If an Indian investor earns money from investments outside India, they usually don’t have to pay tax twice on the same income due to India’s Double Taxation Avoidance Agreements.

The tax paid abroad on income or gains originating overseas can be claimed back in India as Foreign Tax Credit (FTC) by filing Form 67.

This guide covers everything you need to know to correctly file your Form 67 and claim the maximum possible refund while staying compliant.

Table of contents

- What is Form 67?

- Who needs to fill Form 67?

- When do I need to file Form 67?

- What documents do I need for filling Form 67?

- Can I claim full credit for all taxes paid abroad using Form 67?

- Do I need to file form 67 if I have overseas holdings but paid no taxes abroad?

- Common mistakes global investors make around Form 67

- How Paasa helps in filing Form 67

- FAQs

What is Form 67?

Form 67 is the mandatory statement required for any resident taxpayer who wants to claim a credit for taxes paid in a country outside India.

Whether the foreign tax was paid via deduction (like withholding tax on dividends) or paid directly by you, you must furnish this form to the Income Tax Department to legally claim the credit.

Who needs to fill Form 67?

You are required to file Form 67 if you are a resident taxpayer in India and have paid taxes in a foreign country (whether by deduction at source or direct payment) and wish to claim a Foreign Tax Credit (FTC) against your Indian tax liability.

Note: You must also submit Form 67 if you carry backward a loss from the current year that results in a refund of foreign tax for which you had claimed a credit in any previous year.

When do I need to file Form 67?

You must file Form 67 electronically on the Income Tax e-filing portal before filing your Income Tax Return (ITR).

You are technically allowed to submit the form up until the end of the Assessment Year (March 31st). But this is useful only in cases where you are filing a Updated Return (ITR-U) and need to make changes in your Form 67.

Practically, you need to submit Form 67 before you file your ITR. This is because your ITR form requires you to input the details of the tax credit. If Form 67 is not already in the system, the tax department's automated processing may reject your claim.

What documents do I need for filling Form 67?

To successfully file Form 67 and claim your Foreign Tax Credit (FTC), you need to gather the required documents that serve as proof of the tax paid abroad.

These documents generally do not need to be uploaded directly with the form (except for the proof of tax payment/deduction which is often attached), but you must have them ready to extract accurate details and produce them if the tax department sends a query.

1. Proof of Foreign Tax Paid or Deducted

You must provide official evidence of the tax amount. Acceptable documents include:

- Certificate from the Foreign Tax Authority: An official statement or certificate issued by the tax department of the foreign country specifying the nature of income and the exact amount of tax paid.

- Certificate from the Employer/Withholder: A TDS certificate or a statement from the entity responsible for deducting the tax (e.g., your foreign employer or the foreign bank where you hold stocks).

- Self-Signed Statement: If you cannot obtain the certificates mentioned above, Rule 128 allows you to submit a statement signed by yourself. However, this must be accompanied by:

- An acknowledgement of online tax payment, a bank counterfoil, or a challan (if you paid the tax directly).

- Proof of deduction (like a bank statement or pay slip) if the tax was withheld at the source.

2. Income Details and Tax Returns

- Foreign Tax Return: A copy of the income tax return you filed in the foreign country (if applicable).

- Nature of Income Breakdown: You need a clear breakdown of the income source (e.g., Salary, Dividend, Rental Income, Capital Gains) to correctly map it in the form.

- Alignment with ITR: Ensure the figures you enter in Form 67 match exactly with Schedule FSI (Foreign Source Income) and Schedule TR (Tax Relief) in your main Income Tax Return. Discrepancies here are the most common cause of processing errors.

3. Currency Conversion Records

Since foreign taxes are paid in foreign currency (e.g., USD, GBP), you must convert them into Indian Rupees (INR) for the form.

- You must use the Telegraphic Transfer Buying Rate (TTBR) of the State Bank of India (SBI).

- Use the rate from the last day of the month immediately preceding the month in which the tax was paid or deducted.

- Example: If tax was deducted on June 15th, you must use the SBI TTBR rate from May 31st.

- Tip: Keep a screenshot or a simple calculation sheet of the rate used for your records.

Technical Requirements

- Format: All supporting documents that need to be uploaded should be scanned and converted into PDF format.

- Language: If your documents are in a foreign language (other than English), it is legally required to provide a certified English translation to avoid rejection.

- Verification: You will need your Digital Signature Certificate (DSC) or an Electronic Verification Code (EVC) (via Aadhaar OTP or Net Banking) to verify and submit the form online.

