For Indian tax residents with diversified global portfolios, dividend payouts are a regular tax event.

A thorough understanding of how dividends are taxed, the applicable rates, calculation of exact tax liability, currency conversion rules, and how tax on dividends can affect your long term returns can help you stay compliant, avoid unwanted income tax notices, and optimize returns.

Table of contents

- What are dividends?

- How is dividend income calculated?

- How to calculate exchange rates for foreign dividend income and tax credit?

- Are foreign dividends subject to surcharge and cess?

- How is foreign dividend income taxed in the source country?

- How to claim back withholding tax charged on dividend income?

- What are the implications of dividend tax on long term returns?

- Optimizing returns by avoiding dividend tax

- About Paasa

- FAQs

What are dividends?

Dividends are a portion of a company's profits distributed to its shareholders, in proportion to their stake in the company. This means that dividends are declared as a certain amount ‘per share’.

Dividends are usually in the form of cash, but can also be in the form of additional shares.

The income received from this is called dividend income.

For example, suppose you are a senior software engineer who invests globally and you hold 100 shares of BlackRock.

If BlackRock declares a dividend of $5 per share, your dividend income from BlackRock shares will be $500 (100 shares x $5).

Note: Dividends are decided by the board of the company and the distribution typically coincides with earning report releases. The payout is at the discretion of the board, and not a fixed amount that shareholders are entitled to.

How is dividend income calculated?

Dividend income is simply the total amount of dividend payout you have received in a tax year.

Foreign dividends are usually subject to withholding tax in the source country. This withholding tax can be claimed back as foreign tax credit (FTC) in India.

You must calculate income based on the Gross Dividend declared before any taxes were deducted abroad.

Example

Suppose you hold a diversified portfolio with US stocks and US ETFs. During the financial year, you receive the following dividends:

The U.S. deducts 30% dividend withholding tax by default. However, because India and the U.S. have a Double Taxation Avoidance Agreement (DTAA), you are eligible for a reduced rate of 25%. Paasa handles the paperwork (Form W-8BEN) for you and ensures that you get the preferential rate.

Gross Dividend Declared (A) | Tax Withheld Abroad (B) | Net Amount Received (A-B) | |

Apple (US) | $8,000 | $2,000 (25%) | $6,000 |

Microsoft (US) | $7,000 | $1,750 (25%) | $5,250 |

Exxon Mobil (US) | $5,000 | $1,250 (25%) | $3,750 |

Vanguard S&P 500 ETF (VOO) | $5,000 | $1,250 (25%) | $3,750 |

Total | $25,000 | $6,250 | $18,750 |

Even though you only received $18,750 in your bank account, your taxable dividend income in India is $25,000.

You must report the full $25,000 as income.

The $6,250 withheld by the US IRS does not reduce your taxable income; instead, it is claimed separately as a Foreign Tax Credit to reduce your final tax bill.

