For Indian tax residents with global joint brokerage accounts, the compliance requirements can be different and more complex compared to single owner accounts.

A clear understanding of the reporting requirements, the paperwork needed, and compliance laws are a must for joint brokerage account holders as small misses can trigger unwanted scrutiny from the Indian tax authorities.

Table of contents

- How are holdings from joint brokerage accounts taxed in India?

- How to stay compliant in India when having a joint global brokerage account?

- How are holdings from joint brokerage accounts taxed abroad?

- What happens to an IBKR joint brokerage account when one holder dies?

- How is US Estate tax liability decided in case one of the account holders die?

- Common mistakes people make

- How Paasa helps in Taxation

- FAQs

How are holdings from joint brokerage accounts taxed in India?

In India, the beneficial owner is taxed for the gains made from the joint account.

Essentially, tax liability follows funding and beneficial ownership: the person who provided the money owns the investments, receives the benefits, and pays the tax on gains.

In case both account holders own the investments and receive the money, they need to pay proportional taxes.

In case only one person paid for the investment but both received funds, the transaction is seen as an asset transfer, and the tax liability is dedicated accordingly.

Essentially, tax liability follows the person who provided the money to actually buy the asset and receives the benefits from the asset.

If both account holders contributed money to buy the assets, the capital gains are taxed proportionally based on their contribution ratio.

Example

Suppose you and your spouse open a joint brokerage account. You decide to invest $100,000 in a portfolio of US stocks.

- You contribute: $40,000 (40%)

- Your Spouse contributes: $60,000 (60%)

After a few years, the portfolio value grows to $150,000, and you decide to sell everything. The total capital gain is $50,000.

Contribution (Funds Provided) | Ownership Ratio | Share of Capital Gain ($50,000) | |

You | $40,000 | 40% | $20,000 |

Spouse | $60,000 | 60% | $30,000 |

Total | $100,000 | 100% | $50,000 |

Even though the account is joint, you do not split the tax 50-50.

- You must report a capital gain of $20,000 in your ITR.

- Your spouse must report a capital gain of $30,000 in their ITR.

Each of you will pay the applicable Long Term Capital Gains (LTCG) tax (12.5%) or Short Term Capital Gains (STCG) tax on your respective portion.

Learn more about how foreign capital gains are taxed.

How is dividend income from global brokerage accounts taxed in India?

Similar to capital gains, dividend income is taxed based on beneficial ownership. The person who provided the money to buy the shares is considered the owner of the dividend income generated by those shares, regardless of whose name appears on the account statement.

Example

Suppose you open a joint brokerage account with your spouse for operational convenience, but you contribute 100% of the funds. You invest $100,000 in US stocks, and during the year, the portfolio generates $2,000 in dividends.

Contribution | Ownership Ratio | Taxable Dividend Income | |

You | $100,000 | 100% | $2,000 |

Spouse | $0 | 0% | $0 |

Total | $100,000 | 100% | $2,000 |

In this scenario:

- You must report the full $2,000 as dividend income in your tax return and pay tax at your applicable slab rate.

- Your Spouse has zero tax liability for this dividend income because they did not fund the asset.

Learn more about how foreign dividend income is taxed.

What happens if the assets are bought from the funds of A but both A and B are beneficiaries of the profit?

If Person A provides 100% of the money used to buy the assets, but allows Person B to withdraw and keep a share of the profits, Indian tax law views this transaction as a Gift.

Since Person A is the beneficial owner, the primary tax liability falls on them first.

- First, Person A must pay the capital gains tax on the entire profit (since they funded the asset).

- Second, the amount shared with Person B is treated as a transfer of money (gift) from A to B.

The taxability of this "gift" depends on the relationship between A and B:

- If A and B are "Relatives" (e.g., Spouse, Sibling, Parent, Child): The transfer is tax-free. Under the Income Tax Act, gifts received from specified relatives are fully exempt from tax. You do not need to pay any additional tax on the money transferred to the joint holder.

