If you are an Indian professional working at a US tech company such as Google, Microsoft, or Nvidia, chances are a large part of your wealth today sits in company RSUs.

Let’s say those RSUs are now worth around $100,000 (~₹88 lakhs).

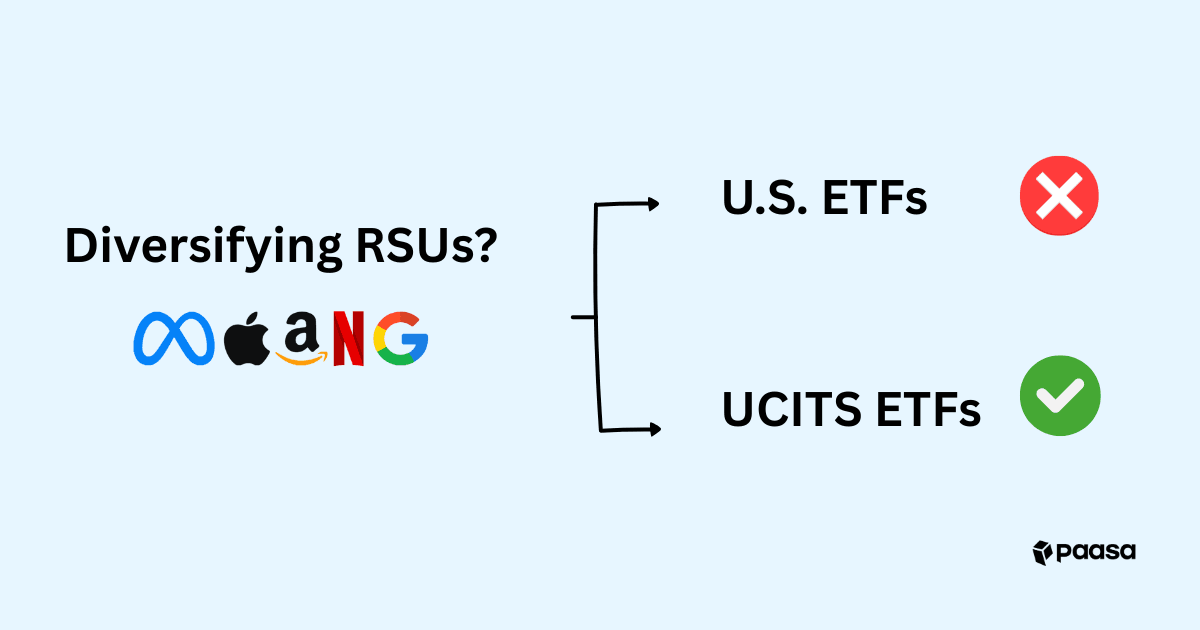

- You already know that holding them directly makes you liable to US estate tax, so you decide to sell and diversify that exposure.

- The next logical step seems simple: reinvest in US-listed ETFs. They offer broader exposure, lower concentration risk, and seem like the easiest way to stay invested in US markets while reducing tax exposure.

But here is the part most professionals miss. Those ETFs are still US-situs assets, which means they carry the same estate-tax risk you were trying to move away from.

This blog explains why that happens, what makes US-listed ETFs different from their global counterparts, and how certain non-US funds, known as UCITS ETFs, can help you achieve the same US market exposure without falling back into the US tax net.

Table of Contents

- Why US-listed ETFs still keep you inside the US tax net

- What are UCITS ETFs and why they are different

- UCITS vs US ETFs

- How RSU holders can transition to UCITS ETFs

- Conclusion

- FAQs

Why US-listed ETFs still keep you inside the US tax net

US-listed ETFs such as SPY, QQQ, or VOO are designed to give investors broad exposure to American markets. They trade on US exchanges, are registered with the US SEC, and hold their underlying assets through US custodians.

