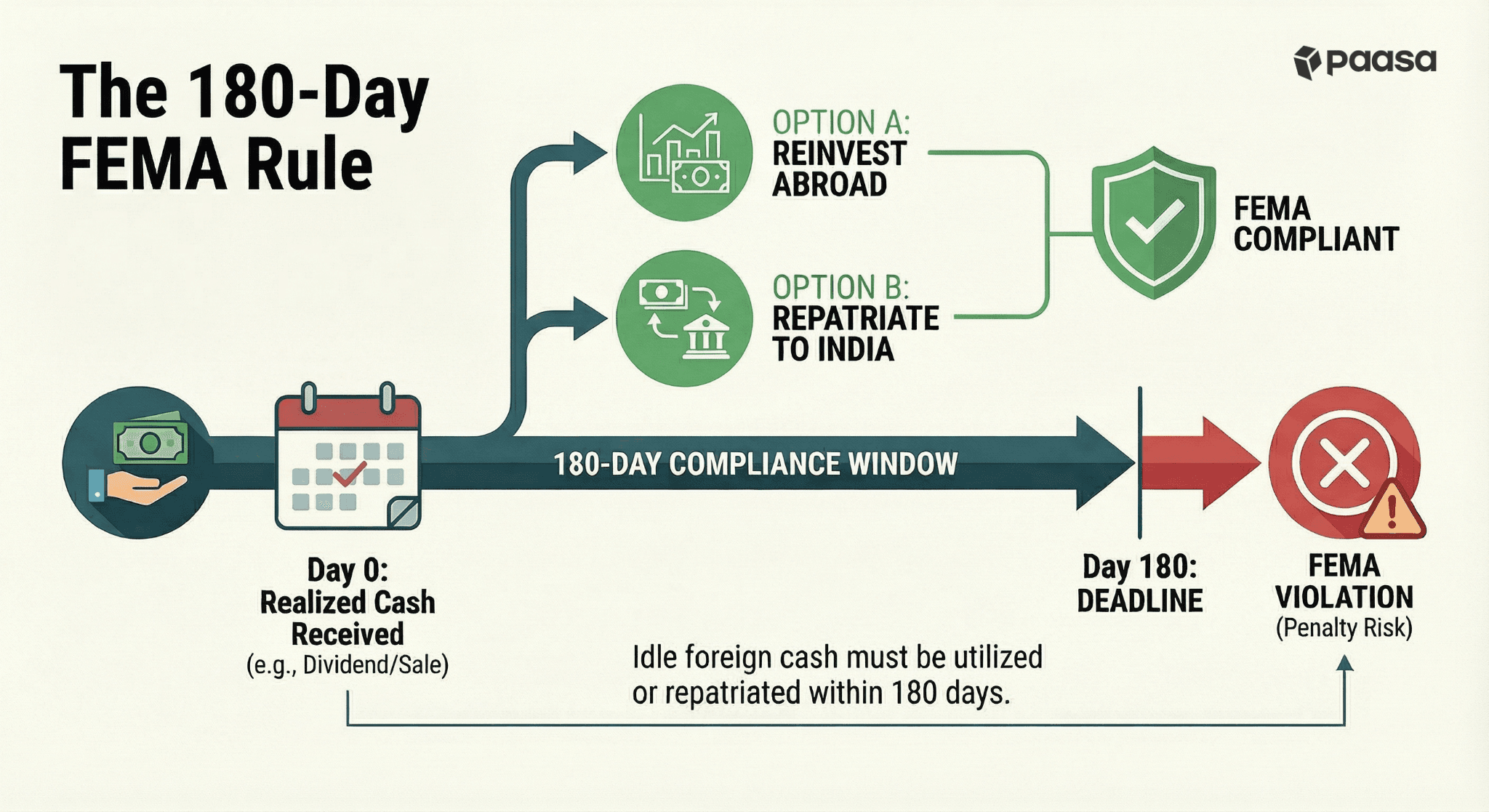

Not indefinitely if you are an Indian tax resident.