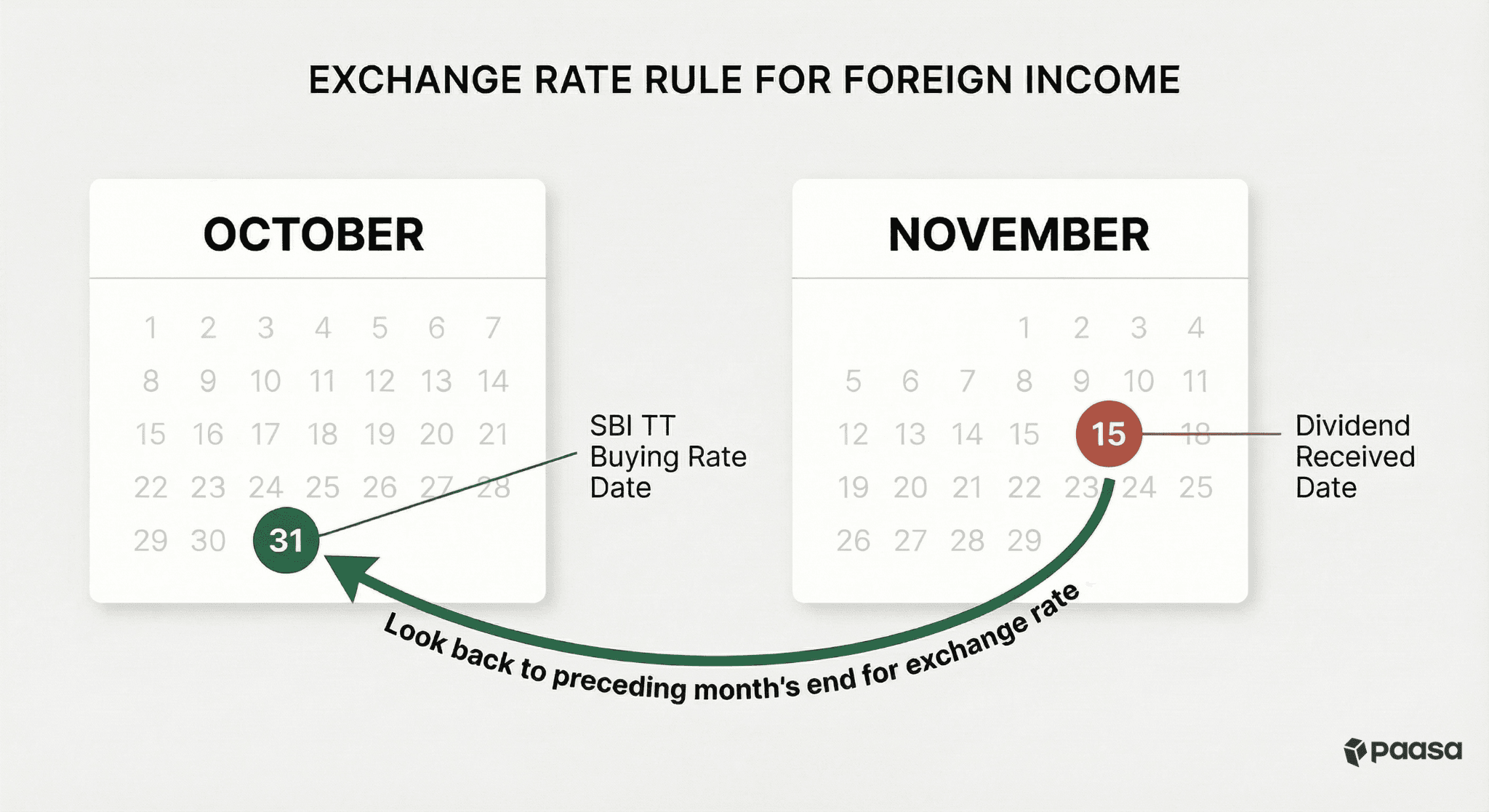

How to calculate exchange rate for foreign dividend income?

When filing your taxes in India, you must convert that $25,000 Gross Dividend into Indian Rupees using the SBI TT Buying Rate on the last day of the month immediately preceding the month in which the dividend is declared, distributed, or paid.

Example

Suppose the Exxon Mobil dividend of $5,000 (Gross) was paid on November 15th.

Rather than converting $5,000 using the exchange rate on November 15th (e.g., ₹90.20), you must use the SBI TT Buying Rate for October 31st (the last day of the preceding month).

Date | Event | Exchange Rate Source | Rate (Assumed) | Taxable Value |

Oct 31 | Reference Date | SBI TT Buying Rate | ₹89.35 | ₹4,46,750 |

Nov 15 | Dividend Paid | Market Rate | ₹90.20 | (Irrelevant for Tax) |

In this scenario, your taxable dividend income for that specific payout is ₹4,46,750. You must repeat this calculation for every single dividend payout received during the year.

How to calculate exchange rate for foreign tax credit?