From a tax perspective, that makes them US-situs assets. For Indian investors, this detail is critical. Even if you invest in these ETFs from India, their legal domicile keeps them within the jurisdiction of the US estate-tax system.

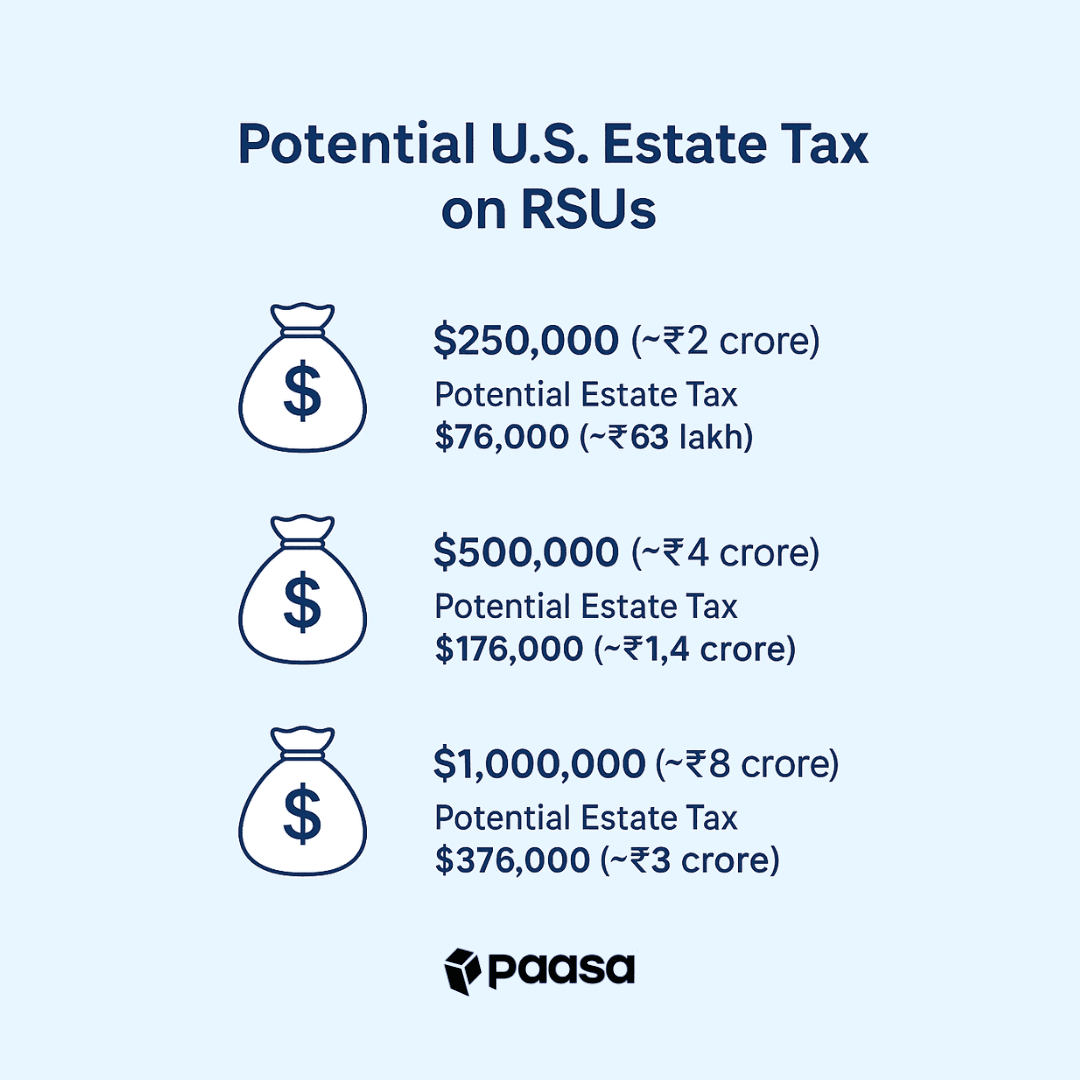

If the total value of your US assets, including ETFs, exceeds USD 60,000, the portion above that threshold can be subject to up to 40% estate tax in the event of death. It is a risk that many professionals overlook after selling RSUs and reinvesting in US ETFs.

