The US estate tax is a massive wealth erosion risk that most Indian investors overlook. While US-domiciled residents enjoy an exemption of $13.99 million, the limit for non-residents is a measly $60,000.

If you are not domiciled in the US, the estate tax will be levied on your total US-situs assets over this $60,000 limit and will wipe out up to 40% of your US-situs assets upon your death.

For Indian investors with substantial holdings in the US, it is necessary to understand what are considered US situs assets, how the estate tax is calculated and collected, and who exactly is considered US ‘domiciled’.

Table of contents

- What is the US estate tax?

- Who is considered a non-resident for US estate tax purposes?

- How is the value of US holdings calculated for estate tax?

- Which assets are considered ‘US-situs’?

- How is the estate tax liability calculated?

- What happens to my brokerage account when I die?

- How are Indian investors protecting assets from the estate tax?

- Common questions Indians have about the US estate tax

- How Paasa helps in wealth management

- FAQs

What is the US estate tax?

The US Estate Tax is a federal tax levied on the transfer of assets (both tangible assets like properties and cars, and intangible assets like stocks and ETFs) to heirs after a person’s death. It is essentially a tax on the right to transfer property upon death.

It is levied at progressive rates ranging from 18% to 40% on the total market value of your US-situs assets above the exemption limit ($60,000 for non-residents).

For US citizens and "domiciled" residents (like Green Card holders living in the US), this tax is rarely a concern because they enjoy an exemption limit of $15 million (as of 2026).

However, for non-residents, the exemption limit is drastically lower at just $60,000.

The US Estate Tax is not covered by the US-India Double Taxation Avoidance Agreement, and no foreign tax credit is available in India against the US Estate Tax.

Who is considered a non-resident for US estate tax purposes?

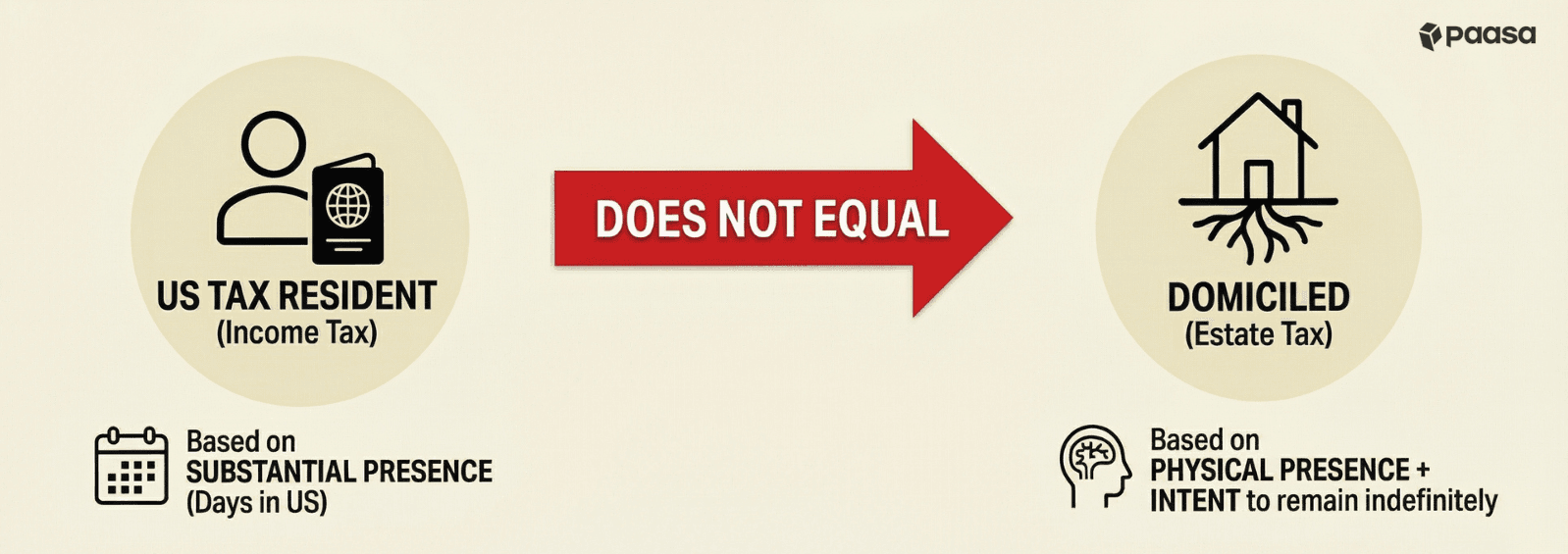

The term "resident" is defined differently for US federal income tax purposes and US federal estate tax purposes.

