Many Indians actively invest in or hold global portfolios that generate income outside India. But the different tax systems across countries can make tax filing and compliance complex, and result in double taxation in some cases.

Double Taxation Avoidance Agreements (DTAAs) are treaties between countries that simplify this by making sure that your global income is taxed only once; and that there are established rules regarding who can tax what, and how. This guide explains how India’s Double Taxation Avoidance Agreements work (with specific examples for the U.S., Singapore, the UK, and Switzerland), where they apply, and how Paasa helps Indian investors maintain a truly global portfolio while remaining fully compliant.

This guide explains how India’s Double Taxation Avoidance Agreements work (with specific examples for the U.S., Singapore, the UK, and Switzerland), where they apply, and how Paasa helps Indian investors maintain a truly global portfolio while remaining fully compliant.

Table of contents

- What is double taxation?

- Indian DTAAs and how they work

- Residency rules under DTAA

- Source vs. residence (Who gets to tax what)

- How to avoid double taxation for global holdings

- Conclusion

- FAQs

What is double taxation?

Things are generally simple when you live, work, and earn in India. But once you have global income sources (from one or more countries), both the country of income and the country of residence may try to tax the same income. This overlap is called double taxation.

For example, suppose you are an Indian resident investing in U.S. stocks or ETFs through Paasa.

If you have US stock market investments worth $100,000 and receive $5,000 as dividends, then:

By default, the U.S. government applies a flat 30% withholding tax on dividends paid to foreign investors. However, because India and the U.S. have a Double Taxation Avoidance Agreement (DTAA), you are eligible for a reduced rate. When you file a valid tax declaration (typically Form W-8BEN) through your broker to prove you are an Indian resident, the U.S. tax rate is automatically lowered to 25%.

Step | Without DTAA (Double Taxation) | With DTAA (Tax Relief) |

Gross Dividend Income | $5,000 | $5,000 |

Dividend Withholding Tax | -$1,500 (30% Standard Rate) | -$1,250 (25% Treaty Rate) |

Net Received in Bank | $3,500 | $3,750 |

Income Reported in India (Must Report Gross) | $5,000 | $5,000 |

Indian Tax Liability (30%) (A) | $1,500 | $1,500 |

Foreign Tax Credit (FTC) (B) | ❌ (No relief claimed) | ✅ $1,250 (Credit for US Tax) |

Net Tax Payable in India (A-B) | $1,500 | $250 |

Final Amount Left in Hand | $2,000 | $3,500 |

Effective Tax Rate | 60% | 30% |

Without DTAAs, this double taxation will occur for all your global income sources, essentially eroding your returns.

Indian DTAAs and how they work

These tax treaties ensure that the same income is not taxed twice, once in the country where it is earned (the source country) and again in the country where the investor lives (the residence country).