Most investors assume diversification equals safety. In reality, diversifying within the same tax jurisdiction does not reduce estate-tax exposure. You are simply spreading the same risk across more instruments, not removing it.

If you want to understand this risk in more depth, especially how RSUs themselves create estate-tax exposure for Indian professionals, you can read our detailed explainer on the key risks with RSUs.

What are UCITS ETFs and why they are different

After selling your RSUs, your goal is not just to diversify but to protect that wealth from unnecessary tax exposure. This is where UCITS ETFs come in.

UCITS stands for Undertakings for Collective Investment in Transferable Securities. It is a European regulatory framework that governs how funds are created, managed, and marketed across the European Union.

- UCITS ETFs are non-US funds that can still invest in US markets but are domiciled in Europe, most commonly in Ireland or Luxembourg.

- UCITS ETFs are not considered US-situs assets. Even if they hold US stocks such as Apple, Microsoft, or Google, they sit outside the US estate-tax net.

This single difference changes the entire risk profile for Indian investors who have already built wealth through US company RSUs.

In addition to avoiding estate-tax exposure, UCITS ETFs offer two other advantages that matter for RSU holders:

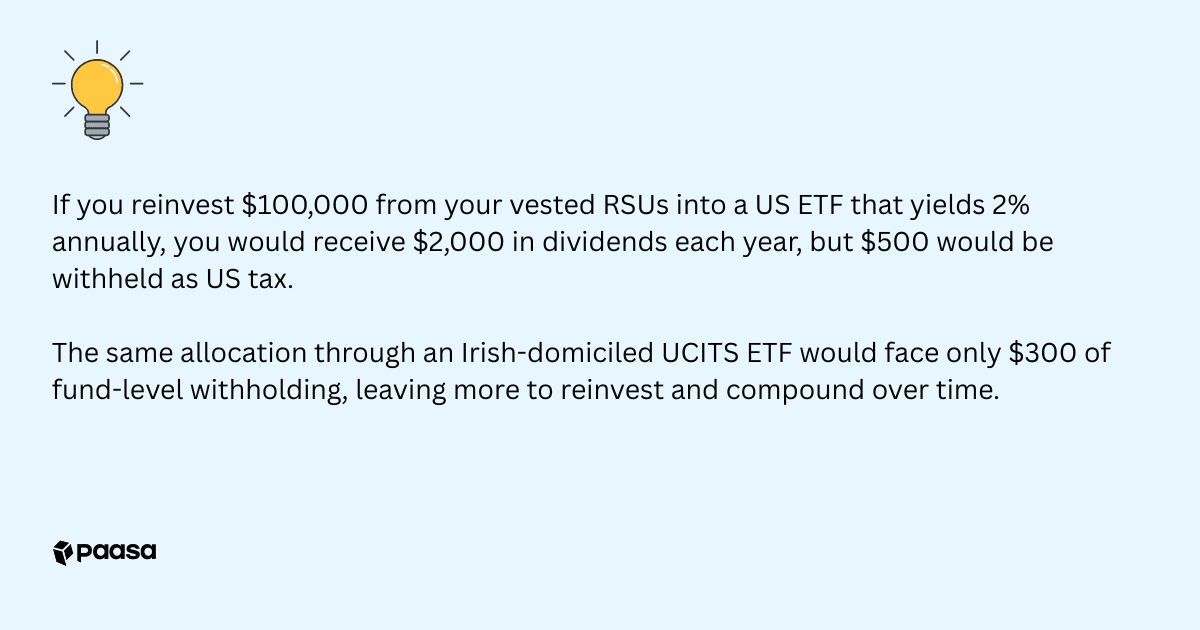

1. Lower dividend withholding

Most Irish-domiciled UCITS ETFs face only a 15% U.S. withholding tax at the fund level. In contrast, U.S. ETFs are subject to a 30% default rate, which can be reduced to 25% for Indian investors under the India–U.S. DTAA when Form W-8BEN is filed.

