Indian residents increasingly use Paasa to hold Japan equities such as Toyota, Sony, Nintendo, or broad Japan ETFs. Dividend income from these holdings is paid in Japan and reported in India, which can create confusion about who taxes what and how to avoid paying twice.

The India–Japan Double Taxation Avoidance Agreement (DTAA) solves this by ensuring your cross-border equity income is taxed only once. This guide explains how the treaty works for dividends, interest, and capital gains, and how Paasa helps you file the Japan treaty application or claim a refund and complete Form 67 so your post-tax returns reflect a single effective tax.

Table of Contents

- What is Double Taxation

- Understanding the India–Japan DTAA

- Residency Rules under DTAA

- Source vs Residence (Who gets to tax what)

- How DTAA Applies to Dividends, Interest & Capital Gains

- How to avoid double taxation?

- Example 1: Interest Income

- Example 2: Dividend Income

- Japan Inheritance/Wealth Taxes (What the DTAA Does Not Cover)

- Common Mistakes Investors Make

- Conclusion

- FAQs

What is Double Taxation

When you earn income in one country but live in another, both countries may try to tax the same income. This overlap is called double taxation.

Example: You are an Indian resident investing in Japan stocks or equity ETFs through Paasa.

• Japan deducts 15.315% as withholding tax on dividends you receive.

• When you file your return in India, you must declare that same income again because India taxes global income.

• Without relief, you would pay both taxes in full, once in Japan and again in India.

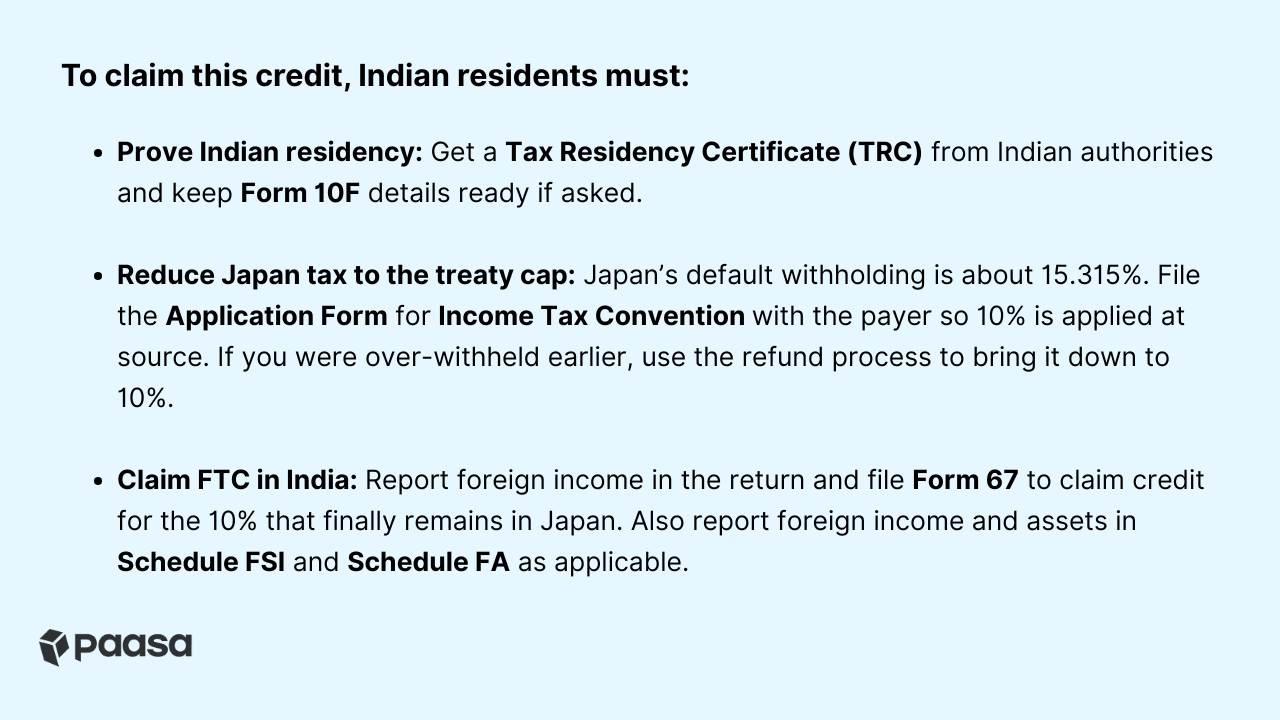

The Double Taxation Avoidance Agreement (DTAA) prevents this by setting limits on tax at source and letting you claim credit in India for tax already paid abroad. For Japan, filing the treaty application with the payer gets the 10% treaty rate at source. If over-withholding happens, a refund process can correct it to the treaty rate.