While Income Tax residency is determined by the "Substantial Presence Test", Estate Tax residency is determined by "Domicile."

Holding a H1B Visa or meeting the substantial presence test does not automatically make you a resident for estate tax purposes. Instead, US domiciliary status is determined by a two-prong test:

- Physical presence: You are physically present in the United States.

- Intent: You have the subjective intention to remain in the United States indefinitely.

While the first prong (physical presence) is objective and easy to prove, the second prong (intent) is a fact-specific inquiry.

Courts examine "objective manifestations" of your intent to decide if you truly planned to stay in the US forever or if you maintained deep ties to your home country.

No single factor is determinative; the courts weigh the evidence based on the following factors:

- Immigration status: Do you hold a US Green Card?

- Time spent: How much time is spent at the claimed domicile vs. abroad?

- Residence duality: A comparison between your US home and foreign residence (size, ownership vs. rental, level of furnishings).

- Asset location: The location of your personal investments and primary business assets.

- Family ties: Where do your spouse and children reside?

- Community integration: Participation in local religious organizations, social clubs, or political organizations.

- Statements of intent: What you have declared on legal documents regarding your permanent residence.

You can be a US Tax Resident for income tax purposes (paying taxes on your global income) while still being considered Non-Domiciled for estate tax purposes.

In such cases, despite paying taxes as a resident, your estate is still subject to the $60,000 exemption limit, exposing the bulk of your assets to the 40% estate tax.

Example

Suppose you are a businessperson who moves to the US for a new venture. You live there for 6 years, paying US income taxes, while maintaining businesses in both India and the US.

However, you have substantial holdings in India and your extended family remains there.

When you pass away (after living in the US for 6 years), the IRS looks at your substantial holdings and ties to India and determines that you never intended to remain in the US "indefinitely."

As a result, you get classified as a Non-Resident for estate tax purposes.

Your US assets above the $60,000 exemption are taxed up to 40%, wiping away a large part of your heirs’ inheritance.

How is the value of US holdings calculated for estate tax?

For estate tax purposes, the value of your US holdings is determined by their Fair Market Value (FMV) on the date of death, not the price at which you originally purchased them.

For example, if you bought US stocks for $50,000 and they are worth $200,000 on the day you pass away, the estate tax is calculated on the $200,000 market value.

