Many Indians today, especially those investing in the Singapore stock market or working with Singapore companies, hold SGX stocks like DBS, OCBC, and Singtel, as well as SGD bonds that generate income outside India.

What most do not realize is how different tax systems across countries can make global investing complex. The India–Singapore Double Taxation Avoidance Agreement (DTAA) simplifies this by ensuring your cross-border income is taxed only once, with both countries recognizing taxes already paid.

This guide explains how the treaty works, where it applies, and how Paasa helps Indian investors stay globally invested while remaining fully compliant.

Table of Contents

- What Is Double Taxation?

- What is the India–Singapore DTAA Treaty?

- Residency rules under DTAA

- Source vs Residence (Who gets to tax what)

- How DTAA Applies to Dividends, Interest & Capital Gains

- How to Avoid Double Taxation

- Example 1: Interest income

- Example 2: Dividend Income

- Common Mistakes Investors Make

- Conclusion

- FAQs

What Is Double Taxation?

When you earn income in one country but live in another, both countries may try to tax the same income. This overlap is called double taxation.

Example: You are an Indian resident investing in Singapore stocks like DBS Group, OCBC, and Singtel through Paasa.

- Singapore deducts 15% as withholding tax on the interest you receive.

- When you file your return in India, you must declare that same income again because India taxes global income.

- Without a treaty, you would pay both taxes in full, once in Singapore and again in India.

The Double Taxation Avoidance Agreement (DTAA) prevents this by allowing you to claim credit in India for taxes already paid abroad, so the same income is not taxed twice.

Without DTAA | With DTAA | |

Investor | Indian resident holding DBS Group shares via Paasa | Indian resident holding DBS Group shares via Paasa |

Interest received | S$10,000 | S$10,000 |

Tax withheld in Singapore | S$1,500 (15%) | S$1,500 (15%) |

Tax payable in India (30% slab) | S$3,000 | S$3,000 |

Credit allowed for Singapore tax paid | ❌ None | ✅ S$1,500 |

Final tax payable in India | S$3,000 | S$1,500 (balance only) |

Total tax paid overall | S$4,500 (double taxed) | S$3,000 (single effective tax) |

The investor saves S$1,500 by claiming credit for Singapore tax already paid, keeping the total tax at one effective rate instead of paying twice.

Note: Paasa helps investors apply these treaty benefits correctly through guided Form 67 filing and compliant tax reporting, ensuring every dollar earned abroad is taxed only once.

What is the India–Singapore DTAA Treaty?

The India–Singapore Double Taxation Avoidance Agreement (DTAA) has been in force since 1994. It is a tax treaty that ensures the same income is not taxed twice, once in the country where it is earned (the source country) and again in the country where the investor lives (the residence country).

For Indian investors earning in Singapore through stocks, bonds, interest, or ETFs, this treaty is what keeps your total tax fair and compliant. It applies to individuals, companies, and trusts that are tax residents of either India or Singapore and covers most types of cross-border income, including:

- Employment income (including stock options)

- Dividends and interest from Singapore investments

- Royalties or technical service fees

- Capital gains on financial assets

In simple terms, the DTAA works through two mechanisms:

- Allocating taxing rights: It defines which country has the primary right to tax each category of income.

- Granting relief: If both countries tax the same income, the country of residence allows a tax credit for taxes already paid abroad.

You can read the official India–Singapore DTAA on the Government of India website here.

For a practical investing workflow for this market, read Invest in Singapore from India.

Residency rules under DTAA

The treaty’s first step is to decide where you are a tax resident. If you are considered a resident in both India and Singapore during a financial year, the tie-breaker rule decides which country will treat you as its resident for tax purposes.

For example, if you work remotely for a Singapore company while living in India, the tie-breaker rule decides your tax residence.

It follows a clear sequence:

- Permanent home: Where you have a fixed home available.

- Centre of vital interests: Where your personal and economic relations are stronger.

- Habitual abode: Where you stay more frequently.

- Nationality: If still unresolved, the country of citizenship applies.

- Mutual agreement: In rare cases, both tax authorities mutually decide.

Understanding residency is crucial because DTAA benefits apply only to residents of one of the treaty countries. For most Indian investors earning Singapore-source income (dividends, interest, or capital gains), India is the country of residence and Singapore is the source country.

Source vs Residence (Who gets to tax what)

The treaty divides taxation rights between the country of source (where income arises) and the country of residence (where you live and file taxes).