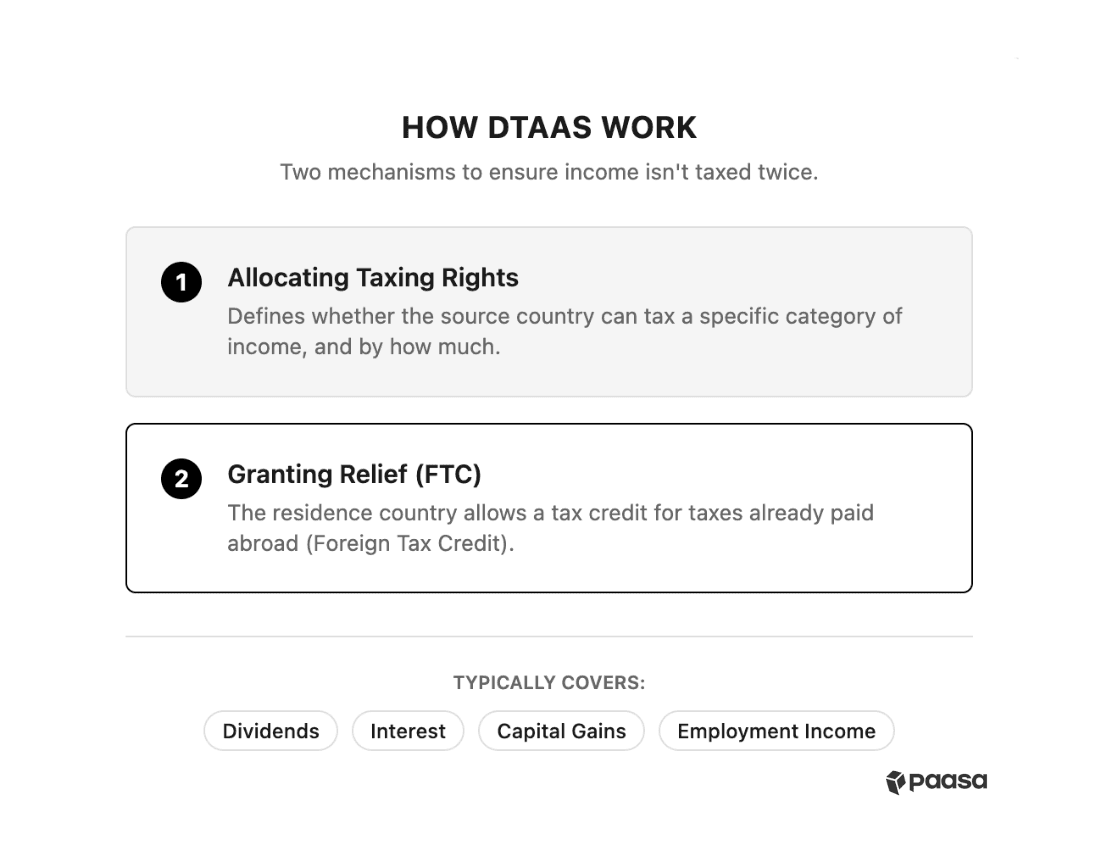

They typically cover:

- Employment income (including stock options)

- Dividends and interest

- Capital gains

These DTAAs work through two mechanisms:

These DTAAs work through two mechanisms:

- Allocating taxing rights: It defines which country has the primary right to tax each category of income.

- Granting relief: If both countries tax the same income, the country of residence allows a tax credit for taxes already paid abroad.

For in-depth information on India’s DTAAs with specific countries, read our guides on:

- India-US DTAA (Protecting Indian Investors from double tax)

- India-Singapore DTAA (Avoid Double Tax on Investments)

- India-UK DTAA (Prevent Double Taxation for Indian Investors)

- India-Swiss DTAA (Avoid Double Taxation for Indians)

- India-Ireland DTAA (Avoid Double Tax on Investments)

- India-Japan DTAA (Avoiding Double Tax for Indian Investors)

- Poland-India DTAA (Avoiding Double Tax for Indian Investors)

- China-India DTAA (Avoiding Double Tax for Indian Investors)

- Germany-India DTAA (Avoid Double Tax for Indian Investors)

Note: These benefits are not automatically applied; you have to actively claim these reliefs by going through specific procedures.

Paasa helps investors apply these treaty benefits correctly through guided Form 67 (for claiming foreign tax credit in India) filing, end-of-year tax documents, and access to a dedicated relationship manager for compliant tax reporting.

Residency rules under DTAA

Individuals are taxed according to the income tax regulations and DTAAs of the country where they are a tax resident.

You are considered a tax resident of India if:

- You are physically present in India for a period of 182 days or more in the tax year (182-day rule), or

- You are physically present in India for a period of 60 days or more during the relevant tax year and 365 days or more in aggregate in four preceding tax years (60-day rule).

However, depending on your travel history, global investment portfolio, and income sources, you might be considered a tax resident of multiple countries.