2. Accumulating share classes

Many UCITS ETFs automatically reinvest dividends back into the fund. This allows your returns to compound without triggering annual dividend taxation in India, which makes them particularly efficient for long-term compounding.

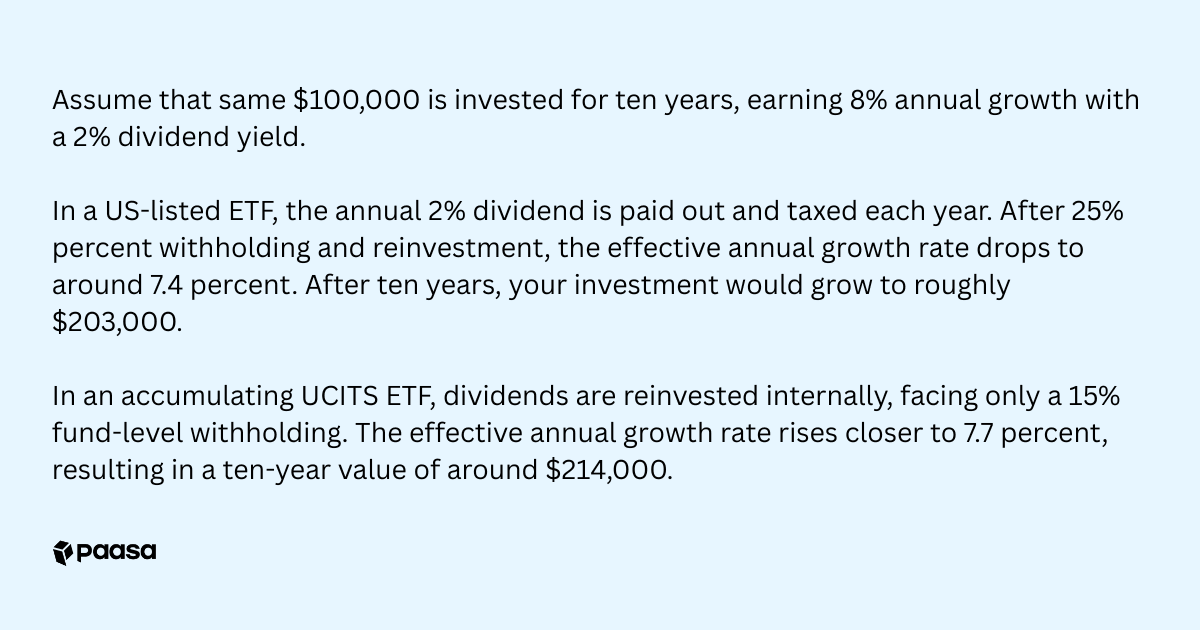

The difference may look small year by year, but over a decade, that compounding adds nearly $11,000 in additional value and that is before considering the estate-tax protection UCITS ETFs provide.

UCITS vs US ETFs (key structural differences)

Below is a simple comparison showing how each behaves when used to diversify RSU proceeds.

Aspect | US-listed ETF | UCITS ETF |

Domicile | United States | Ireland or Luxembourg |

Estate-tax exposure | Subject to up to 40% US estate tax once holdings exceed USD 60,000 | No estate-tax exposure as the fund is non-US domiciled |

Dividend withholding | 25% | 15% at fund level for Irish-domiciled ETFs |

Dividend handling | Mostly distribution share classes that pay out cash dividends | Option of accumulating share classes that automatically reinvest dividends |

Compounding efficiency | Interrupted each year by dividend payout and taxation | Continuous compounding due to internal reinvestment |

Regulatory oversight | US SEC | European UCITS framework focused on investor protection |

Currency options | Primarily USD | Available in USD, EUR, and GBP listings |

Use our UCITS Screener to discover UCITS-equivalents of US ETFs.