- If A and B are Non-Relatives (e.g., Friends, Unmarried Partners): The transfer is taxable. If the amount Person B receives exceeds ₹50,000 in a financial year, the entire amount is treated as "Income from Other Sources" for Person B and taxed at their slab rate.

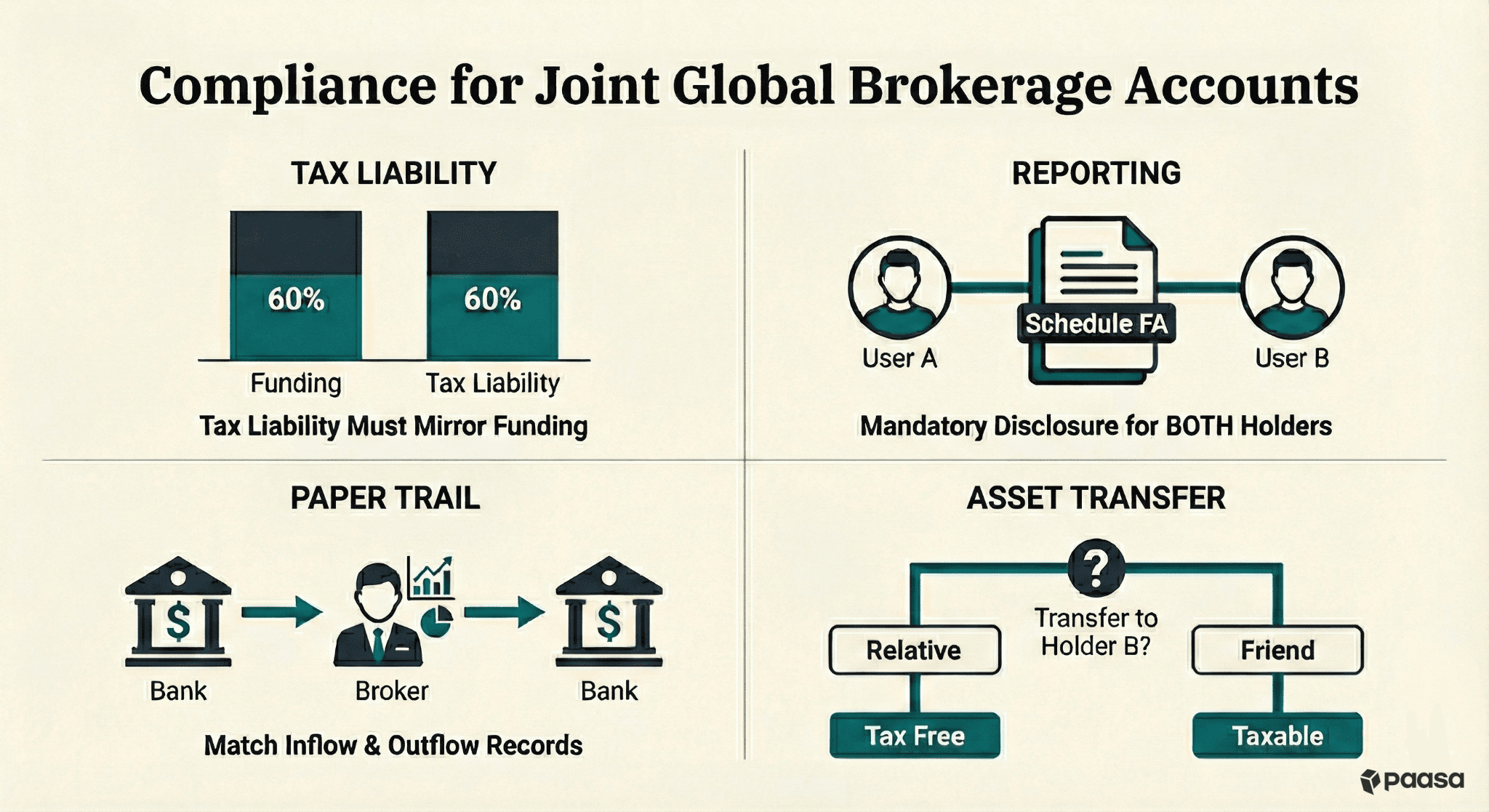

How to stay compliant in India when having a joint global brokerage account?