Example

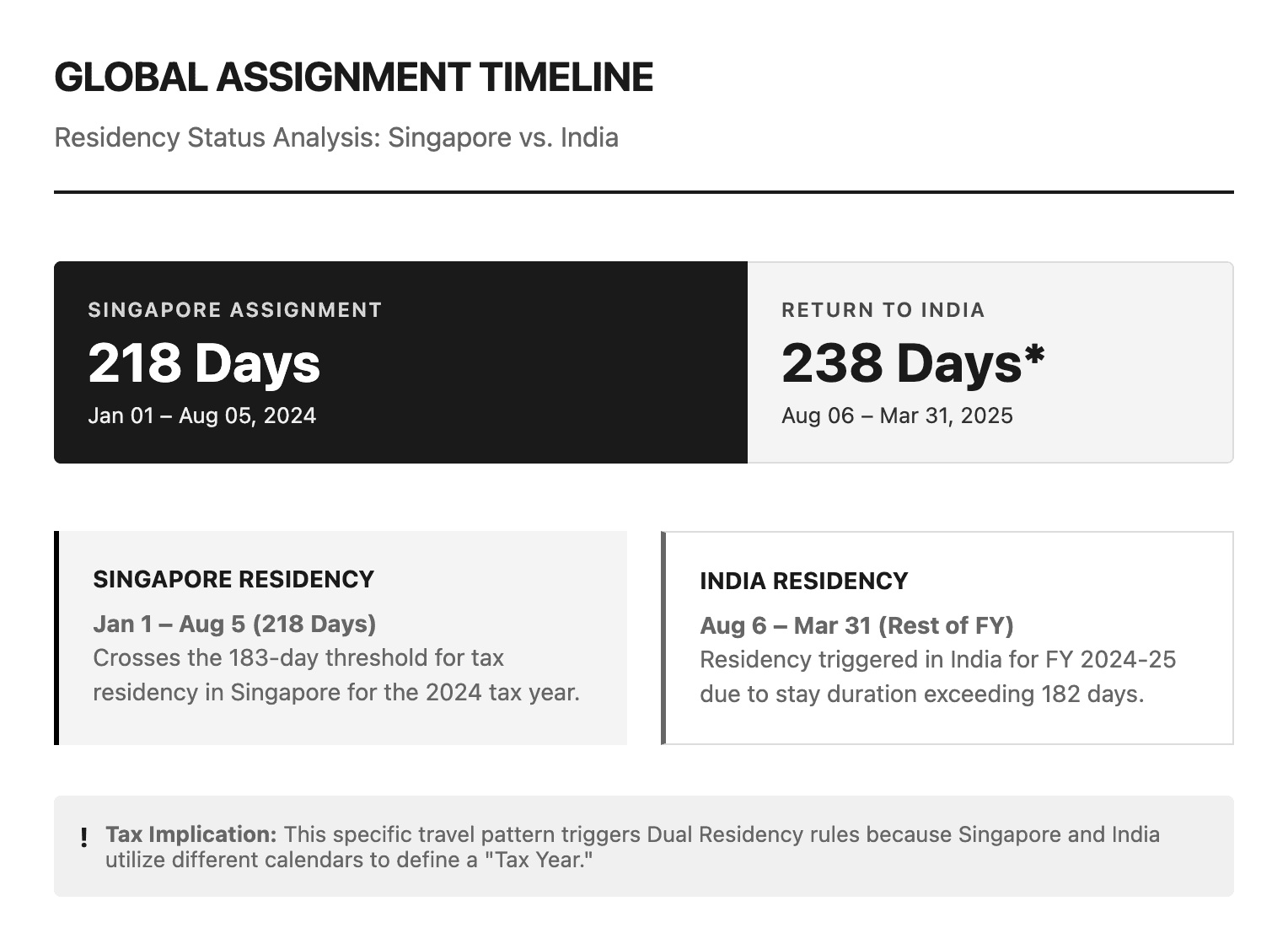

Suppose you are a software engineer sent on a long-term assignment to Singapore. You move there for a project at the start of the year but return to India later. Your schedule looks like this:

Suppose you are a software engineer sent on a long-term assignment to Singapore. You move there for a project at the start of the year but return to India later. Your schedule looks like this:

- 2024: You stayed in Singapore from January 1 to August 5 (218 days).

- Return: You returned to India on August 6, 2024, and stayed in India for the rest of the financial year (until March 31, 2025).

This specific travel pattern triggers residency rules in both countries because, like the U.S., Singapore uses a different calendar to measure a "tax year."

1. The Singapore View (Calendar Year)

Singapore calculates taxes based on the Calendar Year (January 1 – December 31). You are considered a tax resident of Singapore for a given Year of Assessment if you are a foreigner who has:

- Stayed or worked in Singapore for at least 183 days in the calendar year; or

- Stayed or worked in Singapore continuously for 3 consecutive years; or

- Worked in Singapore for a continuous period straddling 2 calendar years (and your total stay is at least 183 days).

Your Status: You were present for 218 days in 2024. Since you were present for more than 182 days, you are considered a Singapore Tax Resident for 2024.

2. The India View (Financial Year)

India calculates taxes based on the Financial Year (April 1, 2024 – March 31, 2025) . They look at your physical presence during this specific window.

- You were in Singapore for April, May, June, and July 2024.

- You returned to India on August 6, 2024, and stayed till March 31, 2025.

- Total stay in India: Approximately 238 days (August to March).

Since you meet the Indian tax residency requirement of staying for 182 days or more, you are considered an Indian Tax Resident for FY 2024-25 .

The Result: Overlapping Tax Demands

Because of the calendar mismatch, you are legally a resident of both countries at the same time.

Specifically, the income you earn during the overlapping period of April 1, 2024, to December 31, 2024, is now at risk of being taxed twice:

- Singapore considers you a resident for this entire period (part of their 2024 tax year) and may tax the income you earned there.

- India considers you a resident for this entire period (part of the 2024-25 financial year) and claims the right to tax your global income .

In such cases, DTAAs have a tiebreaker rule that decides which country will treat you as a resident for tax purposes.

It follows a clear sequence:

- Permanent home: Where you have a fixed home available.

- Center of vital interests: Where your personal and economic relations are stronger.

- Habitual abode: Where you stay more frequently.

- Nationality: If still unresolved, the country of citizenship applies.

- Mutual agreement: In rare cases, both tax authorities mutually decide.

