Table of Contents

- The AI Infrastructure Megatrend

- U.S. Large-Cap AI Leaders

- U.S. Small-Cap AI:

- China's AI Ecosystem

- The Infrastructure Layer

- Investment Strategy & Risk Considerations

- Conclusion

The AI Infrastructure Megatrend

Artificial intelligence has evolved from a novel technology into one of the most significant infrastructure buildouts in modern history.

Black Rock Investment Institute projects AI-related capital expenditure will reach $5-8 trillion through 2030, marking a transformation comparable to the transcontinental railways of the 1800s, the interstate highway system of the 1950s, and the internet backbone of the 1990s.

The 'Magnificent Seven' tech companies alone are expected to invest $414 billion in AI and data center infrastructure in 2025, with projections climbing to $430 billion in 2026.

This massive capital deployment is creating unprecedented opportunities across the entire AI value chain—from semiconductor designers to power utilities, from cloud infrastructure to specialized software providers.

What makes this investment cycle particularly compelling is its global nature.

While U.S. tech giants dominated early AI development, 2025 has witnessed the emergence of serious competitors in China and other markets, creating a more diversified and resilient investment landscape.

This blog examines AI investment opportunities across three key dimensions: U.S. markets (large-cap and small-cap), Chinese AI ecosystem, and the critical infrastructure layer powering this transformation.

U.S. Large-Cap AI Leaders: The Foundation Layer

The U.S. maintains technological leadership in AI through a combination of chip design excellence, cloud infrastructure dominance, and cutting-edge research capabilities. While these companies face higher valuations, they represent the foundational infrastructure that enables the entire AI ecosystem.

Semiconductor Powerhouses

NVIDIA (NVDA)

Despite achieving a $5 trillion market capitalization in late 2025, Nvidia remains the linchpin of AI infrastructure. The company's GPUs power the vast majority of AI training and inference workloads globally.

Analysts project revenue and adjusted EPS to grow at a 46% and 29% CAGR respectively from fiscal 2025 through 2028. Trading at 25x forward earnings, the stock appears reasonably valued given its growth trajectory and dominant market position.

Taiwan Semiconductor Manufacturing (TSM)

TSMC fabricates the most advanced AI chips for Nvidia, Apple, AMD, and others.

The company's shares gained 46.54% in 2025, hitting record highs as Q3 revenue grew 41% year-over-year, driven primarily by AI chip demand.

TSMC represents the critical manufacturing chokepoint in the AI supply chain, making it indispensable to the sector's growth.

ASML Holding (ASML)

The Dutch semiconductor equipment maker holds a monopoly on extreme ultraviolet (EUV) lithography systems, the technology required to manufacture cutting-edge AI chips. ASML's EUV machines cost $200-400 million each and are essential for producing chips below 7 nanometers.

The company projects annual revenue opportunities of €44-60 billion by 2030, with gross margins between 56-60%.

Despite geopolitical headwinds in China, ASML's technological moat makes it Europe's best-positioned candidate to reach $1 trillion in market capitalization by 2035.

Broadcom (AVGO)

Broadcom's shares rose 49% in 2025, driven by its custom AI chip designs and networking infrastructure.

The company supplies critical interconnect technology that enables AI servers to communicate at high speeds, positioning it as a key beneficiary of data center expansion.

Cloud & Software Infrastructure

Microsoft (MSFT), Alphabet (GOOGL), Amazon (AMZN), and Meta (META) form the hyperscaler quartet driving AI infrastructure spending. These companies are not just deploying AI; they're building the cloud platforms, data centers, and software frameworks that enable AI adoption across industries.

