If you are an Indian investor holding US stocks and ETFs (including RSUs), the US Estate Tax should be your top financial planning concern as it can wipe off up to 40% of your assets in the case of your death.

This blog talks about how the US Estate Tax is calculated and how you can find out your exact US Estate Tax liability using our Estate Tax Calculator.

Table of contents

- What is the US Estate Tax?

- Who needs to pay US Estate Tax?

- What assets are considered for calculating Estate Tax?

- How is the Estate Tax calculated?

- Estate Tax liability calculator

- How to reduce Estate Tax exposure to zero?

- FAQs

What is the US Estate Tax?

The US Estate Tax is a federal tax levied on the transfer of a deceased person's assets to their heirs. It is essentially a tax on the right to transfer property upon death.

It is levied at progressive rates ranging from 18% to 40% on the total market value of your US-situs assets above the exemption limit ($60,000 for non-residents).

Who needs to pay the US Estate Tax?

Anyone who has US-situs assets needs to pay the US estate tax.

If you are not a domiciled in the US, only your US-situs assets over the $60,000 exemption limit are subject to the estate tax (up to 40%).

Who is considered non-domiciled for US Estate Tax calculation?

US domiciliary status is based on intent. To be domiciled in the US, you must be physically present there with the definite intention to remain indefinitely.

If you are not based in the US and do not have the intention (and means) to remain there permanently, you are considered non-domiciled for estate tax purposes.

If you are an Indian professional working in India, or even on a visa (like H-1B or L-1) with the intent to return home eventually, the IRS views you as non-domiciled. This means you are subject to the strict $60,000 exemption limit on your US holdings.

What assets are considered for calculating the US Estate Tax?

US-situs assets owned at the decedent’s death that are subject to US estate tax include:

- US real estate: Any land or property located in the US.

- Tangible personal property: Items physically located in the US, such as automobiles, furnishings, art, and jewelry. Note that cash and currency are considered tangible personal property and will be taxable if located in the United States (e.g., in a safe deposit box).

- US stocks: Shares of corporations organized in or under US law (e.g., Apple, Microsoft), even if the share certificates or brokerage account are held outside the US.

- US debt obligations: Bonds or other debt instruments issued by US companies or US persons.

- Retirement plans: Qualified retirement plans (like 401(k)s) held in the United States.

- Business assets: Assets connected to a US trade or business, including bank accounts used for that business.

For estate tax purposes, the value of your US holdings is determined by their Fair Market Value (FMV) on the date of death

How can I calculate the total Estate Tax Liability?

The US estate tax is progressive, meaning the rate increases as the value of the estate rises. The rates range from 18% to 40%.

For non-residents, this tax applies to the value of US-situs assets exceeding the $60,000 exemption limit.

Example

Suppose you are an Indian businessperson with a globally diversified portfolio consisting of direct US stocks and US ETFs. The total value of your US assets (stocks and ETFs) is $800,000.

In case you pass away, here is what your estate tax liability will look like:

- Gross US Estate (A): $800,000

- Exemption (B): $60,000

- Taxable Estate: $740,000 (A-B)

The tax is calculated progressively on this remaining $740,000:

| Tax Rate | Tax Due |

First $10,000 | 18% | $1,800 |

Next $10,000 | 20% | $2,000 |

Next $20,000 | 22% | $4,400 |

Next $20,000 | 24% | $4,800 |

Next $20,000 | 26% | $5,200 |

Next $20,000 | 28% | $5,600 |

Next $50,000 | 30% | $15,000 |

Next $100,000 | 32% | $32,000 |

Next $250,000 | 34% | $85,000 |

Remaining $240,000 | 37% | $88,800 |

Total Estate Tax Liability | 30.6% | $244,600 |

In this scenario, out of your $800,000 hard-earned wealth, the IRS would take $244,600 (more than 30% of your total portfolio) before your family receives anything.