Without DTAA | With DTAA | |

Investor | Indian resident holding Japan stock via Paasa | Indian resident holding Japan stock via Paasa |

Dividend received | $10,000 | $10,000 |

Tax withheld in Japan | $1,532 (15.315%) | $1,000 (10% at source) |

Tax payable in India (30% slab) | $3,000 | $3,000 |

Credit allowed for Japan tax paid | ❌ None | ✅ $1,000 |

Final tax payable in India | $3,000 | $2,000 (balance only) |

Total tax paid overall | $4,532 (double taxed) | $3,000 (single effective tax) |

With DTAA, Japan withholds 10% at source and India gives you a Foreign Tax Credit for that 10% via Form 67. The net result is one effective layer of tax (your Indian rate), not two.

Note: Paasa helps investors apply these treaty benefits correctly through Japan’s tax treaty application paperwork and guided Form 67 filing, ensuring every dollar earned abroad is taxed only once.

What is the India & Japan DTAA Treaty?

The India–Japan Double Taxation Avoidance Agreement (DTAA) makes sure the same income is not taxed twice, once where it is earned (the source country) and again where the investor lives (the residence country).

For Indian residents earning dividends from Japan stocks or equity ETFs via Paasa, this treaty is what keeps your total tax fair and compliant. (Japan deducts tax first; the treaty + India’s credit rules ensure you do not pay twice.)

While the DTAA covers many income types, this guide focuses on equities and fixed income, specifically:

- Dividends from Japan shares and equity ETFs

- Interest from Japan-domiciled bond ETFs or bonds held directly

- Capital gains on listed shares/ETFs

In simple terms, the DTAA works through two mechanisms:

- Allocating taxing rights: It defines which country has the primary right to tax each category of income (for example, dividends vs. capital gains).

- Granting relief: If both countries tax the same income, your country of residence (India) allows a tax credit for tax already paid abroad.

With Japan, you typically file the treaty application with the payer so the 10% rate applies at source. If tax is over-withheld, a refund process reduces it to the treaty rate, and then India gives credit for the tax that ultimately remains.

You can read the official India–Japan DTAA text on the Government of India’s website here.

For a practical investing workflow for this market, read Invest in Japan from India.

Residency rules under DTAA

The treaty’s first step is to decide where you are a tax resident. If you are considered a resident in both India and Japan during a financial year, the DTAA uses a tie-breaker to pick one country for treaty purposes.

For example, if you live in India but spend significant time in Japan, the tie-breaker decides which country will treat you as its resident for tax purposes. It follows a clear sequence:

- Permanent home: Where you have a fixed home available.

- Centre of vital interests: Where your personal and economic relations are stronger.

- Habitual abode: Where you stay more frequently.

- Nationality: If still unresolved, the country of citizenship applies.

- Mutual agreement: In rare cases, both tax authorities mutually decide.

Understanding residency is crucial because DTAA benefits apply only to residents of one of the treaty countries. For most Indian investors earning Japan equity income such as dividends or capital gains (and interest from Japan-domiciled bond funds), India is the country of residence and Japan is the source country.

Source vs Residence (Who gets to tax what)

The treaty divides taxing rights between the country of source (where the income arises) and the country of residence (where you live and file taxes).