If an Indian tax resident receives foreign currency their overseas account (like salary, dividends, interest, or money from selling a stock), they have 180 days from the date of receipt to do one of two things:

- Reinvest or spend it: Buy more stocks, bonds, or ETFs.

- Repatriate it: Send the money back to your Indian bank account.

If you do neither and let the cash sit there for Day 181, you are technically in violation of FEMA laws.

When Is It Triggered?

The 180-day countdown starts the moment "Realized Cash" hits your account.

Event | Status | Compliance Clock |

Stock Price Goes Up | Unrealized Gain | Not Triggered. (You can hold indefinitely). |

Dividend Payment | Realized Income | Triggered. |

Selling a Stock | Realized Cash | Triggered. |

Salary Credit | Realized Income | Triggered. |

Example

- Jan 1: You receive a $1,000 dividend in your Paasa/US Broker account.

- Jan 1 – June 29: The cash sits in your wallet. You are safe.

- June 30 (Day 180): You must effectively "use" this cash.

- Option A: Buy $1,000 worth of shares.

- Option B: Wire $1,000 back to your bank account in India. (Perfectly legal; the clock stops).

- July 1 (Day 181): The cash is still sitting idle in the wallet.

- Result: You are now in violation of FEMA regulations.

Is there any limit on the amount I can repatriate?

No, there is no limit on the amount of money you can bring back to India.

Whether it is salary income, business profits, or capital gains from your investments, you can repatriate the entire amount freely.

While you can bring in as much as you want, sending it back abroad later is restricted. Under the Liberalised Remittance Scheme (LRS), a resident individual can only remit up to $250,000 per financial year (April to March) per PAN card.

What exchange rate is applicable when converting money back to INR?

The exchange rate for bringing money back (inward remittance) is decided entirely by your receiving bank in India, not the sending bank.

Most banks default to applying their "Card Rate," which often includes a high profit margin (spread).

If you are transferring a significant amount, do not accept the default rate.

Instead, call your Relationship Manager (RM) before the transfer hits your account and negotiate for a "Live Deal Rate" or "Treasury Rate."

This is usually much closer to the actual market rate and can save you a significant amount in conversion fees.

Tax compliance and documentation in India

When you repatriate funds to India, the burden of proof lies on you to establish the source and nature of the money.

To stay compliant, you must obtain and preserve the Foreign Inward Remittance Certificate (FIRC) or a formal "Remittance Advice" for every single transaction.

While banks automatically generate these for business transactions, individual accounts often just receive a credit notification. You must proactively request a specific advice slip or certificate that details the sender's name, the foreign currency amount, and the purpose of the transfer.

This document acts as your primary shield if your transaction is ever flagged for scrutiny by the Income Tax Department. High-value international transfers often trigger the Statement of Financial Transactions (SFT) reporting logic.

If the tax officer questions a sudden credit of ₹50 Lakhs in your account, the FIRC serves as conclusive legal proof that the funds are legitimate, tax-paid capital or income from abroad, rather than unexplained "black money" or taxable domestic income.

Types of bank account for repatriation

The type of account you use to bring money back depends entirely on your residential status at the time of the transfer. Choosing the wrong account type can lead to compliance issues with FEMA or unnecessary tax complications.

1. For Resident Indians

If you are an Indian Tax Resident, you do not need any special "foreign" account to receive funds.

- Standard Savings/Current Account: You can wire funds directly to your regular savings account. The bank will automatically convert the foreign currency (USD/GBP) into INR at the prevailing exchange rate upon credit.

- The Better Option (RFC Account): If you are a returning NRI or have significant foreign earnings, you should consider opening a Resident Foreign Currency (RFC) account. This allows you to hold the money in foreign currency (like USD or GBP) within India without converting it to INR immediately, saving you from exchange rate fluctuations until you are ready to use the funds.

2. For Non-Resident Indians (NRIs)

NRIs (Indian citizens living abroad >182 days/year) strictly cannot hold regular resident savings accounts. For repatriation, you must use specific NRI accounts:

- NRE (Non-Resident External) Account: Best for repatriating foreign earnings.