India requires you to disclose all foreign income in Schedule FSI, and also disclose all your foreign assets in Schedule FA.

In case of joint accounts, both account holders must disclose jointly held assets in Schedule FA irrespective of beneficial ownership status.

To avoid scrutiny from the tax department, you must also maintain a clear paper trail that distinguishes between "ownership on paper" and "beneficial ownership”:

1. Maintain a Precise Funding Trail

Since tax liability is determined by who funded the investment, you must keep records of the source of funds from the very inception of the account.

- Inflow: Keep bank statements showing exactly which account holder transferred money to the brokerage.

- Outflow: Similarly, when assets are sold and money is withdrawn, maintain records of who actually received the funds.

- If your funding was 60:40 but you split the tax liability 50:50, the tax department can treat the difference as unexplained income or tax evasion.

2. Document Asset Transfers (Gifts)

If the person who funded the asset is not the sole beneficiary of the sale (e.g., you funded 100% of the investment but allowed your joint holder to keep 50% of the profit), you must show this transfer clearly in your books.

- For Relatives: If the joint holder is a "relative" (e.g., spouse, sibling, parent, or child), this transfer is treated as a tax-free gift. It is best practice to document this with a simple gift deed or declaration to establish that the money was voluntarily transferred.

- For Non-Relatives: If the joint holder is not a defined relative, this transfer is taxable. You should clearly document it so the recipient can correctly report it as "Income from Other Sources."

How are holdings from joint brokerage accounts taxed abroad?

The source country taxes joint and individual accounts similarly. The withholding taxes charged depends on India’s DTAA with the specific country.

However, the paperwork provided for withheld taxes is slightly different for joint accounts, and this affects you when claiming foreign tax credit in India.

How are withholding taxes deducted for joint accounts?

In a joint account, the primary account holder's information is used for tax reporting purposes such as Name, Tax ID number and address.

The tax form you receive is in reference to the account's US taxable activity as a whole on the IRS Form 1042-S/1099.

The second account holder would not receive a separate tax form Form 1042-S/1099, all information is reported on one form.

For non-US markets (like the UK, Japan, or Europe), withholding tax rules and reporting standards vary significantly by jurisdiction. We recommend that you consult your tax advisor or brokerage directly to understand how tax certificates are issued for joint accounts in those specific markets.

What happens to an IBKR joint brokerage account when one holder dies?

If one account holder has passed away, you need to contact Interactive Brokers (IBKR) and inform them of the death, and provide them with the certified notice of death and other required documents.

IBKR will then guide you regarding the specific processes and may transfer the assets to the executor, administrator, or another legally appointed fiduciary who is managing the estate.

Note

After Interactive Brokers has received all required documents and the tax obligations has been settled, the disposition varies by account type:

- Joint Tenants with Rights of Survivorship: The account reverts to the surviving account holder on the death of the other.

- Tenants in Common: The deceased person's share passes to their heirs through a will or probate process rather than to the surviving account holder.

- Community Property: The account reverts to the surviving account holder unless there is a valid will directing the deceased holder's half otherwise.

The disposition of assets and any tax obligations remain the responsibility of the estate and beneficiaries (IBKR will not directly deduct any taxes), and generally requires the opening of a new individual account to transfer the assets. You should consult your tax advisor for questions about estate tax calculations, obligations, and how they apply to specific account types.