Here is how it works for income types relevant to Japan equities:

Type of Income | Taxed in Source Country (Japan) | Taxed in Residence Country (India) |

Dividends | Yes. Withheld at about 15.315% when paid by default; reduced to 10% at source when treaty paperwork is on file. | Yes, with credit for Japan tax that remains after the treaty rate is applied. |

Interest | Yes, when distributions are classified as interest (for example, from bond ETFs with Japan-source income). 15.315% at payment; reduced to 10% with DTAA paperwork. Bank or deposit interest is not covered in this guide. | Yes, taxed in India with foreign tax credit for the Japan tax that remains. |

Capital gains from sale of shares or securities | No. Japan does not tax a non-resident’s gains on listed shares or ETF units unless the investor held 25% or more at any time in the year of sale or the preceding two years and disposes of 5% or more in that year. | Yes. |

Employment income | Taxed in the country where services are rendered. Short-stay exceptions can apply. | Yes, if you are tax-resident in India. Foreign tax credit may apply if also taxed in Japan. |

How DTAA Applies to Dividends, Interest & Capital Gains

When Indian investors earn income from Japan assets such as stocks or equity or bond ETFs, Japan deducts tax at source before paying out. This is called withholding tax.

Under the India–Japan Double Taxation Avoidance Agreement (DTAA), this burden reduces. With the correct treaty form on file, Japan applies the treaty rate at source. If tax was over-withheld earlier, a refund process reduces it to the treaty rate and then India gives a foreign tax credit for the tax that finally remains.

Dividends

- By default, Japan withholds about 15.315% on dividends paid by Japan companies to non-residents.

- Under the DTAA, when the treaty application is filed with the payer, the rate is 10% for India-resident beneficial owners.

- The balance Indian tax is paid in India, with a credit for the 10% Japan tax that remains.

Japan Dividend Withholding | |

At payment without treaty paperwork | ~15.315% |

With DTAA rate applied at source (India resident, beneficial owner) | 10% |

Note: For most Paasa investors, expect the final Japan rate to be 10% when paperwork is in place. The same 10% can be claimed as a foreign tax credit in India via Form 67.

Interest

Interest income in scope here means bond coupons and interest-type distributions from Japan-domiciled bond ETFs or funds. It does not include bank or deposit interest.

Under the DTAA, the treaty rate is 10%. Without paperwork, the domestic default at payment is commonly about 15.315%. If over-withheld, you reclaim the excess so the final rate is 10%.