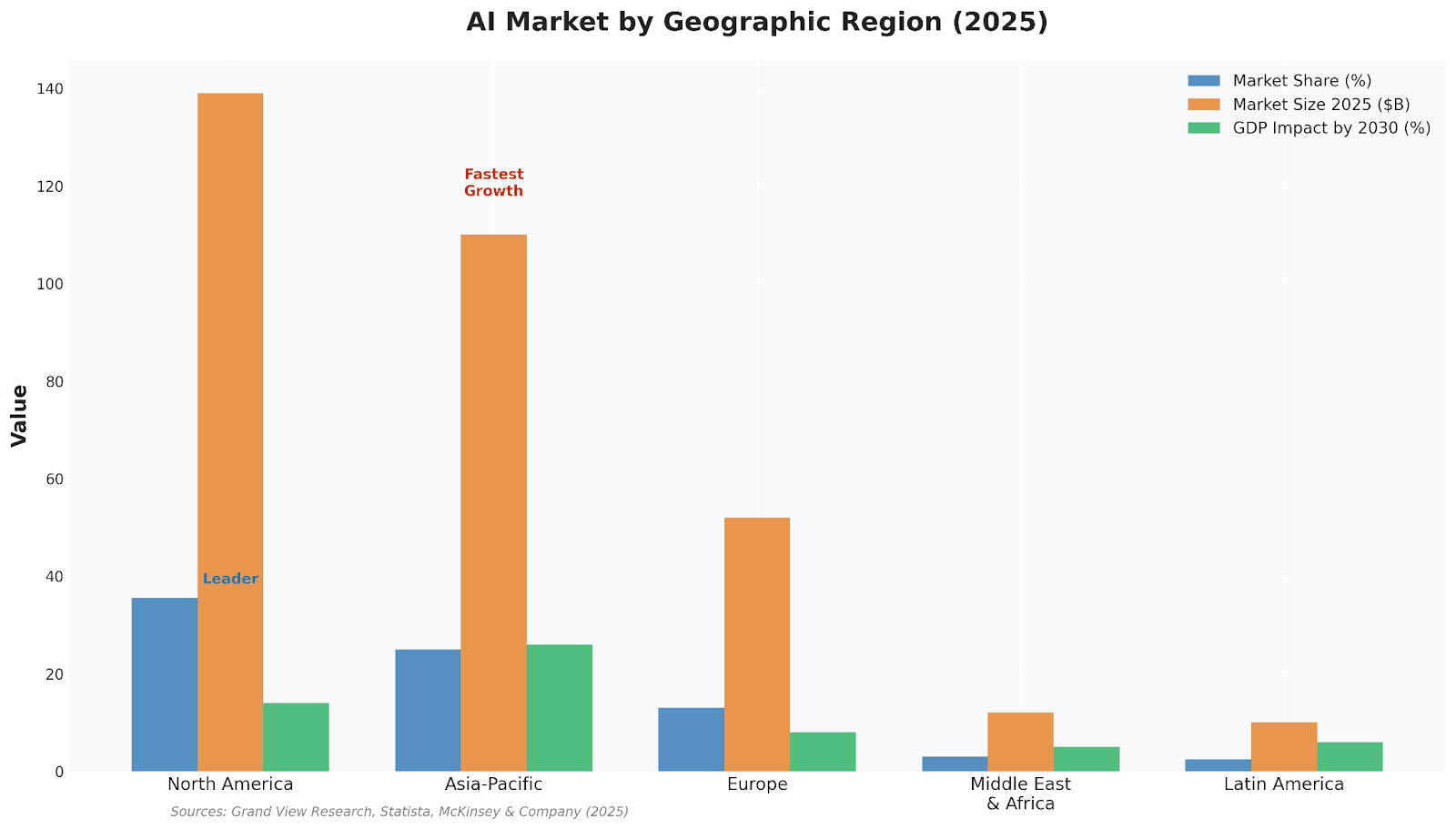

Geographic Market Distribution

U.S. Small-Cap AI: Hidden Gems with Explosive Potential

While large-cap tech captured headlines, nimble small-cap AI companies often delivered superior returns in 2025.

These specialized players address specific industry problems with targeted solutions, offering investors exposure to high-growth niches at more attractive valuations than their mega-cap counterparts.

Enterprise AI Software

C3.ai (AI)

C3.ai specializes in enterprise AI applications for predictive analytics and decision-making.

The company has secured strategic partnerships with Microsoft Azure and Google Cloud, along with major contracts including Baker Hughes.

Despite taking a 36.6% hit in early 2025, the stock rebounded 14.9% in recent months as the company demonstrated revenue growth and expanding use cases across manufacturing, energy, and defense sectors.

UiPath (PATH)

UiPath leads the robotic process automation (RPA) market with AI-embedded automation tools. The platform spans automation, orchestration, and generative AI integration, positioning it perfectly as enterprises adopt agentic AI workflows.

The company introduced specialized large language models (DocPATH and CommPATH) and maintains strategic relationships with Microsoft, Nvidia, Snowflake, and SAP. Analysts expect 9.3% revenue growth and 14.2% earnings growth for the next year.