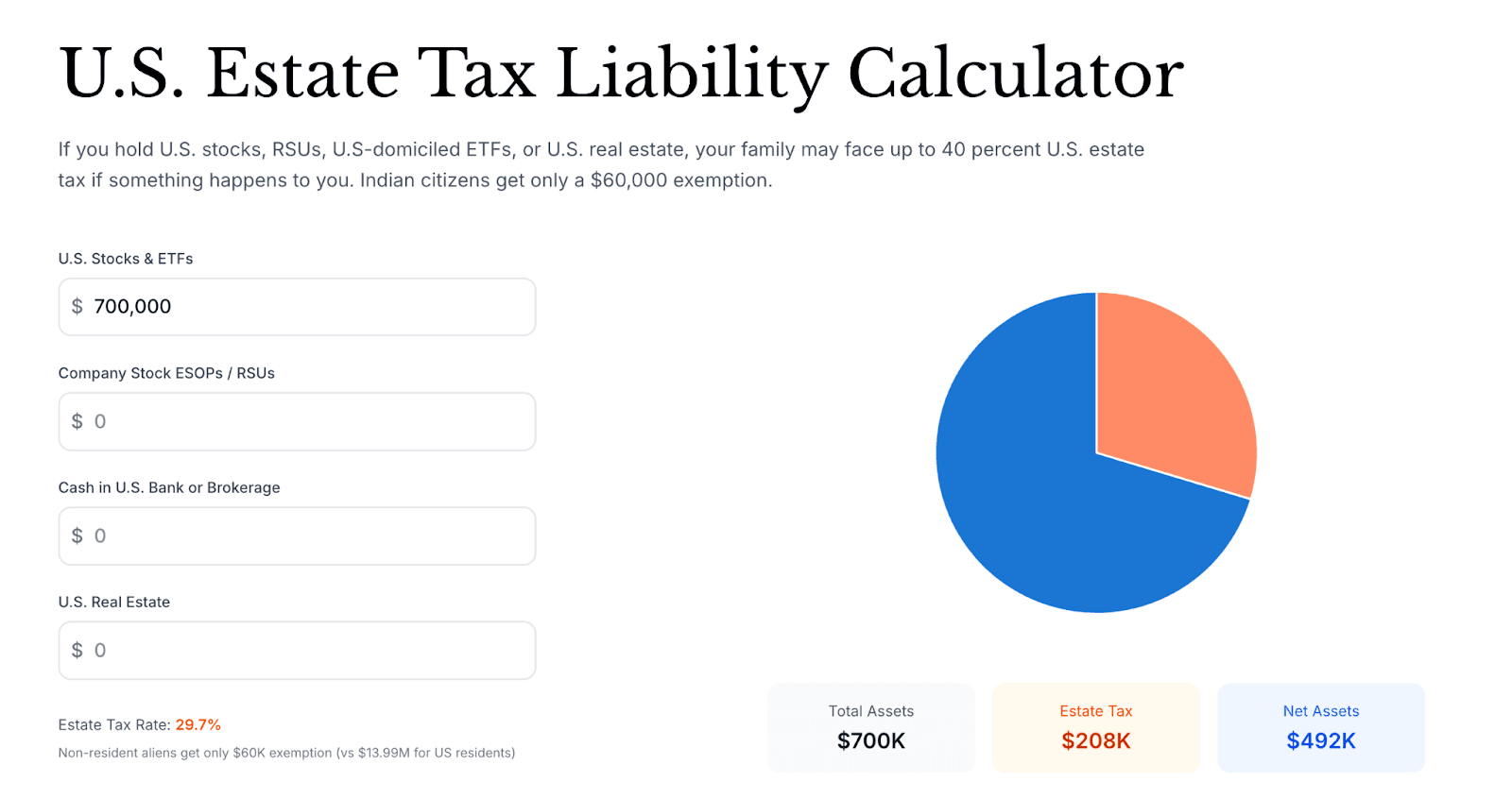

Calculate the US Estate Tax liability using our Estate Tax Calculator

You can use Paasa’s Estate Tax calculator to instantly find out your total estate tax liability based on the value of your US assets.

Simply put the value of your US assets here and our calculator will gove you the exact tax liability and tax rate.

Use our Estate Tax Calculator to find your exact liability.

How to reduce Estate Tax exposure to zero?