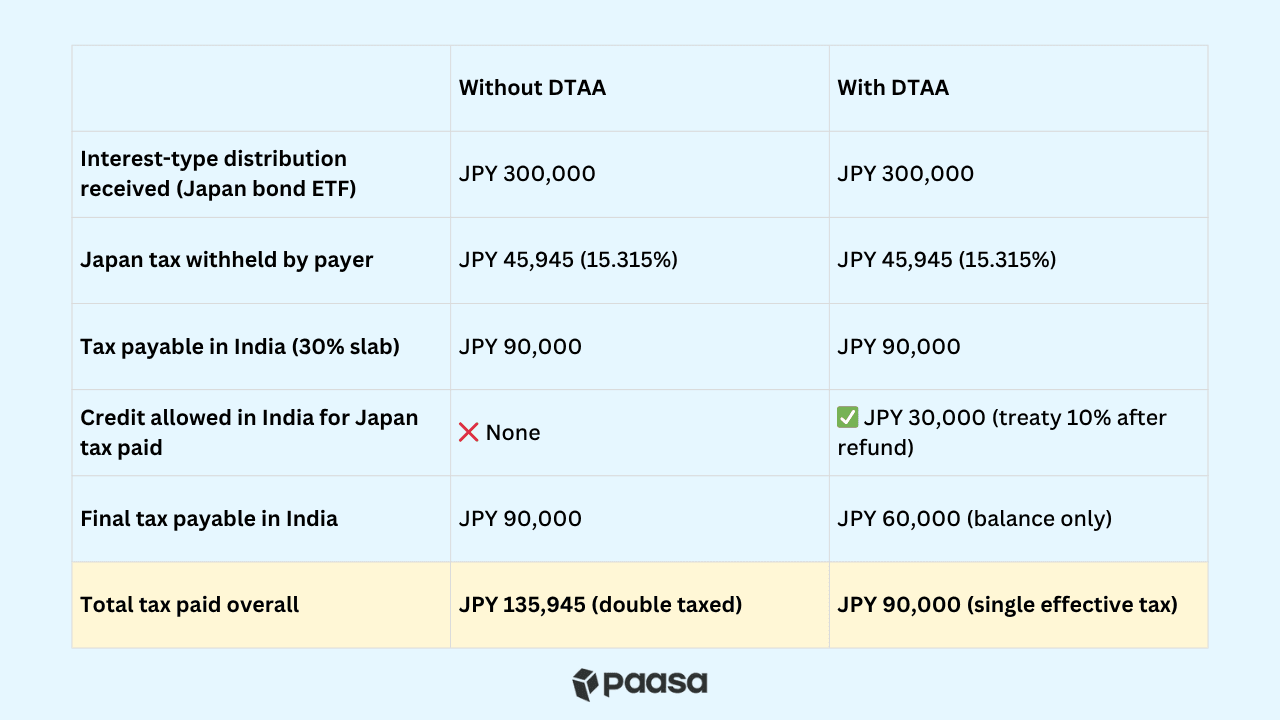

Example: You receive JPY 300,000 in Japan-source interest this year.

- Japan withholds JPY 45,945 (15.315%).

- In India, at a 30% slab, tax on this interest is JPY 90,000.

- You claim foreign tax credit of JPY 30,000 for the treaty 10% that finally remains after refund.

- You pay the balance JPY 60,000 in India.

- Total tax equals JPY 90,000 (your Indian rate), not 15.315% + 30%.

Japan Interest Withholding Tax Rate | |

No treaty paperwork submitted (default at payment) | ~15.315% |

DTAA rate applied or refund completed (India resident, beneficial owner) | 10% |

Capital Gains

Under the India–Japan DTAA and Japan domestic rules, capital gains from the sale of listed Japan securities by an India-resident portfolio investor are usually taxed only in India.

- Japan generally does not levy capital gains tax on non-resident portfolio investors selling listed shares or ETF units.

- Tax in Japan can apply if substantial-shareholder conditions are met (often called the 25/5 rule) or if the company is primarily real-estate-holding.

- Indian residents must report and pay capital gains tax in India.

- If Japan did not tax the gain at source, there is no foreign tax credit in India for that sale.

How to avoid double taxation?

Once both countries have exercised their taxing rights, the DTAA gives you relief through India’s Foreign Tax Credit (FTC) system under Sections 90 and 91, read with Rule 128.

Here’s how it works:

- If Japan finally keeps 10% on your dividend or in-scope interest and your Indian slab rate is 30%, India allows a credit for the 10% already paid abroad.

- You pay only the remaining 20% in India so that your total equals your Indian rate, not both countries added together.

Note: Paasa helps streamline this flow with clear income summaries, Japan treaty paperwork support, and ready-to-file Form 67 figures so every rupee earned abroad is taxed only once.

Example 1: Interest income

Imagine an Indian investor holding units of a Japan bond ETF. The fund pays interest-type distributions periodically.

- When those distributions are paid while the person is living in India, Japan withholds about 15.315% at source.

- Under the India–Japan DTAA, the final rate for individuals is 10%. You file the treaty application with the payer to apply 10% at source or claim a refund to reduce 15.315% down to 10%.

- Since the person is an Indian tax resident, India also taxes that same income as part of global earnings.

- Under the DTAA, the individual can claim a Foreign Tax Credit (FTC) in India for the 10% Japan tax that finally remains.

- Effectively, they pay only the difference in India if India’s rate is higher, not the full amount twice.

Example: Suppose an Indian investor receives JPY 300,000 of distribution income from the Japan bond ETF this year while living in India.

Paasa’s role:

- Paasa guides investors through the Japan treaty paperwork to reach the 10% treaty rate and prepares ready figures for Form 67 so the FTC is claimed correctly in India.

- We keep distribution breakdowns and Japan tax vouchers organized, reducing source-tax drag and protecting long-term returns.

Example 2: Dividend Income from Japan Stocks and ETFs

An Indian investor using Paasa may hold individual Japan stocks or equity ETFs with Japan exposure.

- Japan companies pay regular dividends, and Japan withholds about 15.315% at payment by default.

- Under the India–Japan DTAA, you file the treaty application with the payer to bring this down to 10% if you are an India-resident beneficial owner.