AI-Powered Financial Services

Upstart Holdings (UPST)

Upstart revolutionizes credit underwriting by replacing traditional FICO scores with machine learning models.

In 2025, the company secured $1.2 billion in loan funding from Fortress Investment Group and expanded a $2 billion partnership with Blue Owl Capital. Over 100 bank and credit union partners now use Upstart's AI foundation model.

The company enhanced its Auto Retail software with instant AI-powered loan approvals and introduced new products including small-dollar relief loans and home equity lines of credit.

BILL Holdings (BILL)

BILL automates financial operations for small and midsize businesses using AI-powered tools for accounts payable, receivable, and expense management.

In Q2 2025, the company launched forecasting and anomaly detection features for real-time cash flow visibility, plus an AI-powered procurement module positioning itself as a comprehensive 'CFO Command Center.'

Despite a 47% share price decline in 2025, the company's 10x revenue growth since 2020 and expected 10% growth in fiscal 2026 suggest strong fundamentals.

AI Data Center Semiconductor Market

Segment | 2024 Revenue (USD B) | 2030 Revenue (USD B) | CAGR |

GPUs | $100 | $215 - $342 | ~14% |

AI ASICs | $15 - $20 | $84.5 - $104 | ~30% |

CPUs (x86 & ARM) | $8 | $12 | ~12% |

Networking | $31 | $75 | ~15% |

Memory & Storage | $55 | $100 | ~10% |

TOTAL | $209 | $457 - $492 | ~14-23% |

Voice AI & Conversational Interfaces

SoundHound AI (SOUN)

SoundHound specializes in voice, sound, and natural-language AI technologies with customers including Pandora, Krispy Kreme, White Castle, and Hyundai.

Restaurants leverage SoundHound's technology for AI-powered order-taking and reservations, while automakers integrate voice activation for navigation and safety features. With a $3.65 billion market cap, SoundHound has substantial growth runway compared to mega-cap competitors.

Five9 (FIVN)

Five9 provides AI-powered call center services with personalized AI agents emerging as a major growth driver.

The company introduced its Intelligent CX Platform powered by Five9 Genius AI on Google Cloud, alongside new AI agents tailored for Google Cloud integration. Strategic partnerships with Salesforce, Microsoft, ServiceNow, Verint, and Alphabet enable Five9 to build more tailored AI tools and improve platform integration.

Analysts expect 9.7% revenue growth and 8.3% earnings growth for the coming year.

AI Data Services

Innodata (INOD)

Innodata provides AI data services to five of the seven 'Magnificent 7' hyperscalers, all of which raised their 2025 AI capital expenditure guidance.

The company posted record Q3 2025 revenue of $62 million (20% year-over-year growth) and confirmed expectations for 45% full-year growth. Innodata launched a GenAI Test and Evaluation Platform built on Nvidia NIM microservices for LLM validation and risk benchmarking.

Despite recent volatility, the stock retained 30%+ year-to-date gains with Benzinga Edge Scores of 96.36 for Growth and 98.53 for Quality.

Tempus AI (TEM)

Tempus applies AI to healthcare, particularly precision medicine and clinical decision support. The company leads in healthcare AI applications with government and industrial backing, making it a strong contender in the specialized medical AI segment.

Emerging Technology Plays

Quantum Computing Inc. (QCI)

QCI develops quantum photonic chip technology gaining recognition from Nvidia.

The company completed its quantum photonic chip foundry and secured pre-orders from Spark Photonics and Alcyon Photonics.

With growing footprint in aerospace and biopharma applications, QCI represents a long-term quantum-AI convergence play.

Evolv Technologies (EVLV)

Evolv develops AI security screening services for large-crowd live events.

Q3 2025 revenue hit a record $42.85 million (57% year-over-year growth), with management raising full-year 2025 guidance to $145 million.

Annual recurring revenue is expected to grow over 20% year-over-year in 2026, supported by increasing security concerns and regulatory requirements for public venues.