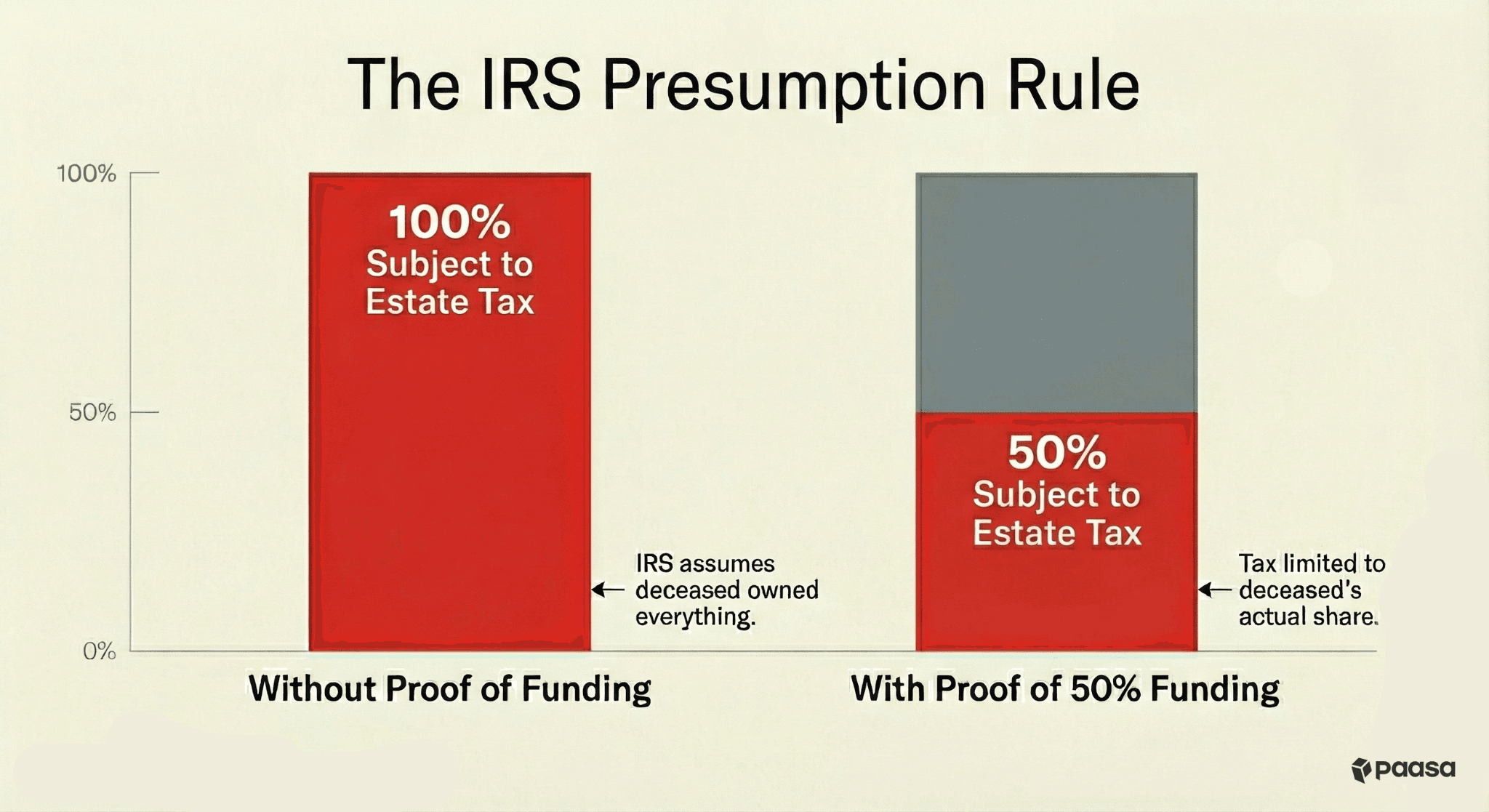

How is US Estate tax liability decided in case one of the account holders die?

For non-US residents, the US Estate Tax of up to 40% applies if the value of US-situs assets (like US stocks) exceeds $60,000.

In the case of joint accounts, the IRS presumes the first person to die owned 100% of the assets unless the survivor can provide evidence of their own financial contribution.