Here’s how it works for key income types relevant to Indian investors in Singapore:

Type of Income | Taxed in Source Country (Singapore) | Taxed in Residence Country (India) |

Dividends | No, 0% withholding tax under Singapore’s one-tier system | Yes, reported and taxed in India. No foreign tax credit since no Singapore tax is paid |

Interest | Yes, 15% at source under the India–Singapore DTAA for individuals. | Yes, with foreign tax credit for Singapore tax paid |

Capital gains from sale of shares or securities | No | Yes |

Employment income | Yes, taxed where services are rendered | Yes, if you are tax-resident in India. Credit available for Singapore tax paid |

How DTAA Applies to Dividends, Interest & Capital Gains

When Indian investors earn income from Singapore assets such as stocks or bonds, Singapore may deduct tax at source before paying out. This is known as withholding tax. However, under the India–Singapore Double Taxation Avoidance Agreement (DTAA), the applicable rates apply once you declare your Indian tax residency to the payer and then claim foreign tax credit in India.

Let’s see how it works for the most relevant income types:

Dividends

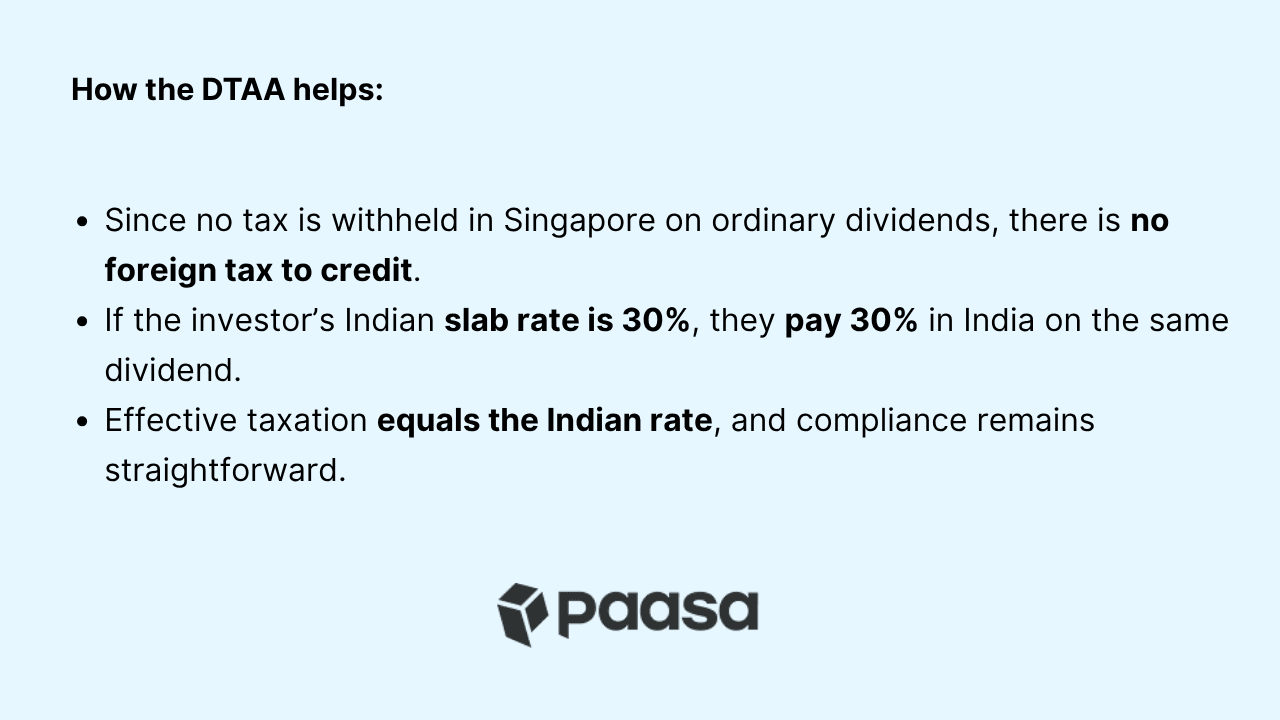

By default, Singapore withholds 0% tax on dividends paid by Singapore-resident companies.

After you declare treaty residency, the rate remains 0% because Singapore’s one-tier system does not impose dividend withholding.

Domestic rule today:

- Singapore’s one-tier system applies 0% dividend withholding.

- When domestic law is lower than the treaty ceiling, the lower domestic rate prevails → 0% at source.