Can I claim full credit for all taxes paid abroad using Form 67?

Not always.

Under India's "Ordinary Credit Method" (Rule 128), the Foreign Tax Credit (FTC) is adjusted only against the tax liability on that specific foreign income, not your total tax bill.

The credit you can claim is restricted to the lower of:

- Actual US Tax paid (25%)

- Indian Tax payable on that specific income

In the rare case where your Indian tax liability on the income is less than the tax withheld above, you will only get foreign tax credit equal to the Indian tax liability.

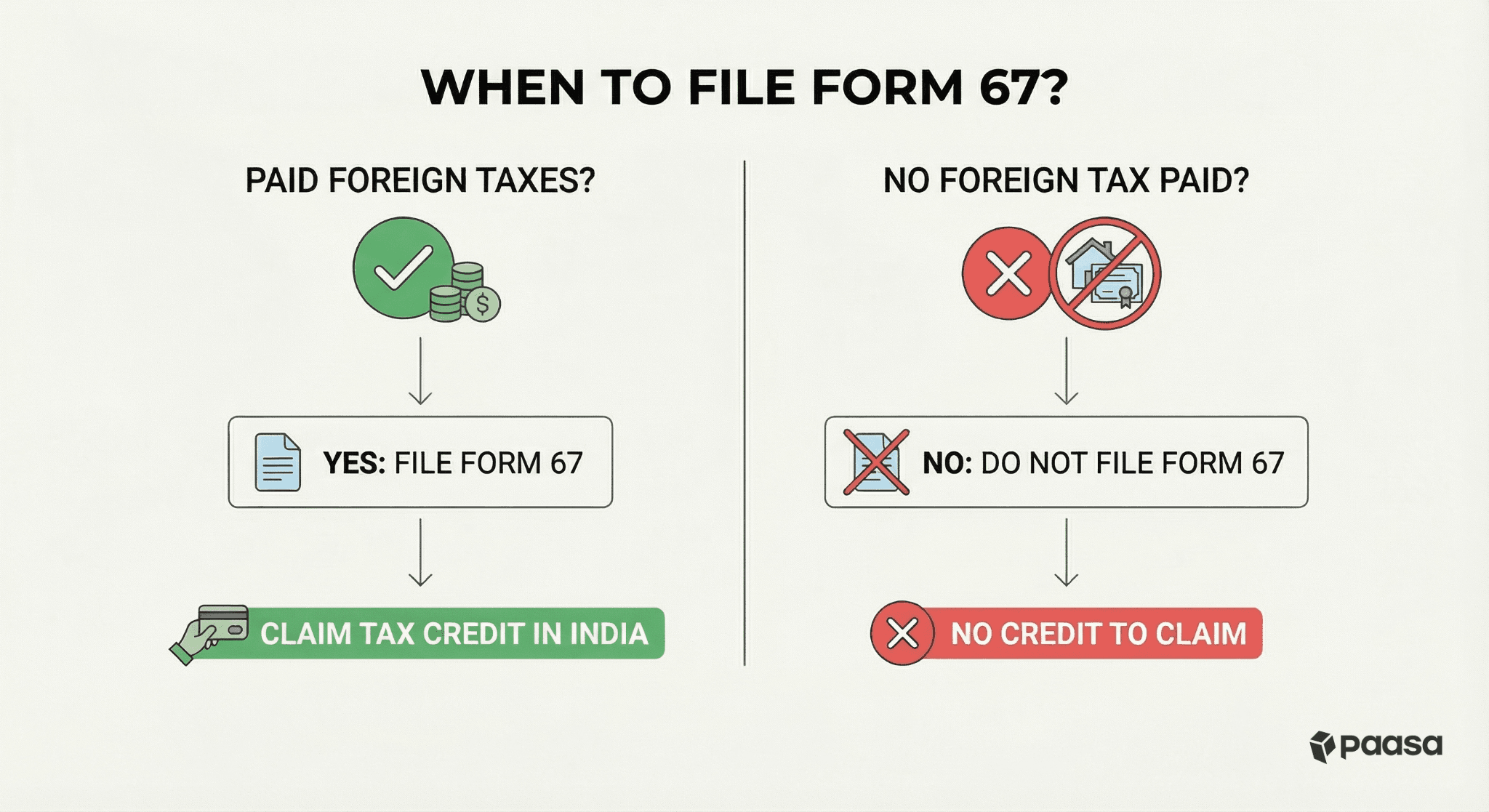

Do I need to file form 67 if I have overseas holdings but paid no taxes abroad?

No.