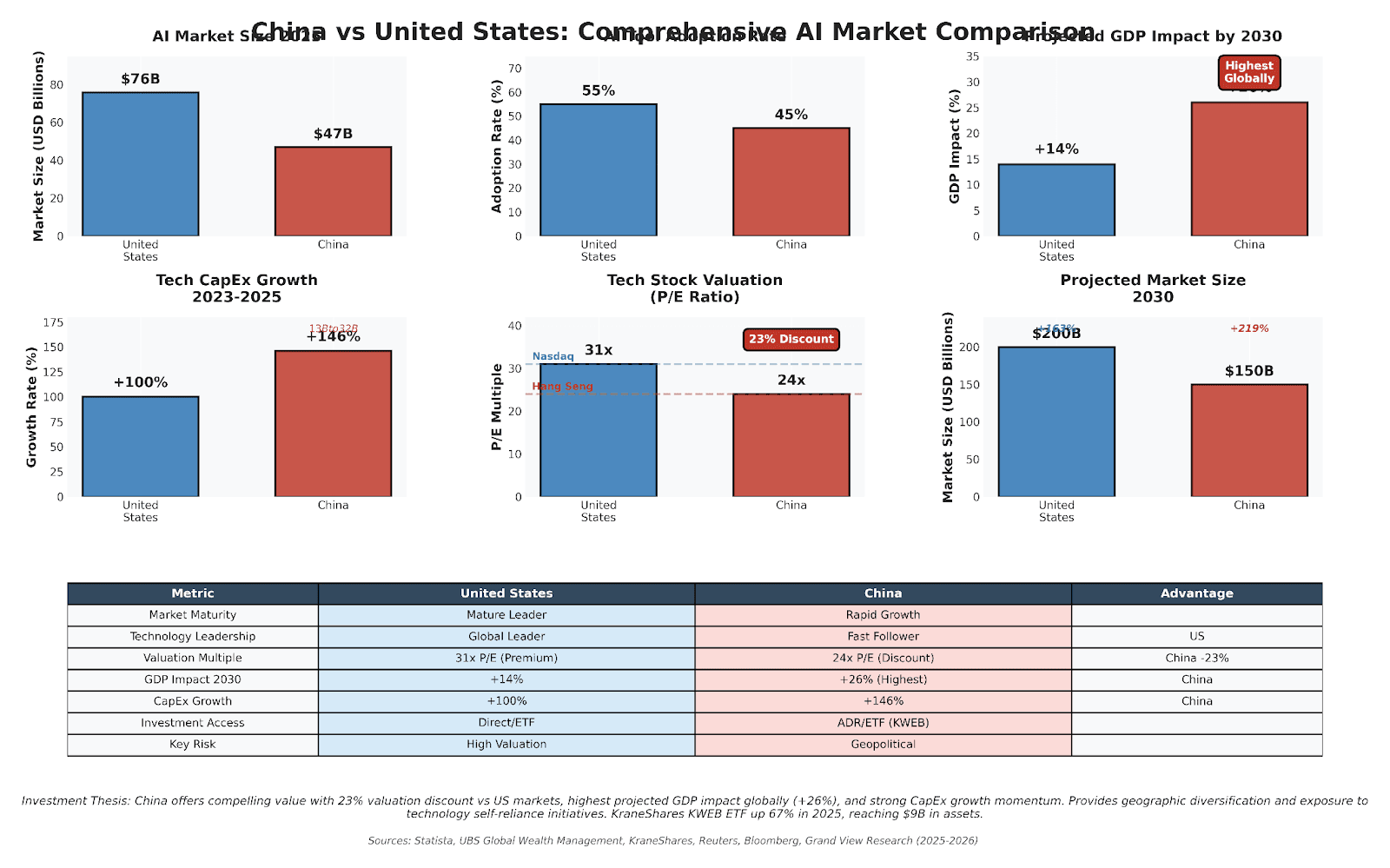

China's AI Ecosystem: The DeepSeek Disruption & Beyond

2025 marked a pivotal moment for Chinese AI. The emergence of DeepSeek, a startup that built ChatGPT-comparable models at a fraction of Western costs, shattered assumptions about China's technological capabilities and triggered massive capital flows into Chinese AI companies.

The DeepSeek R1 model demonstrated that sophisticated AI could be developed using less powerful chips and dramatically lower budgets, threatening the established narrative of American AI supremacy.

The DeepSeek Effect

DeepSeek claimed it trained its V3 model for $6 million compared to $100 million for OpenAI's GPT-4, using approximately one-tenth the computing power required for Meta's LLaMA 3.1.