When the treaty caps would matter: Only if Singapore reintroduces dividend withholding in the future.

Singapore Dividend Withholding Tax Rate | |

No tax forms submitted (default) | 0% |

Treaty residency declared (India tax resident) | 0% |

Interest

- Interest income from Singapore bonds or interest-bearing instruments faces a 15% withholding at source by default.

- Under the DTAA, for individual investors, the treaty rate is 15%. The 10% rate applies only when the recipient of the interest is a bank or similar financial institution (including insurers), not an individual.

Example: You receive S$30,000 in Singapore-source interest this year.

- Singapore withholds S$4,500 (15%).

- In India, at a 30% slab, tax on this interest is S$9,000.

- You claim foreign tax credit of S$4,500 for the Singapore tax.

- You pay the balance S$4,500 in India.

- Total tax = S$9,000 (your Indian rate), not 45%.

Singapore Interest Withholding Tax Rate | |

No tax forms submitted (default) | 15% |

Treaty residency declared (India tax resident) | 15% for individuals. 10% only when the recipient is a bank or insurer |

Note: For most Paasa investors who are individuals, expect 15% at source and a matching foreign tax credit in India via Form 67.

Capital Gains

Under the India–Singapore DTAA and Singapore domestic law, capital gains from the sale of Singapore securities by an Indian resident are taxed only in India, not in Singapore.

- Singapore does not levy capital gains tax on non-resident investors selling listed Singapore securities.

- Indian residents must, however, report and pay capital gains tax in India as part of their global income.

- The applicable tax rate depends on the holding period:

- Long-term capital gains on foreign shares held more than 24 months: 12.5% without indexation.

- Short-term capital gains (24 months or less): taxed at the investor’s income-tax slab rate.

How to avoid double taxation?

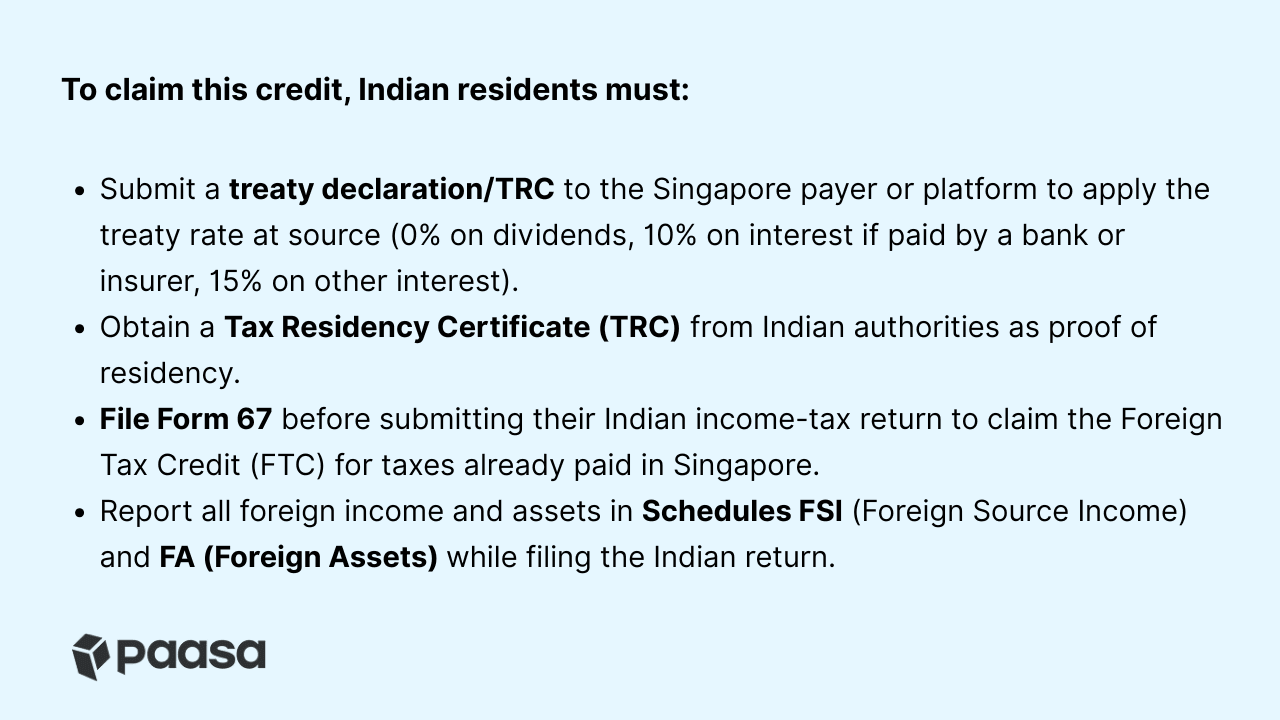

Once both countries have exercised their taxing rights, the DTAA ensures you receive relief through the Foreign Tax Credit (FTC) system in India under Sections 90 and 91 of the Income-tax Act.