When claiming foreign tax credit in India, you must convert the tax paid abroad to Indian rupees using the SBI TT Buying Rate on the last day of the month immediately preceding the month in which such tax has been paid or deducted.

Example

Similarly, suppose the $1,250 withholding tax for Exxon Mobil was deducted on November 15th.

Rather than converting $1,250 using the exchange rate on November 15th, you must use the SBI TT Buying Rate for October 31st (the last day of the preceding month).

Date | Event | Exchange Rate Source | Rate (Assumed) | Creditable Tax Value |

Oct 31 | Reference Date | SBI TT Buying Rate | ₹89.35 | ₹1,11,688 |

Nov 15 | Tax Deducted | Market Rate | ₹90.20 | (Irrelevant for Tax) |

In this scenario, the foreign tax eligible for credit is ₹1,11,688. When filing Form 67, you must report this specific INR value, not the value based on the day the money left your account.

How is foreign dividend income taxed in India?

Foreign dividend income is treated as regular income and added to your total taxable income under the head "Income from Other Sources", and taxed according to your applicable income tax slab rates.

- Taxed at Slab Rate: The entire dividend income (the gross amount before foreign taxes were deducted) is added to your other income (like salary or business income) and taxed according to your applicable income tax slab rates.

- Surcharge Cap of 15%: While high earners in India can face a surcharge of up to 25% on their income tax, the surcharge on dividend income is capped at 15%.

Are foreign dividends subject to surcharge and cess?

Yes, foreign dividend income is subject to surcharge and cess on top of the base tax rate (which is your applicable income tax slab rate). But the surcharge on dividend income is capped at 15%.

Surcharge

While the surcharge on regular income can go as high as 25%, the surcharge on dividend income is capped at 15%.

Surcharge is levied on the amount of income tax at the following rates:

Range of Income | Surcharge |

Rs. 50 Lakhs to Rs. 1 Crore | 10% |

Rs. 1 Crore to Rs. 2 Crores | 15% |

Exceeding Rs. 2 Crores | 25% (capped at 15% for dividend income) |

Even if your total income places you in the 25% surcharge bracket for other income (like salary), your surcharge on dividend income will not exceed 15%.

For example, if your tax liability on foreign dividends is ₹10 lakhs and you earn more than ₹2 crore per year (normally 25% surcharge), your surcharge on this specific dividend tax will still be restricted to 15%, and your tax on this dividend income with surcharge (but before cess) will be ₹11.5 lakhs (₹10 lakhs + 15% of ₹10 lakhs).

Cess

A Health and Education Cess is levied at the rate of 4% on the aggregate amount of income tax plus surcharge.

For example, if your tax liability on dividends after surcharge is ₹11.5 lakhs, the 4% cess is applied on top of this ₹11.5 lakhs. This takes your total tax liability to ₹11.96 lakhs (₹11.5 lakhs + 4% of ₹11.5 lakhs).

This is what your final tax calculation looks like:

Amount | |

Tax Liability on Dividends (A) | ₹10,00,000 |

Surcharge (B) (15% of A) | ₹1,50,000 |

Tax Liability after Surcharge (A+B) (C) | ₹11,50,000 |

Cess (4% of C) (D) | ₹46,000 |

Total Tax Liability (C+D) | ₹11,96,000 |

The surcharge is applied on the base tax liability, and the cess is applied on the tax liability after adding surcharge.

How is foreign dividend income taxed in the source country?

When you receive a dividend from a foreign company, the country where that company is based (the "source country") often has the first right to tax that income.

For example, if you hold US stocks, the US has the first right to tax the income.

This is done via Dividend Withholding Tax (DWT), which is deducted before the money even leaves the foreign country.

However, as an Indian tax resident, you are protected by Double Taxation Avoidance Agreements (DTAAs). These treaties typically "cap" the withholding tax rate, preventing the source country from charging you their full domestic rate.

Example

- Without DTAA: The US charges a flat 30% withholding tax on dividends paid to non-residents.