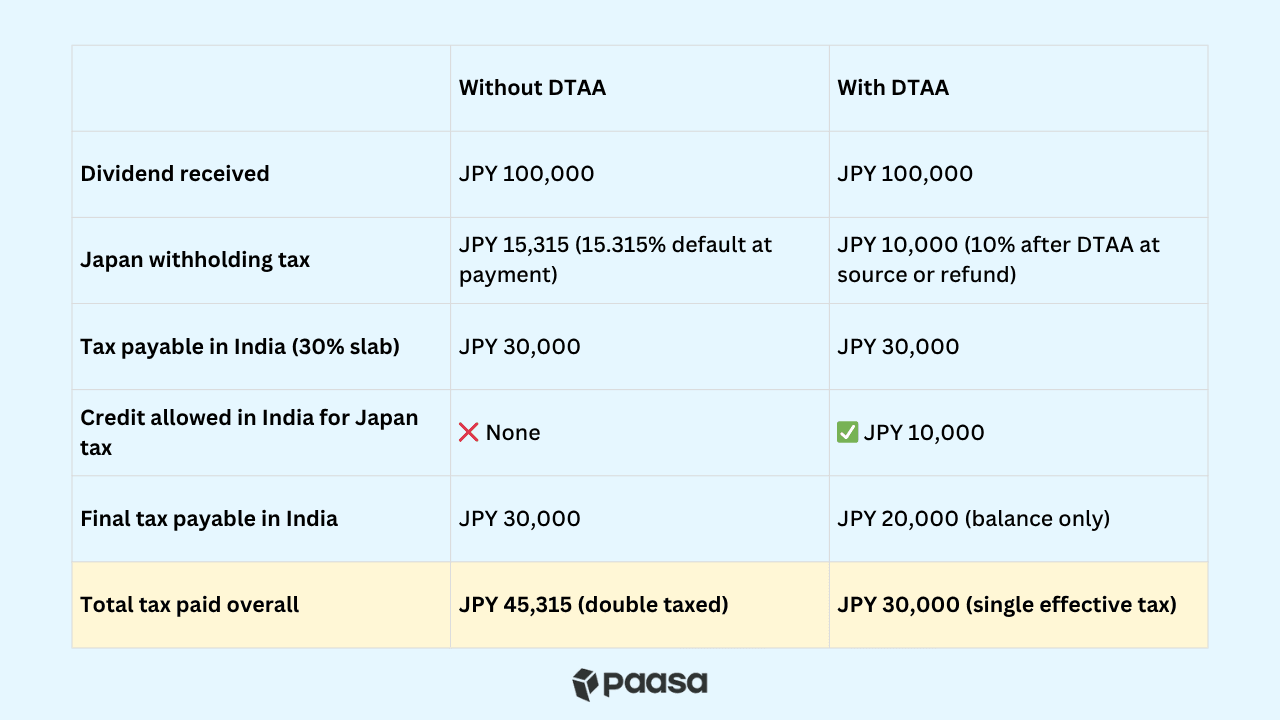

- In India, you must still declare the gross dividend and claim a Foreign Tax Credit (FTC) for the 10% finally kept by Japan.

How DTAA helps

- The 10% Japan tax that remains after the treaty rate or refund can be claimed as FTC in India through Form 67.

- If your Indian slab rate is 30%, you pay only the remaining 20% in India, so your total stays 30%, not 15.315% + 30%.

- Compliance stays straightforward with Paasa’s treaty paperwork support and ready FTC figures.

Example: Let’s say an Indian investor using Paasa receives JPY 100,000 in annual dividends.

Paasa’s role:

- Paasa guides investors through the Japan treaty application so the 10% rate applies and prepares ready figures for Form 67 so the FTC is claimed correctly in India.

- We keep dividend breakdowns and Japan tax vouchers organized, reducing source-tax drag and protecting long-term returns.

Japan Inheritance and Wealth Taxes (What the DTAA Does Not Cover)

Many Indian investors holding Japan equities are unaware that inheritance and gift taxes fall outside the India–Japan Double Taxation Avoidance Agreement (DTAA). The treaty covers only taxes on income, not on transfers of wealth or assets at death.

- Inheritance tax in Japan can apply even if you live in India. Japan’s tax law looks at both the decedent (the person who passes away) and the heir.

- If either person has a residential or address link to Japan (for example, they live, work, or own a permanent home in Japan), then Japan may tax worldwide assets–even those outside Japan.