- Benefits: Principal and interest are fully repatriable (you can send it back abroad anytime). Interest earned is tax-free in India.

- FCNR (Foreign Currency Non-Resident) Account: Ideally suited for HNIs who want to hold money in foreign currency (USD, Euro, etc.) to avoid exchange rate risk.

- Benefits: Fully repatriable and tax-free interest.

- NRO (Non-Resident Ordinary) Account: Primarily used for income earned within India (like rent or dividends).

- Limitations: Repatriation is capped at $1 Million per financial year. Interest earned is taxable in India.

3. For PIOs and OCIs

Persons of Indian Origin (PIOs) and Overseas Citizens of India (OCIs) follow the exact same banking regulations as NRIs. You are eligible to open NRE, NRO, and FCNR accounts.

- Repatriation Rules: Funds in NRE/FCNR accounts remain fully repatriable. Funds in NRO accounts are subject to the same $1 Million/year limit and require a 15CA/CB certificate for repatriation.

What happens to unrepatriated foreign assets in case of death?

Claiming foreign investments is procedurally similar to claiming Indian assets. Your heirs simply need to contact the broker and provide standard documents, like a death certificate, to start the transfer process.

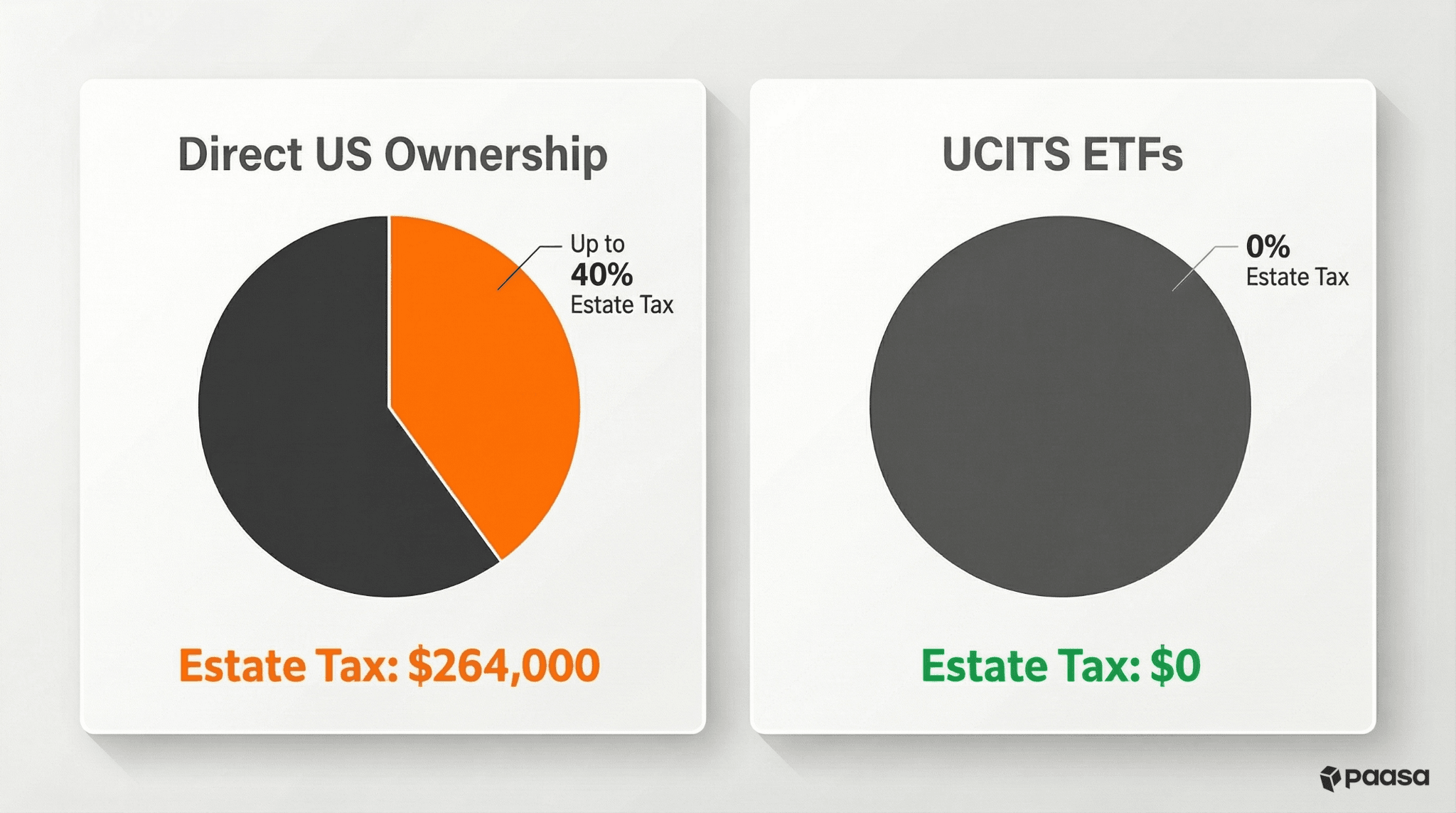

However, while the process is simple, there is a major financial risk that most investors overlook: the US estate tax.

While India does not charge inheritance tax, the US applies a tax on the transfer of US assets owned by non-residents.

US estate tax on assets over $60,000

For non-US residents (like Indian investors), this tax applies if your US assets, such as stocks or ETFs, exceed $60,000.

- The tax rate: The US government charges a tax of up to 40% on the value of assets above $60,000.

- No treaty protection: This tax is not covered by the Double Taxation Avoidance Agreement (DTAA) between India and the US.

For example, if you hold US stocks worth $200,000, you will have to pay $36,000 (17.9%) in estate tax.

Use our US Estate Tax Calculator to find the exact tax you will have to pay.

How the estate tax is collected

The IRS does not automatically deduct the tax from your account. Instead, the process is manual and can lock your funds for a long time.