This breakthrough sent shockwaves through markets in January 2025, causing Nvidia to lose $588.8 billion in market value in a single day, the largest one-day loss in stock market history. However, rather than destroying the AI investment thesis, DeepSeek's emergence validated China as a serious AI competitor and sparked renewed interest in undervalued Chinese tech stocks.

Chinese Tech Giants

Alibaba (BABA)

Alibaba shares soared 75.81% in 2025 as the company embraced AI and launched its own chatbot.

Goldman Sachs raised price targets citing improved outlook for Alibaba's cloud business, which is capturing increasing AI workloads.

The company raised $3.2 billion from a blockbuster convertible bond offering to fund AI infrastructure expansion. Alibaba's chip unit T-Head secured contracts to deploy AI chips at China Unicom's Sanjiangyuan data center, demonstrating progress in domestic semiconductor self-reliance.

Baidu (BIDU)

Baidu leads China's search market and has aggressively pivoted to AI. The company's shares jumped 16% in a single session following positive AI developments.

Arete Research Services upgraded Baidu's ADRs from sell to buy based on growth potential for its in-house chip business. Baidu's artificial intelligence chip unit has confidentially filed for a Hong Kong listing, signaling plans to capitalize on the booming demand for domestic AI semiconductors.

Tencent Holdings (0700.HK / TCEHY)

Tencent benefits from AI integration across its gaming, social media, and cloud platforms.

The company turned to the dim sum bond market for 9 billion yuan ($1.27 billion) in 2025 (its first bond sale in four years) to fund AI infrastructure investments. Total capital expenditure from major Chinese internet firms including Tencent is set to hit $32 billion in 2025, more than doubling from $13 billion in 2023.

Chinese Semiconductor Champions

U.S. export restrictions on advanced chips accelerated China's push for semiconductor self-reliance, creating explosive opportunities in domestic chipmakers:

Moore Threads (688795.SS)

Dubbed 'China's Nvidia,' Moore Threads debuted in December 2025 with eye-catching first-day gains.

The company develops GPU alternatives for AI workloads using domestically-produced technology, benefiting directly from Beijing's policy push for technological independence.

MetaX Integrated Circuits (688802.SS)

Founded by former AMD executives, MetaX jumped approximately 700% in its Shanghai debut.

The company designs AI chips competitive with Western offerings, capturing urgent demand as Chinese tech giants seek alternatives to sanctioned U.S. semiconductors.

Cambricon Technologies

Cambricon manufactures AI chips positioned as Nvidia alternatives.

The company received a significant boost when DeepSeek announced it had optimized its models to work better with domestically produced chips including Cambricon's products. This validation from a high-profile AI startup turbocharged investor interest.

Shanghai Biren Technology

Shanghai Biren's stunning stock market debut underscored China's AI rally.

The company develops high-performance AI accelerators for data center applications, with backing from major Chinese tech firms seeking to reduce dependence on foreign chips.

SMIC (Semiconductor Manufacturing International Corporation)

SMIC is China's largest chip foundry, attempting to replicate TSMC's manufacturing capabilities domestically.

Despite U.S. restrictions limiting access to cutting-edge lithography equipment, SMIC has made progress manufacturing 7nm chips and below. The company's shares surged on news of domestic chip optimization by DeepSeek and increasing government support.

Valuation Advantage

Chinese AI stocks trade at significant discounts to U.S. peers.

The Hang Seng Tech Index trades at approximately 24x earnings compared to the Nasdaq's 31x multiple.

KraneShares' KWEB ETF, which holds offshore-listed Chinese internet stocks including Tencent, Alibaba, and Baidu, has surged this year to nearly $9 billion in assets.

UBS Global Wealth Management rates China tech as 'most attractive,' citing geographic diversification benefits, strong policy backing, technological self-reliance, and rapid AI monetization.

The Infrastructure Layer: Powering the AI Revolution

AI's explosive growth has created an often-overlooked investment opportunity: the physical infrastructure enabling this transformation.

Data centers housing AI systems consume enormous amounts of electricity, a single large facility can require billions of dollars of utility investment. This power constraint is reshaping where tech companies build facilities and creating winners across the industrial supply chain.

Power Generation & Utilities

NextEra Energy (NEE)

NextEra owns America's largest electric utility (Florida Power & Light) and a massive energy infrastructure development arm.

The company partnered with Google to develop multiple gigawatt-scale data center campuses, combining NextEra's energy expertise with Google's data center development capabilities.