- If both the decedent and the heir are non-residents with no Japan connection, then Japan taxes only Japan-situs assets, such as shares of Japan-resident companies, units of Japan-domiciled funds, or real estate in Japan.

- The inheritance tax rate is progressive from 10 percent up to 55 percent, depending on the taxable value of inherited assets after exemptions.

- A basic exemption of ¥30 million plus ¥6 million for each statutory heir applies before rates are calculated.

- India has no estate or wealth tax. Heirs in India do not pay any tax on the act of inheriting foreign shares. Tax arises only later, when the inherited shares are sold, and is treated under India’s capital-gains rules (12.5 percent long-term or slab-rate short-term, depending on holding period).

Paasa’s role: Paasa helps investors stay organized for succession by providing clear dividend and transaction statements, custody confirmations, and holding summaries that heirs and advisors can use. This keeps your global equity income compliant and makes it simpler for heirs to step in if needed.

Common Mistakes Investors Make

Even seasoned investors slip up when managing Japan equity income across two tax systems. These are not about intent, just clarity. Here are the most common ones to avoid:

Assuming Japan withholding is automatically adjusted in India

The ~15.315% tax deducted on dividends or interest does not sync with Indian filings. You must get the treaty rate at source or use Japan’s refund route to reach 10%, then claim credit in India for that 10%.

Skipping Form 67 submission

Missing Form 67 can forfeit your Foreign Tax Credit, even if Japan tax was paid and reduced to 10%.

Not reporting foreign assets in Schedule FA

Every overseas brokerage account and security must be disclosed in your Indian return. Non-disclosure can trigger scrutiny later.

Confusing inheritance/gift taxes with double taxation

The India–Japan DTAA covers income taxes only. Japan inheritance and gift taxes are separate and generally matter only if Japan’s rules pull you or your heirs into scope. Do not mix these with dividend withholding or FTC.

Forgetting the treaty mechanics on dividends and interest

Japan withholds about 15.315% at payment by default. Under the DTAA, you file the treaty application so the rate is 10% at source or refund the excess to 10%, and then claim FTC in India for that 10%. Filing correctly preserves your post-tax return.

Claiming credit for the wrong amount

You cannot claim FTC for the full ~15.315% deducted at payout or for any tax that is later refunded. Credit only the 10% that finally remains after Japan applies the treaty, capped by Indian tax on that income.

Relying on W-8BEN for Japan

W-8BEN is a U.S. form. It does nothing for Japan withholding. Use Japan’s treaty application forms via your broker, plus TRC and 10F details if asked.

Conclusion

The India–Japan DTAA ensures that Indian residents earning from Japan equities pay tax only once on their global income. Using Japan’s treaty paperwork to reach the 10% rate at source and claiming credit in India through Form 67 helps you stay compliant and protect post-tax returns.

About Paasa

Paasa helps Indian investors invest globally with full compliance. It is trusted by HNIs, family offices, and professionals with overseas income, and it lets you diversify across the U.S., Europe, Japan, and more.

What sets Paasa apart is its India-first compliance layer for cross-border investors:

FEMA, LRS, and DTAA alignment built into every transaction and cash flow.

- Integrated tax analytics and reporting for Indian residents investing abroad, covering LTCG, STCG, dividend tax, and TCS tracking.

- End-to-end support for remittances, reconciliation, and tax-credit documentation such as Form 67.

Whether you buy U.S. equities, UCITS ETFs, or follow curated global equity strategies, Paasa gives you a single transparent platform to keep your portfolio aligned with India’s tax and regulatory framework.

Relevant Reads

Compare routes, costs, and taxes across markets with these quick reads.

- Invest in US from India

- Invest in Ireland from India

- Invest in Switzerland from India

- Invest in China from India

- Invest in Japan from India

- Invest in Singapore from India

- Invest in UK from India

- Invest in Poland from India

- Invest in Germany from India

Disclaimer

This article is for information only and does not constitute investment, tax, or legal advice. The material is based on public sources and our interpretation of current regulations, which can change. Investing in global markets involves risks, including currency risk, political risk, and market volatility. Past performance does not predict future outcomes. Please seek advice from qualified financial, tax, and legal professionals before acting.