- Account freeze: As soon as the broker is notified of the death, they freeze the account. Your heirs cannot sell stocks or withdraw money.

- Payment from own pocket: Your heirs must calculate the tax and pay it to the IRS using their own funds. They cannot use the money inside the frozen brokerage account to pay this tax.

- Waiting period: After payment, the IRS takes about 18 to 24 months to issue a transfer certificate.

- Release of assets: The broker will unfreeze the account and transfer the assets to your heirs only after they receive this certificate.

Repatriation of inherited funds

Once the process is complete and your heirs receive the assets, the rules for bringing the money back are straightforward:

- Capital gains tax: If your heirs decide to sell the stocks, they must pay capital gains tax in India. This is calculated based on the price you originally paid for the stocks.

- Tax-free repatriation: The act of transferring the money back to India is not taxed. Since the estate tax and capital gains tax cover the liability, bringing the funds home is tax-free.

Recommendation: Avoid this risk with UCITS ETFs

The most efficient way to invest in US markets while avoiding the US estate tax is to use UCITS ETFs.

Since UCITS ETFs are legally domiciled in Europe (typically Ireland), not the US, they are not classified as "US-situated assets."

Even if the ETF holds Apple, Microsoft, or the S&P 500, your investment is legally in Ireland. This completely exempts your portfolio from the 40% US Estate Tax.

Use our UCITS Screener to discover and compare UCITS-compliant investment instruments.

How can people moving back to India manage their overseas assets

When moving back to India, you essentially have two choices: bring your assets with you (repatriation) or keep them invested abroad.

While bringing everything home feels like the "cleanest" option, it leads to significant capital erosion due to currency depreciation, transaction costs, and regulatory friction.

Option 1: Repatriate everything to India

If you sell your US stocks and wire the cash to India, you trigger a chain of costs and friction:

- Forced realization: You must sell your assets, triggering immediate Capital Gains Tax (in the US or India, depending on residency).

- Currency loss: You convert strong currency (USD) to a depreciating currency (INR).