NextEra is also developing 2.5 GW of solar projects for Meta Platforms and exploring over $25 billion in potential transmission infrastructure investments to support AI-driven electricity demand.

Constellation Energy (CEG)

Constellation operates the largest fleet of nuclear power plants in the United States.

The company partnered with Microsoft to restart Three Mile Island Unit 1, providing carbon-free baseload power for Microsoft's AI operations.

Nuclear power's ability to provide reliable, zero-carbon electricity 24/7 makes it uniquely suited for AI data centers' constant power demands.

Dominion Energy (D)

Dominion's Virginia utility faces requests to supply 47.1 gigawatts of power to data centers, a 17% increase over the past year. Virginia hosts one of the world's largest data center markets.

The company is investing $50 billion between 2025-2029, with the bulk supporting Dominion Energy Virginia's infrastructure, including the $11.2 billion Coastal Virginia Offshore Wind project.

Electrical Infrastructure

Eaton Corporation (ETN)

Eaton manufactures electrical power distribution equipment, backup power systems, and control software for data centers.

The company recently launched detection and control systems designed to manage sudden power bursts GPU clusters create when hundreds of processors spin up simultaneously.

Eaton's data center portfolio includes uninterruptible power supplies, power distribution units, switchgear, and busway systems managing electricity from utility connections down to individual server racks.

Vertiv Holdings (VRT)

Vertiv specializes in critical power and integrated infrastructure supporting AI data center workloads.

Key offerings include AI-ready uninterruptible power supply (UPS) systems handling rapid power load changes, power distribution units (PDUs) designed for high-voltage AI requirements, and battery energy storage systems (BESS) enabling data centers to build microgrids.

Vertiv expects $4.08 EPS for 2025, with 25% year-over-year EPS growth projected for 2026.

Data Center Infrastructure

Equinix (EQIX)

Equinix dominates the interconnection market with over 250 data centers globally. Q3 2025 results showed a 10% increase in adjusted EBITDA from Q3 2024 and a 14% increase in annualized gross bookings over Q2 2025.

The company's platform enables direct, private connections between enterprises, cloud providers, and network service providers—critical for low-latency AI applications.

Digital Realty Trust (DLR)

Digital Realty is the leader in offering massive, power-heavy facilities for hyperscalers to run core infrastructure.

The company's PlatformDigital spans over 300 data centers globally. Digital Realty launched its first U.S. Hyperscale Data Center Fund in 2025 to support up to $10 billion of data center investments and partnered with Blackstone on a $7 billion joint venture to build large-scale facilities.

Storage & Memory

Micron Technology (MU)

Micron is one of three major memory producers (alongside Samsung and SK Hynix) and the only one based in the U.S. AI servers require massive amounts of high-bandwidth memory (HBM) to store and process AI models.

Chipmakers are taking all available memory production capacity, leading to worldwide shortages and driving prices higher. Micron's shares more than tripled in 2025 as revenue increased 21% to $2.63 billion in the fiscal third quarter.

Western Digital (WDC) & Seagate Technology (STX)

Both major hard drive manufacturers saw shares nearly triple in 2025. AI companies need increasing amounts of storage space for applications and data.

Data centers require hard drives, and AI companies need larger, more expensive units. Western Digital Q3 revenue rose 27% to $2.82 billion, while Seagate hit $2.63 billion (21% growth) with 80% of sales going to the data center market. Customers are signing build-to-order contracts with firm volume and price commitments.

Investment Strategy & Risk Considerations

Portfolio Construction Approach

A diversified AI investment strategy should balance exposure across the value chain:

- Core Holdings (40-50%): Established large-cap leaders like Nvidia, TSMC, ASML, and Microsoft provide portfolio stability and liquidity while capturing AI's structural growth. These companies have proven business models, strong balance sheets, and dominant market positions.

- Growth Allocation (20-30%): U.S. small-cap AI stocks offer higher risk/reward profiles. Companies like Innodata, C3.ai, UiPath, and SoundHound target specific industry verticals with compelling unit economics. Size up positions as companies demonstrate revenue acceleration and margin expansion.

- International Exposure (15-25%): Chinese AI stocks provide geographic diversification at attractive valuations. Consider a basket approach through vehicles like KraneShares KWEB ETF, or direct positions in Alibaba, Baidu, and emerging chipmakers. The valuation discount compensates for regulatory and geopolitical risks.