- With India-US DTAA: The treaty limits this rate to 25%.

Here are the withholding tax rate applicable to Indian tax residents for major jurisdictions:

Dividend Tax (at Source) | |

U.S. | 25% under DTAA |

Singapore | 0% under DTAA |

UK | 0% |

Switzerland | 10% under DTAA |

Ireland | 10% under the DTAA, or reduced to 0% at source with a valid V2 non-resident declaration, 0% for UCITS ETFs |

Japan | 10% under DTAA |

Poland | 10% under DTAA |

China | 10% under DTAA |

Germany | 10% under DTAA |

Ireland does not levy dividend withholding tax on UCITS ETFs to non-residents. This makes Ireland-domiciled (UCITS) ETFs significantly more tax efficient than their US counterparts.

DTAA benefits are available only if you file the correct paperwork with the source country. For example, to claim treaty benefits in the US, you need to submit Form W-8BEN with your broker.

To learn more about how to claim DTAA benefits, check out our guides on:

- US-India DTAA

- Singapore-India DTAA

- UK-India DTAA

- Switzerland-India DTAA

- India-Ireland DTAA

- Japan-India DTAA

- Poland-India DTAA

- China-India DTAA

- Germany-India DTAA

How to claim back withholding tax charged on dividend income

When foreign brokers deduct tax (e.g., the 25% US withholding tax), you do not get this money back as a direct refund into your bank account. Instead, you claim it as a Foreign Tax Credit (FTC) to reduce your tax liability in India.

The amount of credit you can claim is the lower of the following two:

- Foreign Tax Paid: The actual amount withheld by your broker (converted to INR).

- Indian Tax Payable: The tax you would have paid on this specific income in India.

Example

Suppose you are in the highest tax bracket (30%) with a total income exceeding ₹1 Crore. You received a gross dividend of ₹10,00,000 from your US stocks.

Amount | |

Gross Dividend Income (A) | ₹10,00,000 |

Foreign Tax Paid (25% of A) (B) | ₹2,50,000 |

Indian Tax Liability | |

Base Tax (30% of A) (C) | ₹3,00,000 |

Surcharge (15% of C) (D) | ₹45,000 |

Cess (4% of (C + D)) (E) | ₹13,800 |

Total Indian Tax Liability (C + D + E) (F) | ₹3,58,800 |

Foreign Tax Credit (Lower of B or F) (G) | ₹2,50,000 |

Net Tax Payable in India (F - G) | ₹1,08,800 |

Your total tax liability in India is ₹3,58,800. The ₹2,50,000 you already paid to the IRS is adjusted against your Indian tax liability as foreign tax credit, and you only owe the remaining balance of ₹1,08,800 to the Indian tax department.

To claim the Foreign Tax Credit (FTC) you need to file Form 67 on the Income Tax Portal before you file your actual Income Tax Return (ITR).

When filing Form 67, you will need to upload proof of tax deduction, such as your broker’s Year-End Statement or Form 1042-S (for taxes paid in the US).

Once Form 67 is submitted, you can proceed to file your ITR (typically ITR-2 or ITR-3). You must fill two specific schedules:

- Schedule FSI (Foreign Source Income): Here you report the gross income earned and the tax paid abroad.

- Schedule TR (Tax Relief): This is where you claim the actual relief under Section 90. The system will automatically calculate the eligible credit based on the "lower of the two" rule (Foreign Tax Paid vs. Indian Tax Payable).

What are the implications of dividend tax on long term returns?

As dividends are taxed at a higher slab compared to capital gains, dividend payouts increase your tax liability and decrease your net returns.

Here’s how dividend payouts can lead to a noticeably lower rate of return over time:

1. Difference in tax rates

Dividend income is added to your total income and taxed at your slab rate.

In contrast, Long Term Capital Gains (LTCG) are taxed at a flat 12.5%.

By receiving returns as dividends rather than capital appreciation, you are effectively opting to pay more tax on that portion of your return.