To avoid paying tax on the full amount, the surviving account holder must prove exactly how much they contributed to the account.

- If you can prove you funded 50%: Only 50% of the account value is taxed.

- If you cannot prove funding: The entire 100% is taxed, even if the survivor is a joint holder.

Important: Holding a "Joint Account with Rights of Survivorship" does not protect you from this tax. While the title and access to the account passes on differently depending on the account type, the tax obligation remains.

What to do if an IBKR joint account holder passes away?

If a joint account holder passes away, you need to contact Interactive Brokers immediately to report the death.

This transfer to the estate’s legal representative can happen before the IRS estate-tax requirements are fully resolved.

However, distribution from that executor to the actual heirs/beneficiaries is not allowed until one of the following documents has been provided:

- A signed letter from Executor or heir(s) affirming that on date of death, the deceased owned less than $60,000 in US-located assets, or

- A Transfer Certificate issued by the U.S. IRS

In order to obtain a Transfer Certificate, an estate tax return for a non-resident alien (Form 706-NA) must be filed and all taxes due paid.

IBKR will not directly tax accounts at the time of an account holder's death. The executor of the individual's estate is responsible for calculating and paying any applicable taxes, including US estate taxes on foreign nationals for US-domiciled assets.

Common mistakes people make regarding joint brokerage accounts

Arbitrarily splitting taxes equally

Many couples assume that a "Joint Account" allows them to split the income 50-50 to lower their tax liability.

In India, tax strictly follows the Source of Funds. If you contributed 100% of the capital, you must pay tax on 100% of the gains. Splitting the income without a matching split in funding is considered tax evasion.

Assuming being a "secondary holder" exempts you from reporting

A common error is thinking that the secondary holder (who didn't contribute funds) has no reporting obligation.

Indian tax law requires all residents to disclose foreign assets in Schedule FA of the ITR. Even if you are just a named beneficiary with zero financial contribution, you must disclose the account. Failure to do so triggers a flat penalty of ₹10 Lakhs under the Black Money Act.

Thinking "Right of Survivorship" helps avoid US estate tax

While a "Right of Survivorship" account allows the title of the assets to pass to your spouse automatically, it does not protect you from the US IRS.

The IRS assumes the entire account belonged to the deceased and is liable for 40% Estate Tax, unless the survivor can strictly prove their own financial contribution.

How Paasa helps in Taxation

Paasa is the platform used by global Indian Investors, HNIs, family offices to diversify their wealth across global markets like US, UK, China, Singapore, Switzerland, and beyond.

Paasa offers a comprehensive advisory layer that keeps your portfolio compliant and makes tax filing hassle free with:

- Dedicated relationship manager

- Ongoing remittance, FEMA and tax advisory

- Ongoing tax loss harvesting and rebalancing

- End of year tax documents

What type of documents does Paasa provide to file taxes?

At the end of the financial year, Paasa provides a ready-to-file tax package containing:

Capital Gains Report: A clear breakdown of Short-Term vs. Long-Term capital gains, calculated specifically according to the 24-month holding rule for unlisted shares.

Dividend & Interest Reports: Consolidated statements showing exactly how much income you earned and the tax withheld abroad, making it easy to fill Schedule FSI.

Schedule FA Report: This is typically the hardest part of the ITR. We provide a report with the Peak Value and Closing Value of your assets in INR, calculated using the mandatory SBI TT Buying Rates, so you can simply copy-paste the numbers into your tax return.

We believe that global taxation should not come at the cost of your peace of mind. If you are investing in global equities and have doubts around taxation, FEMA, LRS, or compliance, feel free to reach out to our team.

Disclaimer

This article is intended solely for information and does not constitute investment, tax, or legal advice. The material is based on public sources and our interpretation of prevailing regulations, which are subject to change. Global investments carry certain risks, including currency risk, political risk, and market volatility. Past performance does not predict future outcomes. Please seek advice from qualified financial, tax, and legal professionals before acting.