- Infrastructure Layer (10-20%): Utilities, power generation, and data center REITs offer defensive characteristics with AI-driven growth. These companies provide steady cash flows, dividend income, and less volatility than pure-play tech stocks while benefiting from secular AI tailwinds. NextEra, Constellation Energy, Equinix, and Digital Realty represent quality names.

Key Risk Factors

Valuation Risk

Many AI stocks trade at elevated multiples reflecting high growth expectations. The Nasdaq trades at 31x earnings compared to historical averages in the low 20s.

Concentration risk exists as well—the top 10 S&P 500 stocks now represent over 30% of index weight, with most being AI-related. Any disappointment in AI adoption rates or profitability could trigger significant multiple compression.

Competition & Technological Disruption

DeepSeek's emergence demonstrated that efficient AI development is possible with less capital and compute power than previously assumed.

This challenges the 'scale equals success' narrative that justified massive infrastructure spending.

Continued efficiency gains could reduce demand for expensive hardware and power infrastructure. Open-source models further intensify competitive dynamics.

Geopolitical Tensions

U.S.-China technology rivalry creates ongoing uncertainty. Export restrictions on advanced chips to China hurt companies like Nvidia and ASML while accelerating Chinese domestic alternatives.

The situation is fluid and policy changes could materially impact sector profitability. Additionally, investing in Chinese companies carries regulatory risk as Beijing's tech crackdown demonstrated in 2021-2022.

Power Constraints & Environmental Concerns

AI data centers' massive electricity demands strain power grids and face environmental opposition.

Utilities must invest billions in generation capacity and transmission infrastructure, with long lead times creating bottlenecks.

Nuclear power faces public opposition despite its zero-carbon profile. Regulatory delays in siting new power plants could constrain AI infrastructure buildout.

Monetization Uncertainty

While AI infrastructure spending is massive and measurable, end-user revenue remains uncertain for many applications.

Companies are investing hundreds of billions betting on future AI monetization, but the timeline and magnitude of returns are unclear. If AI productivity gains disappoint or take longer to materialize than expected, investors may question whether infrastructure spending was excessive.

Conclusion: Navigating the AI Investment Landscape

The AI revolution represents one of the most significant investment opportunities of the 21st century, with projected capital expenditures of $5-8 trillion through 2030 creating ripple effects across the global economy.

However, this is not a monolithic trade, success requires discernment in selecting companies positioned to capture specific parts of the value chain.

U.S. large-cap tech giants—Nvidia, ASML, TSMC, and the hyperscalers—provide the foundation layer with proven technology, dominant market positions, and the capital resources to lead long-term. These stocks offer the most liquid exposure and, despite elevated valuations, remain reasonably priced relative to their growth trajectories.

Small-cap U.S. AI companies present higher risk/reward opportunities for investors willing to conduct deeper due diligence. Names like Innodata, C3.ai, UiPath, and Upstart address specific industry verticals with targeted solutions, offering exposure to explosive growth in niches overlooked by mega-cap competitors. These stocks are more volatile but can deliver outsized returns as they scale.

China's AI ecosystem deserves serious consideration despite geopolitical risks. DeepSeek's disruption validated Chinese technological capabilities and triggered massive capital flows into companies like Alibaba, Baidu, Moore Threads, and Cambricon.

Trading at significant discounts to Western peers, Chinese AI stocks offer geographic diversification and exposure to the world's second-largest economy as it pursues technological self-reliance. The KraneShares KWEB ETF provides diversified exposure for investors seeking to mitigate single-stock risk.

Finally, the infrastructure layer (utilities, power companies, electrical equipment manufacturers, and data center operators) represents the most overlooked segment of the AI value chain.

These companies benefit from secular growth in electricity demand while offering defensive characteristics: stable cash flows, dividend income, and lower volatility than pure-play technology stocks. As AI scales, the physical infrastructure enabling this transformation will become increasingly valuable.

Investors should approach AI thematically with diversified exposure across geographies, market capitalizations, and subsectors.

No single company or country will capture all value creation. The winners will be those who adapt to technological evolution, navigate geopolitical complexity, and execute on large-scale infrastructure projects requiring patient capital.

The gold rush is real, but as history teaches, the smartest investors don't just stake claims on mining sites. They invest in picks, shovels, railways, and general stores. In the AI era, that means building exposure across the entire value chain: from cutting-edge chips to the power plants keeping them running.