You can eliminate U.S. estate-tax risk by moving from U.S.-domiciled assets to UCITS ETFs, which are Europe-domiciled and not treated as U.S.-situs.

What do UCITS ETFs offer?

For Indian professionals who hold significant RSUs or U.S. equity exposure, UCITS ETFs offer a safe and compliant alternative that avoids estate tax altogether.

Here are the key advantages of the UCITS ETFs:

- 100% Estate Tax Protection: Because UCITS ETFs are domiciled in Europe (typically Ireland or Luxembourg), they are not considered US-situs assets. This means your heirs face zero US estate tax liability on these holdings, regardless of the amount.

- Direct Exposure to US Giants: UCITS ETFs hold the exact same underlying assets as their US counterparts. You can get full exposure to companies like Apple, Nvidia, Microsoft, and Amazon through an Ireland-domiciled S&P 500 or Nasdaq-100 equivalent UCITS ETF.

- Reduced Dividend Leakage: Ireland-domiciled UCITS ETFs benefit from the US-Ireland tax treaty, which reduces the internal withholding tax on US dividends to 15% (compared to the 25% or 30% you would pay as an Indian resident holding US-listed stocks directly).

- Tax-Efficient Compounding: By selecting "Accumulating" share classes, dividends are automatically reinvested within the fund. This defers Indian income tax (ordinarily taxed at your slab rate) until you sell, allowing your wealth to compound much faster.

- Institutional-Grade Safety: UCITS funds are subject to strict European regulatory oversight. A key requirement is asset segregation, where your investments are held by an independent depository, ensuring they are protected even if the fund manager faces financial issues.

- Mandatory Diversification: To protect investors from over-concentration, UCITS rules (like the 5/10/40 rule) mandate that no single holding can dominate the portfolio. This ensures your risk is spread across a broad range of companies.

- Guaranteed Liquidity & Transparency: By law, all UCITS ETFs must be open-ended, giving you the right to redeem your investment at any time. Furthermore, they must provide standardized disclosure documents (like the KIID) so you always know exactly what you own and what it costs.

UCITS vs US ETFs

Here is a comparison showing the main differences between US ETFs and UCITS ETFs.

| US-listed ETF | UCITS ETF |

Domicile | United States | Ireland or Luxembourg |

Estate-tax exposure | Subject to up to 40% US estate tax once holdings exceed USD 60,000 | No estate-tax exposure as the fund is non-US domiciled |

Dividend withholding | 25% | 15% at fund level for Irish-domiciled ETFs |

Dividend handling | Mostly distribution share classes that pay out cash dividends | Option of accumulating share classes that automatically reinvest dividends |

Compounding efficiency | Interrupted each year by dividend payout and taxation | Continuous compounding due to internal reinvestment |

Regulatory oversight | US SEC | European UCITS framework focused on investor protection |

Currency options | Primarily USD | Available in USD, EUR, and GBP listings |

More tools from Paasa

- UCITS Screener: You can use Paasa’s UCITS Screener to discover and compare UCITS-compliant investment instruments.

- Brokerage Calculator: You can calculate your brokerage costs by Paasa’s Global Brokerage Calculator.

About Paasa

Paasa is a global investing platform, designed specifically for Indian HNIs, family offices, and professionals with international wealth.

With Paasa, investors can go far beyond US equities. We enable access to UCITS ETFs, managed strategies, and access to global markets including China, Japan, Germany, Switzerland, Europe, and emerging economies. This makes it simple to build a portfolio that is globally diversified, tax-efficient, and fully compliant with Indian regulations.

Whether you are de-risking RSUs, planning estate tax protection, or building long-term cross-border allocations, Paasa provides the structure and support to secure your global wealth.

Disclaimer

This blog is for educational purposes only and should not be construed as tax, legal, or investment advice. RSU taxation, estate tax exposure, and cross-border investment rules are subject to change and may vary based on your personal circumstances.

Investing in global markets involves risks, including currency risk and market volatility. UCITS ETFs, RSUs, and other securities referenced here are used for illustration and do not constitute recommendations. Past performance is not indicative of future results.