Source vs. residence (Who gets to tax what)

The treaty divides taxation rights between the country of source (where income arises) and the country of residence (where you live and file taxes).

Your income is ultimately taxed by India as per Indian income tax norms. But if the source country has deducted taxes, then you can claim the tax paid as tax credit in India.

Here’s how it works for Indian tax residents for key income types:

Dividend

Dividends are the most common form of passive income for global investors.

In India, your dividend income is taxable at your personal income tax slab rates.

Country | Dividend Tax (at Source) |

U.S. | 25% under DTAA |

Singapore | 0% under DTAA |

UK | 0% |

Switzerland | 10% under DTAA |

Ireland | 10% under the DTAA, or reduced to 0% at source with a valid V2 non-resident declaration. |

Japan | 10% under DTAA |

Poland | 10% under DTAA |

China | 10% under DTAA |

Germany | 10% under DTAA |

Example: You own Apple (US) shares and receive a $100 dividend, thus under the India-US DTAA, US government will tax you 25% on this so you will receive $75.

Interest

Interest income (from bonds, uninvested cash in brokerage accounts, or bond ETFs) also attracts different rates of withholding taxes depending on the country where the income originates.

Country | Interest Tax (at Source) |

U.S. | 15% under India-US DTAA |

Singapore | 15% |

UK | 0% (some corporate bonds may trigger 20% withholding, reduced to15% under India-UK DTAA). |

Switzerland | 10% under DTAA |

Ireland | 0% |

Japan | 10% under DTAA |

Poland | 10% under DTAA |

China | 10% under DTAA |

Germany | 10% under DTAA |

Example: You hold Singapore Government Bonds and earn SGD 1,000 in interest. Under the India-Switzerland DTAA, the broker will deduct 15% and you will receive SGD 850.

Capital Gains

Most major financial hubs do not tax non-residents on capital gains.

While you pay zero tax abroad, you must pay Capital Gains Tax (CGT) in India (Long Term or Short Term depending on the holding period):

- Long-term capital gains (held for more than 24 months): 12.5% without indexation benefit.

- Short-term capital gains (held for 24 months or less): Taxed at the investor’s income-tax slab rate.

Example: You bought Tesla (US) stock for $1,000 and sold it for $1,500. As the US government does not tax capital gains, you get the full $1500 sale proceeds.

Note that you will be taxed in India as per Indian norms.

How to avoid double taxation for global holdings

Once the source country has exercised their taxing rights, the DTAA ensures you receive relief through the Foreign Tax Credit (FTC) system in India under Section 90 and 91 of the Income-tax Act.

To claim foreign tax credit in India, you need to file Form 67 (and Form 10F if you are a non-resident), and report all foreign income and assets while filing income tax returns. You also need to file paperwork in the country where the income originates (source country).

The exact mechanism of claiming tax credit varies based on where your income originates. Here’s the process for various countries:

- How to Avoid Double Taxation For Holdings in the US

- How to Avoid Double Taxation For Holdings in Singapore

- How to Avoid Double Taxation For Holdings in UK

- How to Avoid Double Taxation For Holdings in Switzerland

- How to Avoid Double Taxation For Holdings in Ireland

- How to Avoid Double Taxation For Holdings in Japan

- How to Avoid Double Taxation For Holdings in Poland

- How to Avoid Double Taxation For Holdings in China

- How to Avoid Double Taxation For Holdings in Germany

Conclusion

Double Taxation Avoidance Agreements ensure that Indian residents earning from overseas sources pay tax only once on their global income. Understanding and applying the regulations correctly helps investors stay compliant and protect post-tax returns.

About Paasa

Paasa is an Indian investor’s gateway to compliant global investing, trusted by HNIs, family offices, and professionals with global income. It enables seamless diversification into markets across the U.S., Europe, China, Japan, and beyond.

What makes Paasa unique is its India-facing compliance layer built for cross-border investors:

- FEMA, LRS, and DTAA alignment embedded into every global transaction.

- Integrated tax analytics and reporting for Indian residents investing overseas (covering LTCG, STCG, dividend tax, and TCS tracking).

- End-to-end support for remittance structuring, reconciliation, and tax-credit documentation such as Form 67.

Whether it’s U.S. equities, global ETFs, UCITS funds, or managed strategies, Paasa provides a single transparent platform that ensures your global investments stay compliant with India’s tax and regulatory framework.

Disclaimer

This article is intended solely for information and does not constitute investment, tax, or legal advice. The material is based on public sources and our interpretation of prevailing regulations, which are subject to change. Global investments carry certain risks—including currency risk, political risk, and market volatility. Past performance does not predict future outcomes. Please seek advice from qualified financial, tax, and legal professionals before acting.