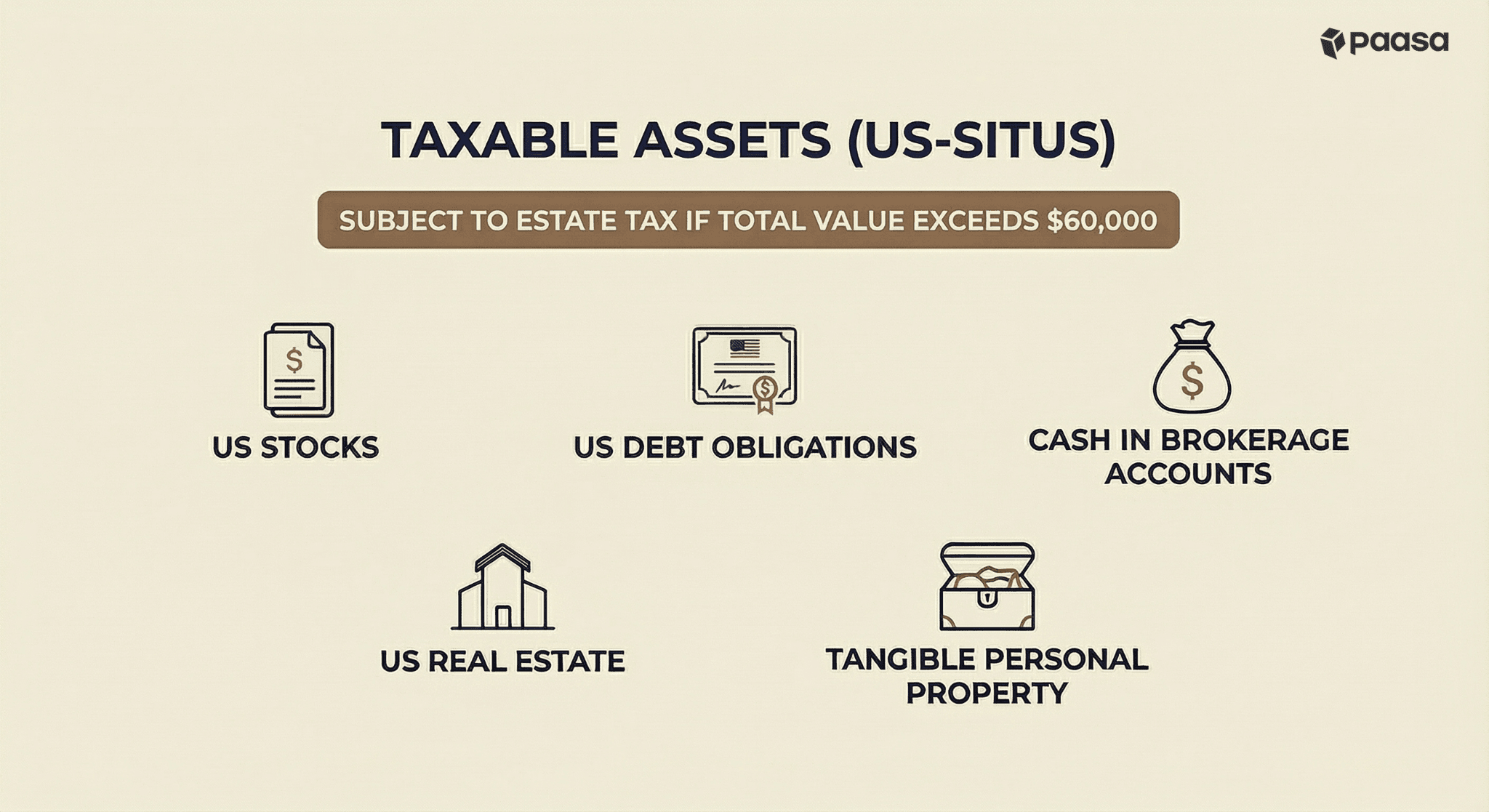

US-situs assets owned at the decedent’s death that are subject to US estate tax include:

- US real estate: Any land or property located in the US.

- Tangible personal property: Items physically located in the US, such as automobiles, furnishings, art, and jewelry. Note that cash and currency are considered tangible personal property and will be taxable if located in the United States (e.g., in a safe deposit box).

- US stocks: Shares of corporations organized in or under US law (e.g., Apple, Microsoft), even if the share certificates or brokerage account are held outside the US.

- US debt obligations: Bonds or other debt instruments issued by US companies or US persons.

- Retirement plans: Qualified retirement plans (like 401(k)s) held in the United States.

- Business assets: Assets connected to a US trade or business, including bank accounts used for that business.

To arrive at the final "taxable estate," the IRS allows you to deduct specific liabilities from the total value of your US assets.

If properly documented, these deductions can include funeral and administration expenses, claims against the estate (legitimate debts owed by the deceased), unpaid mortgages and liens secured by the US property, and certain uncompensated losses (such as theft or casualty losses) arising during the settlement of the estate.

For non-residents, the US Estate Tax is levied only on US-situs assets, and your worldwide estate is not factored into the calculation.

Warning for joint accounts: If you own a joint account with your spouse, the IRS will assume 100% of the money belonged to the first person who dies, and tax the full amount. The surviving spouse must prove their own contribution to save their share.

For an in-depth guide on how joint accounts are taxed, visit How are Joint Global Brokerage Accounts Taxed

Which assets are considered ‘US-situs’?

For non-residents, the US estate tax applies only to assets that are legally "situated" in the United States. These are known as US-situs assets.

If an asset is not situated in the US, the IRS has no claim over it.

Taxable assets (US-situs)

The following assets are considered situated in the US and are subject to the estate tax if their total value exceeds $60,000:

- US real estate: Any land, homes, or commercial property physically located in the United States.

- Tangible personal property: Items physically located in the US, such as cars, jewelry, or art.

- US stocks: Shares of US corporations (e.g., Apple, Microsoft, Tesla), regardless of where the share certificates or brokerage accounts are held. Even if you hold these stocks through an overseas broker, they are still considered US-situs assets.

- US debt obligations: Corporate bonds issued by US companies.

- Cash in brokerage accounts: Cash balances held in brokerage accounts are classified as US-situs property and can be taxed.

Non-taxable assets (non-US situs)

Assets legally situated outside the US are completely exempt from US estate tax. This includes:

- Non-US stocks: Shares of companies not incorporated in the US (e.g., Reliance, Tata, or European companies like Nestle).

- UCITS ETFs: ETFs domiciled in Europe (typically Ireland). Even if a UCITS ETF tracks the S&P 500 or holds 100% US stocks, the legal structure is Irish. Therefore, it is not a US-situs asset and is exempt from US estate tax.

- Bank deposits: Cash held in a standard US bank savings or checking account (not connected to a US trade or business) is exempt.