Here’s how it works:

- If you paid 15% tax in Singapore and your Indian slab rate is 30%, India allows a credit for the 15% already paid abroad.

You only pay the remaining 15% balance in India, ensuring total tax equals your Indian rate, not both combined.

Note: Paasa simplifies this entire process for Indian investors in Singapore markets by generating global income summaries and ready-to-file tax reports that make claiming DTAA benefits effortless.

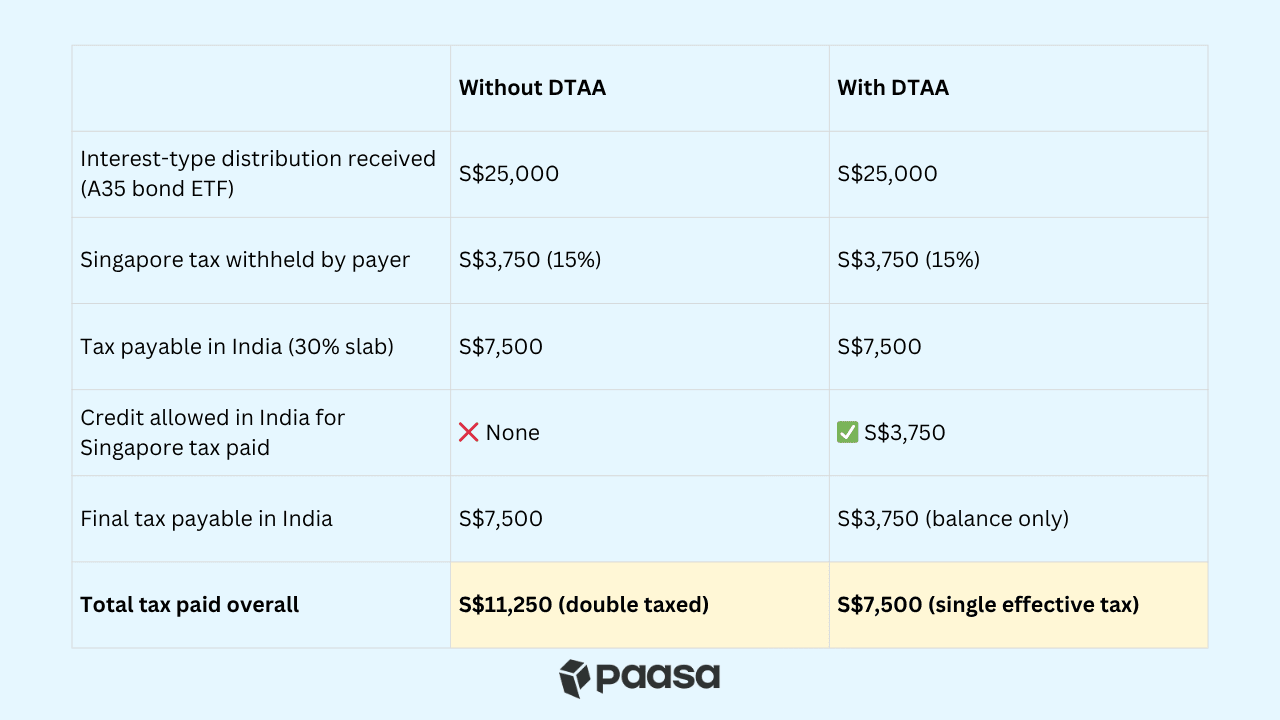

Example 1: Interest income

Imagine an Indian investor holding units of a Singapore-listed bond ETF such as ABF Singapore Bond Index Fund (A35). The fund pays interest-type distributions periodically.

- When those distributions are paid while the person is living in India, Singapore withholds tax at source. Under the India–Singapore DTAA, the rate for individuals is 15%.

- Since the person is an Indian tax resident, India also taxes that same income as part of their global earnings.