2. You pay tax twice if you reinvest

If you don't need the cash and choose to reinvest your dividends (e.g., buying more shares), you pay taxes twice:

- Tax 1: You pay Income Tax immediately upon receiving the dividend.

- Tax 2: When you eventually sell the shares purchased with that post-tax dividend money, the profit is taxed again as Capital Gains.

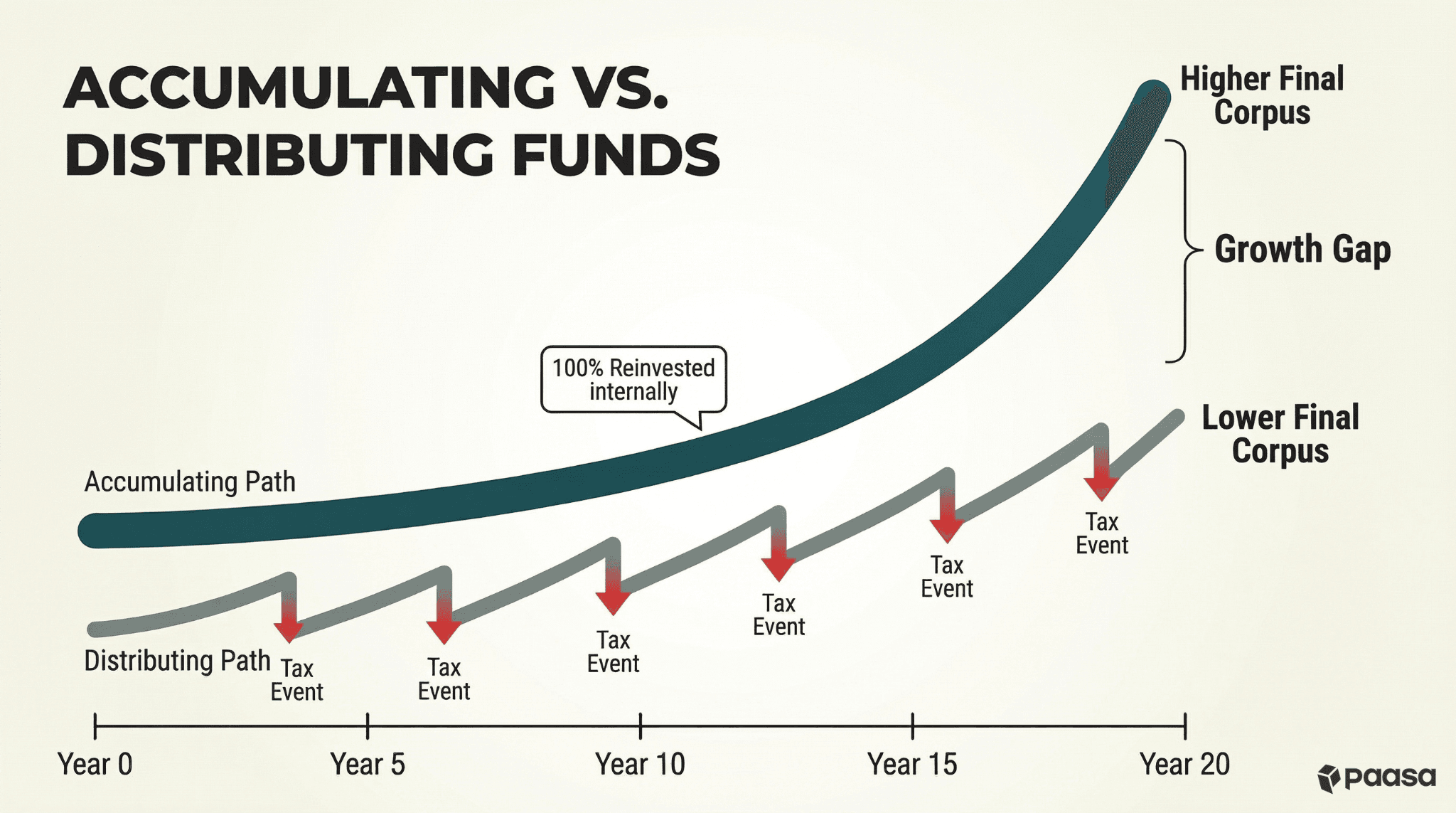

3. Reduced compounding

Investments that do not pay out dividends (like Accumulating UCITS ETFs) retain 100% of their earnings to reinvest internally.