- LRS regulations: If you ever want to send that money back abroad (e.g., for your child's education or to buy US stocks again), you are restricted by the LRS limit of $250,000 per year. You also face a 20% TCS (Tax Collected at Source) on the transfer.

Example

Suppose you moved back in 2020 with $1 Million and decided to bring it all to India. Five years later (2025), you want to send it back to the US for investment or personal needs.

- Step 1: Inflow (2020)

- You convert $1,000,000 at ₹74 (Average 2020 rate).

- Value in India: ₹7.4 Crores.

- Step 2: The idle period (2020-2025)

- While you held ₹7.4 Cr in India, the USD strengthened from ₹74 to ~₹86.

- Step 3: Outflow (2025)

- You now want to convert that ₹7.4 Cr back to USD.

- Exchange Rate: ₹86 + Bank Spread (1%) = ₹86.86.

- Regulatory Friction: You cannot send it all at once. The $250k LRS limit forces you to split this over 4 years (or use 4 family members' PAN cards).

- TCS Impact: On top of the transfer, you must pay 20% TCS upfront (approx ₹1.48 Cr blocked until you claim a refund).

- Final result:

- ₹7.4 Cr / 86.86 = ~$851,945.

- Net Loss: You lost ~$148,000 (nearly 15% of your wealth) purely due to currency depreciation and exchange spreads.

Option 2: Keep assets abroad

A far more efficient approach is to leave your corpus invested abroad. This provides advantages like:

- Tax deferral: Every time you sell to repatriate, you trigger a tax bill that eats into your capital. By keeping assets abroad, you pay tax only on the part you sell, when you decide to sell. The rest continues to grow.

- No currency risk: Your corpus remains in USD/GBP. This protects you from exchange rate fluctuations and preserves your global purchasing power.

- In-kind transfers: You don't have to sell your US stocks to change brokers. You can simply transfer the shares to a global account. No sale means zero tax liability during the move.

- No foreign remittance limit: If you ever need to move abroad again, your funds are already there. You avoid the 20% TCS and the $250,000 annual limit that apply when trying to send money out of India.

Staying invested abroad and avoiding unnecessary tax events in the middle can make a major difference in your long-term returns. By deferring taxes and staying in a strong currency, you allow your wealth to compound more effectively over time.

Recommendation: Do not liquidate your global portfolio just because you are moving. Use Paasa to transfer your existing brokerage holdings via in-kind transfer and manage them as an Indian resident without triggering a taxable sale.

How Paasa helps in repatriation

Paasa is the platform used by global Indian Investors, HNIs, family offices to diversify their wealth across global markets like US, UK, China, Singapore, Switzerland, and beyond.

Paasa offers a comprehensive advisory layer that keeps your portfolio compliant and makes tax filing hassle free with:

- Dedicated relationship manager

- Ongoing remittance, FEMA and tax advisory

- Ongoing tax loss harvesting and rebalancing

- End of year tax documents

What type of documents does Paasa provide to file taxes?

At the end of the financial year, Paasa provides a ready-to-file tax package containing:

- Capital Gains Report: A clear breakdown of Short-Term vs. Long-Term capital gains, calculated specifically according to the 24-month holding rule for unlisted shares.

- Dividend & Interest Reports: Consolidated statements showing exactly how much income you earned and the tax withheld abroad, making it easy to fill Schedule FSI.

- Schedule FA Report: This is typically the hardest part of the ITR. We provide a report with the Peak Value and Closing Value of your assets in INR, calculated using the mandatory SBI TT Buying Rates, so you can simply copy-paste the numbers into your tax return.

If you are an Indian tax resident or NRI who wants to understand how to repatriate larger sums while keeping your future goals like investments, global travel, or your children's education in focus, feel free to reach out to our team of experts.

Disclaimer

This article is intended solely for information and does not constitute investment, tax, or legal advice. The material is based on public sources and our interpretation of prevailing regulations, which are subject to change. Global investments carry certain risks, including currency risk, political risk, and market volatility. Past performance does not predict future outcomes. Please seek advice from qualified financial, tax, and legal professionals before acting.