- Under the DTAA, the individual can claim a Foreign Tax Credit (FTC) in India for the tax already withheld in Singapore.

- Effectively, they only pay any difference if India’s rate is higher, not the full amount twice.

Example: Suppose an Indian investor receives S$25,000 of distribution income from A35 this year while they are living in India.

Paasa’s Role:

- Paasa guides Indian investors through every step of cross-border compliance, from preparing Form 67 and supporting documentation to understanding how to claim foreign-tax credits correctly.

- Many fixed-income products have specific source-tax rules and exemptions in Singapore. Paasa helps investors structure their holdings and documentation to reduce source-tax drag and protect long-term returns.

Example 2: Dividend Income from Singapore Stocks and ETFs

An Indian investor using Paasa may hold individual Singapore stocks like DBS, Singtel, or CapitaLand, or SGX-listed ETFs such as the Straits Times Index ETF (ES3).

- Singapore companies and ETFs pay regular dividends, and Singapore applies 0% withholding tax on company dividends under its one-tier system.

- Once the investor declares treaty residency, the rate remains 0% at source.

- The investor receives 100% of the declared dividend in the Paasa account.

- In India, the investor must still declare the dividend as part of global income.

Paasa’s role:

Paasa guides investors through the filing and documentation steps, including accurate dividend reporting in India and, where relevant for other income types, preparing Form 67 for cross-border FTC claims so DTAA benefits are applied automatically.

Common Mistakes Investors Make

Even seasoned investors often make simple mistakes when it comes to managing cross-border income. These usually do not arise from intent, just from lack of clarity. Here are the most common ones to avoid:

Assuming Singapore withholding is automatically adjusted in India

Tax withheld in Singapore on your interest or on certain REIT taxable distributions for non-resident non-individuals does not automatically sync with Indian filings. You must claim it through Form 67 to get the credit.

Skipping Form 67 submission

Missing this step means losing eligibility for the Foreign Tax Credit (FTC) even if you have already paid tax in Singapore.

Not reporting foreign assets in Schedule FA

Every overseas investment, brokerage account, or RSU holding must be disclosed in your Indian tax return. Non-disclosure can trigger scrutiny later.

Confusing estate duty with double taxation

Singapore abolished estate duty in 2008. That is different from income-based double taxation. Paasa helps investors stay compliant by structuring Singapore exposure correctly and preparing Indian filings so the right income character is reported and any FTC is claimed where applicable.

Forgetting treaty rates on dividends and interest

Dividends from Singapore companies are paid at 0% withholding, so there is no FTC to claim. Interest defaults to 15% unless you give the payer a Tax Residency Certificate (TRC or COR) to apply the treaty rate. Under the India–Singapore DTAA, interest is 10% if paid by a bank or insurer, and 15% otherwise. Filing correctly preserves post-tax returns.

Conclusion

The India–Singapore DTAA ensures that Indian residents earning from Singapore sources pay tax only once on their global income. Understanding and applying it correctly helps investors stay compliant and protect post-tax returns.

About Paasa

Paasa is the Indian investor’s gateway to compliant global investing, trusted by HNIs, family offices, and professionals with overseas income. It enables seamless diversification into markets across the U.S., Europe, China, Japan, and more.

What sets Paasa apart is its India-first compliance layer for cross-border portfolios:

- FEMA, LRS, and DTAA alignment built into every global transaction

- Integrated tax analytics and reporting for Indian residents investing abroad, including LTCG, STCG, dividend tax, and TCS tracking

- End-to-end support for remittances, reconciliation, and tax-credit documentation such as Form 67

Whether you invest in U.S. equities, global ETFs, UCITS funds, or managed strategies, Paasa provides a single, transparent platform that keeps your global investments aligned with India’s tax and regulatory rules.

Relevant Reads

Compare routes, costs, and taxes across markets with these quick reads.

- Invest in US from India

- Invest in Ireland from India

- Invest in Switzerland from India

- Invest in China from India

- Invest in Japan from India

- Invest in Singapore from India

- Invest in UK from India

- Invest in Poland from India

- Invest in Germany from India

Disclaimer

This blog is for informational purposes only and should not be treated as investment, tax, or legal advice. The information provided relies on publicly available data and our understanding of current regulations, which may change over time. Investing in international markets, including China, involves risks such as currency movements, political developments, and market volatility. Past performance is not indicative of future results. Investors should consult their financial, tax, and legal advisors before making any investment decisions.