This allows the entire pre-tax amount to compound year over year.

In a dividend-paying scenario, the tax bill removes a chunk of capital every year, significantly lowering your final corpus over a 10 or 20-year horizon.

Optimizing returns by avoiding dividend tax

The most effective way to optimize your long term returns is to change how you receive your returns.

Most US ETFs (like VOO or SPY) are "Distributing" funds. They are legally required to pay out dividends to you, which triggers a tax bill every time.

Instead of receiving payouts that get taxed immediately, you can choose funds like accumulating UCITS ETFs that automatically reinvest the money for you.

Not all funds that reinvest dividends proceeds avoid the dividend tax. UCITS ETFs are specifically structured to not trigger tax events.

UCITS ETFs offer a specific category called Accumulating funds. When an Accumulating ETF receives dividends from companies like Apple or Microsoft, it uses that cash to buy more shares internally.

Because this happens inside the fund, no dividend is ever distributed to you. This structure helps you in three ways:

- No annual tax: Since you never received a payout (not even technically), you have zero dividend income to report. You pay 0% tax on these dividends in the year they are earned.

- Lower tax rate: The dividend effectively becomes part of your capital growth. You only pay tax when you finally sell the ETF units. At that point, it is taxed as Long Term Capital Gains (12.5%) instead of your higher Income Tax Slab Rate.

No US estate tax risk: For non-residents, US assets above $60,000 are subject to the US Estate Tax. The US estate tax can go as high as 40% and wipe out a significant portion of your holdings. Since UCITS ETFs are domiciled outside the US, they completely shield your heirs from this liability while keeping you invested in the US market.

Use our US Estate Tax Calculator to find the exact tax you will have to pay.

By using Accumulating ETFs, you ensure that 100% of the dividend is reinvested to grow your wealth, rather than losing a part of it to taxes every year. It also ensures that your assets are not subject to the US estate tax.

About Paasa

Paasa is the platform used by global Indian Investors, HNIs, family offices to diversify their wealth across global markets like US, UK, China, Singapore, Switzerland, and beyond.

Paasa offers a comprehensive advisory layer that keeps your portfolio compliant and makes tax filing hassle free with:

- Dedicated relationship manager

- Ongoing remittance, FEMA and tax advisory

- Ongoing tax loss harvesting and rebalancing

- End of year tax documents

What type of documents does Paasa provide to file taxes?

At the end of the financial year, Paasa provides a ready-to-file tax package containing:

- Capital Gains Report: A clear breakdown of Short-Term vs. Long-Term capital gains, calculated specifically according to the 24-month holding rule for unlisted shares.

- Dividend & Interest Reports: Consolidated statements showing exactly how much income you earned and the tax withheld abroad, making it easy to fill Schedule FSI.

- Schedule FA Report: This is typically the hardest part of the ITR. We provide a report with the Peak Value and Closing Value of your assets in INR, calculated using the mandatory SBI TT Buying Rates, so you can simply copy-paste the numbers into your tax return.

We believe that global taxation should not come at the cost of your peace of mind. If you are investing in global equities and have doubts around taxation, FEMA, LRS, or compliance, feel free to reach out to our team.

Disclaimer

This article is intended solely for information and does not constitute investment, tax, or legal advice. The material is based on public sources and our interpretation of prevailing regulations, which are subject to change. Global investments carry certain risks, including currency risk, political risk, and market volatility. Past performance does not predict future outcomes. Please seek advice from qualified financial, tax, and legal professionals before acting.