You only need to file Form 67 if you have actually paid taxes in a foreign country and want to claim a credit for them in India.

If you hold foreign assets but have paid no foreign taxes, you do not need to file Form 67.

This generally happens in two cases:

- No Income Generated: You simply held the asset (like accumulating UCITS ETFs) throughout the year without selling any shares or receiving any dividends.

- Income Generated but Tax-Exempt Abroad: You earned income, but the foreign country does not tax that specific type of income for non-residents.

- Example: If you sell US stocks or Ireland-domiciled ETFs, the US/Ireland does not charge Capital Gains Tax to non-residents.

In these cases, there is no credit to claim, so Form 67 is not required.

⚠️Do not confuse this with "Schedule FA"

While you might skip Form 67, you generally cannot skip Schedule FA (Foreign Assets).

Many investors confuse these two requirements:

- Form 67 is for Tax Credit (Optional, only if you paid foreign tax).

- Schedule FA is for Reporting Assets (Mandatory, even if you earned zero income).

If you hold even a single share of a foreign company (like Apple or Tesla), you must declare it in Schedule FA of your Income Tax Return, regardless of whether you made a profit or paid any tax.

Failure to disclose foreign assets in Schedule FA can lead to severe penalties (₹10 Lakhs) under the Black Money Act.

Common mistakes global investors make around Form 67

The most frequent issues usually stem from small, unintended errors in calculation or timing that slip through during the filing process.

Filing Form 67 after the ITR

While the law technically allows for late filing, the automated processing system at the Central Processing Centre (CPC) ignores the credit if Form 67 is not on record when your ITR is processed.

Not filing your Form 67 before your ITR can result in your tax credit getting denied and will ultimately require you to file an updated Income Tax Return.

Skipping DTAA Paperwork in the Source Country

Many investors forget to regularly file the necessary tax residency documents (like the W-8BEN form for US stocks and ETFs) with their foreign broker. Without this, the foreign country may deduct tax at a higher standard rate instead of the lower treaty rate.

For example, the US deducts 30% dividend withholding tax by default, but Indians are subject to a lower 25% dividend withholding tax because of the US-India DTAA.

While it is technically possible to claim back the higher tax paid, it might result in unnecessary back and forth with the income tax department as your initial FTC claim might get rejected.

Manual Calculation Errors

Filing Form 67 manually without expert support can lead to errors as the form demands specific data points that are not always obvious.

Here are the most common types errors global investors face when filing Form 67:

- Exchange Rate Errors: Using the wrong exchange rate for calculation of capital gains or tax paid abroad is a frequent trigger for scrutiny.

- Mismatching Figures: If the tax deducted figure in Form 67 differs from the figure in Schedule FSI of your ITR, the system flags it.

These small discrepancies can lead to defective return notices, increased scrutiny from the Assessing Officer, and potential penalties for misreporting.

How Paasa helps in filing Form 67

Paasa is the platform used by global Indian Investors, NRIs, and family offices to diversify their wealth across global markets like US, UK, China, Singapore, Switzerland, and beyond.

Paasa’s tax advisory service offers complete tax filing support, from submitting forms for getting preferential rates under DTAAs to claiming foreign tax credit in India.

This makes compliance and tax filing hassle free with:

- Dedicated relationship manager

- Ongoing remittance, FEMA and tax advisory

- Ongoing tax loss harvesting and rebalancing

- End of year tax documents

What type of documents does Paasa provide to file taxes?

At the end of the financial year, Paasa provides a ready-to-file tax package containing:

- Capital Gains Report: A clear breakdown of Short-Term vs. Long-Term capital gains, calculated specifically according to the 24-month holding rule for unlisted shares.

- Dividend & Interest Reports: Consolidated statements showing exactly how much income you earned and the tax withheld abroad, making it easy to fill Schedule FSI.

- Schedule FA Report: This is typically the hardest part of the ITR. We provide a report with the Peak Value and Closing Value of your assets in INR, calculated using the mandatory SBI TT Buying Rates, so you can simply copy-paste the numbers into your tax return.

We believe that global taxation should not come at the cost of your peace of mind. If you are investing in global equities and have doubts around taxation, FEMA, LRS, or compliance, feel free to reach out to our team.

Disclaimer

This article is intended solely for information and does not constitute investment, tax, or legal advice. The material is based on public sources and our interpretation of prevailing regulations, which are subject to change. Global investments carry certain risks, including currency risk, political risk, and market volatility. Past performance does not predict future outcomes. Please seek advice from qualified financial, tax, and legal professionals before acting.