How RSU holders can transition to UCITS ETFs

For most professionals, the goal after each RSU vesting cycle is to convert concentrated company stock into a globally diversified portfolio. The challenge lies in doing this efficiently, without adding new layers of tax or regulatory complexity.

Paasa is a platform that helps Indian professionals diversify their RSUs end to end.

It connects your existing RSU holdings, bank accounts, and brokerage setup into a single compliant flow and enables you to liquidate RSUs, remit funds under LRS, and reinvest into UCITS ETFs in a seamless and fully compliant manner.

Here is how the transition works through Paasa?

Step 1: Sell or transfer your vested RSUs

Once your RSUs vest, Paasa helps you move them from your equity broker (whether that is Fidelity, Morgan Stanley, Charles Schwab, or E*TRADE) to a personal global brokerage account using the Automated Customer Account Transfer Service (ACATS). This gives you full control over your vested shares, separate from your employer’s ecosystem.

Step 2: Strategic liquidation

Once your RSUs appear in your Paasa account, you can choose to liquidate them either partially or fully depending on your goals.

This helps reduce exposure to a single company and frees up liquidity that can be redeployed toward diversified global investments.

Step 3: Reinvestment into UCITS portfolios

After liquidity is unlocked, you can reinvest the proceeds into UCITS ETFs or Paasa’s managed strategies.

These portfolios give you:

- global diversification beyond your employer’s stock,

- protection from US estate-tax exposure, and

- more efficient compounding through accumulating UCITS ETFs such as CSPX (S&P 500) or EQQQ (Nasdaq 100).

Step 4: Ongoing compliance handled

Paasa helps ensure that every step of your global investing journey remains compliant with Indian regulations.

This includes:

- FEMA/LRS reporting for cross-border remittances,

- Form 67 support for claiming foreign tax credits, and

- Schedule FA and FSI support for annual income-tax filings.

Note: Compliance support is provided when you are using Paasa’s managed strategies.

Typical timeline:

Most RSU transfers and reinvestments are completed within 3 – 5 business days, after which your funds are fully set up to diversify globally with confidence.

If you would like to understand this transition in detail, you can schedule a call with our team or reach us at support@paasa.com

Conclusion

You do not have to exit the US market to exit the US tax net.

That is the core shift UCITS ETFs enable for RSU holders who want to stay invested in global markets without carrying unnecessary risk.

Selling RSUs is the first step toward diversification. The smarter next step is to ensure that your new investments do not reintroduce the same estate-tax exposure in a different form.

UCITS ETFs make that possible by giving you identical US market access, cleaner tax treatment, and long-term compounding efficiency, all while staying outside the US estate-tax system.

About Paasa

Paasa is a global investing platform, designed specifically for Indian HNIs, family offices, and professionals with international wealth.

With Paasa, investors can go far beyond US equities. We enable access to UCITS ETFs, managed strategies, and access to global markets including China, Japan, Germany, Switzerland, Europe, and emerging economies. This makes it simple to build a portfolio that is globally diversified, tax-efficient, and fully compliant with Indian regulations.

Whether you are de-risking RSUs, planning estate tax protection, or building long-term cross-border allocations, Paasa provides the structure and support to secure your global wealth.

Disclaimer

This blog is for educational purposes only and should not be construed as tax, legal, or investment advice. RSU taxation, estate tax exposure, and cross-border investment rules are subject to change and may vary based on your personal circumstances.

Investing in global markets involves risks, including currency risk and market volatility. UCITS ETFs, RSUs, and other securities referenced here are used for illustration and do not constitute recommendations. Past performance is not indicative of future results.