- Life insurance proceeds: Payouts from a US life insurance policy on the life of a non-resident are generally exempt.

Example

Suppose you are an Indian investor with a globally diversified portfolio with overseas holdings worth $700,000.

You have split your foreign investments between direct US stocks (like Tesla and US-domiciled ETFs) and Ireland-domiciled UCITS ETFs.

- US holdings: $400,000 in US stocks and ETFs (US-situs assets).

- UCITS holdings: $300,000 in Ireland-domiciled ETFs (non-US situs assets).

If you pass away, here is how the estate tax applies to these two portions of your wealth:

| Market value | Exemption status | Taxable value | Estate tax liability |

US stocks & ETFs | $400,000 | First $60,000 is exempt | $340,000 | $101,400 (~25.4% of asset value) |

UCITS ETFs | $300,000 | 100% Exempt (Not US-situs) | $0 | $0 |

Even though you held $700,000 in total assets, the $300,000 held in UCITS ETFs is completely safe.

However, the $400,000 held directly in US structures triggers a massive tax bill of $101,400. This means your heirs lose over a quarter of your US portfolio simply because of where the funds were domiciled.

For more information on how overseas assets are taxed when you sell them, visit our guide on How Global Stocks and ETFs Are Taxed for Indian Investors

How is the estate tax liability calculated?

The US estate tax is progressive, meaning the rate increases as the value of the estate rises. The rates range from 18% to 40%.

For non-residents, this tax applies to the value of US-situs assets exceeding the $60,000 exemption limit.

Here are the tax rates applied to the taxable estate amount:

Value of Taxable Estate | Tax Rate |

$0 – $10,000 | 18% |

$10,001 – $20,000 | 20% |

$20,001 – $40,000 | 22% |

$40,001 – $60,000 | 24% |

$60,001 – $80,000 | 26% |

$80,001 – $100,000 | 28% |

$100,001 – $150,000 | 30% |

$150,001 – $250,000 | 32% |

$250,001 – $500,000 | 34% |

$500,001 – $750,000 | 37% |

$750,001 – $1 million | 39% |

Over $1 million | 40% |

Example

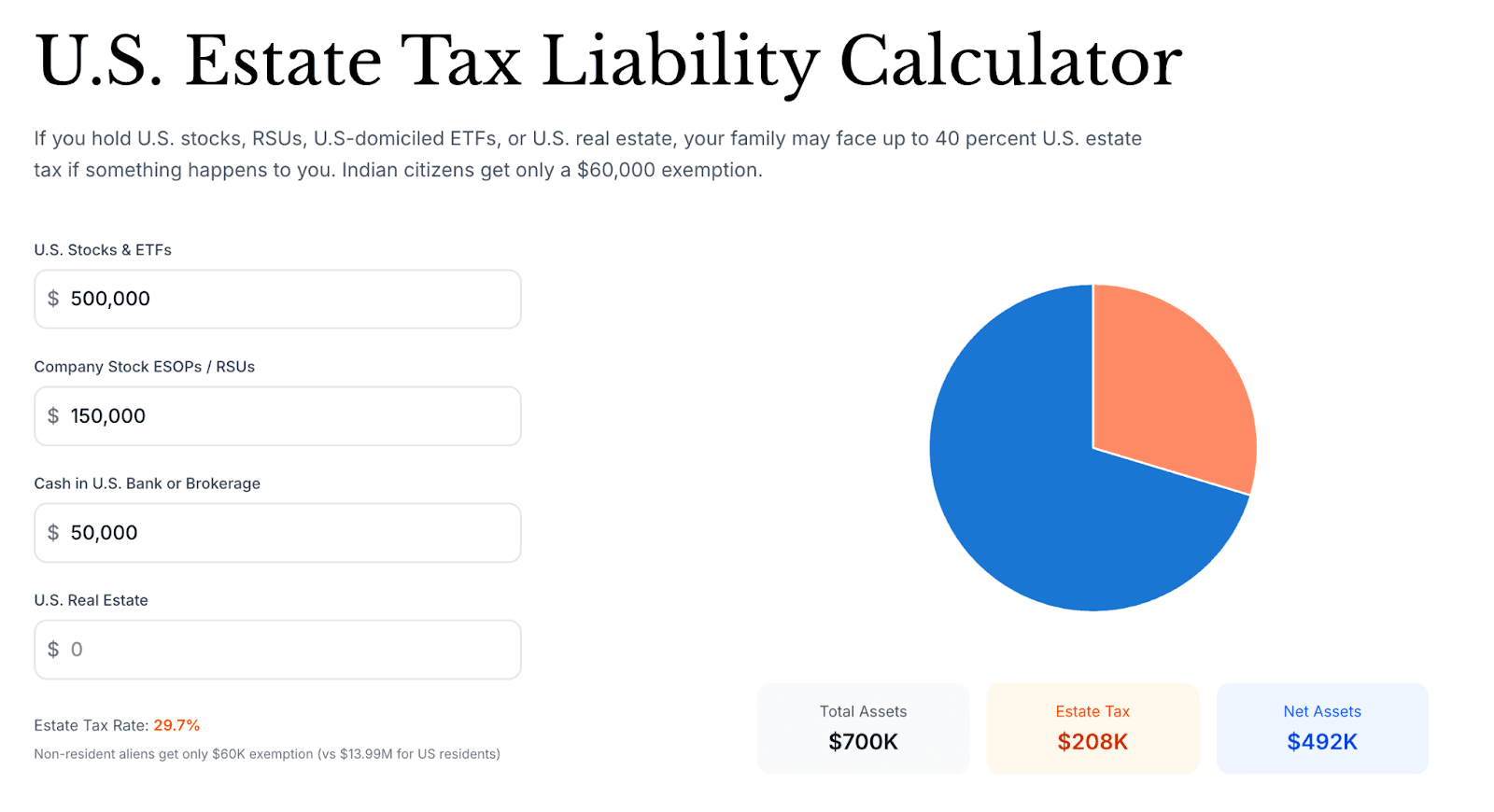

Suppose you are a software professional working in the US. Your total US assets, including stock market investments and other US-situs property, amounts to $700,000.

In case you pass away, here is what your estate tax liability will look like:

- Gross US Estate: $700,000

- Less Exemption: (-$60,000)

- Taxable Estate: $640,000

The tax is calculated progressively on this remaining $640,000:

| Tax Rate | Tax Due |

First $10,000 | 18% | $1,800 |

Next $10,000 | 20% | $2,000 |

Next $20,000 | 22% | $4,400 |

Next $20,000 | 24% | $4,800 |

Next $20,000 | 26% | $5,200 |

Next $20,000 | 28% | $5,600 |

Next $50,000 | 30% | $15,000 |

Next $100,000 | 32% | $32,000 |

Next $250,000 | 34% | $85,000 |

Remaining $140,000 | 37% | $51,800 |

Total Estate Tax Liability |

| $207,600 |

In this scenario, out of your $700,000 hard-earned wealth, the IRS would take $207,600 (nearly 30% of your total portfolio) before your family receives anything.

Use our Estate Tax Calculator to find your exact liability.

What happens to my brokerage account when I die?

When a non-US resident passes away with US assets exceeding $60,000, the custodian (e.g., Interactive Brokers) will freeze the account upon notification of death.

Step 1: Transfer to the executor

Unlike a direct transfer to heirs, the broker may transfer the assets to the estate’s legal representative (executor, administrator, or fiduciary) before the IRS estate-tax requirements are fully resolved.

- Management only: The executor gains control to manage the estate's liabilities.

- No distribution: While the executor can manage the assets, distribution to the actual heirs or beneficiaries is not allowed at this stage. The assets remain locked within the estate's control until the IRS confirms that all taxes are paid.

Step 2: Paying the tax

Before the executor can distribute the wealth to your heirs, they must obtain a transfer certificate (Form 5173) from the IRS. To get this, they must file Form 706-NA and pay the estimated tax.

This creates a cash-flow problem because the IRS typically demands payment before granting the clearance needed to release funds.

- Scenario A (ideal): The estate has enough liquid cash outside of the US brokerage account (e.g., in an Indian bank account) and can settle the tax bill upfront. Even then, the transfer certificate takes 18 to 24 months after the estate tax return has been filed with the IRS.

- Scenario B (common problem): If the heirs do not have the liquid cash to pay the tax, the executor may have to apply for a special release from the IRS to sell specific US stocks solely to pay the tax. This adds further delays to the process.

Step 3: Distribution to heirs

Once the tax is paid, the IRS processes the return, which currently takes 18 to 24 months.

- The IRS issues the transfer certificate (Form 5173).

- The executor submits this certificate to the broker.

- Only then does the broker allow the final distribution of assets from the estate to your heirs.

The requirement to pay the tax before accessing the funds creates a catch-22: your heirs need money to unlock your assets, but your assets are locked until they pay the money.

When you combine this liquidity problem with an 18 to 24-month processing delay, your family is left navigating a complex bureaucratic maze during an already difficult time.

Your financial and succession plans should ensure that your family has timely access to the wealth you built for them.

How are Indian investors protecting assets from the estate tax?

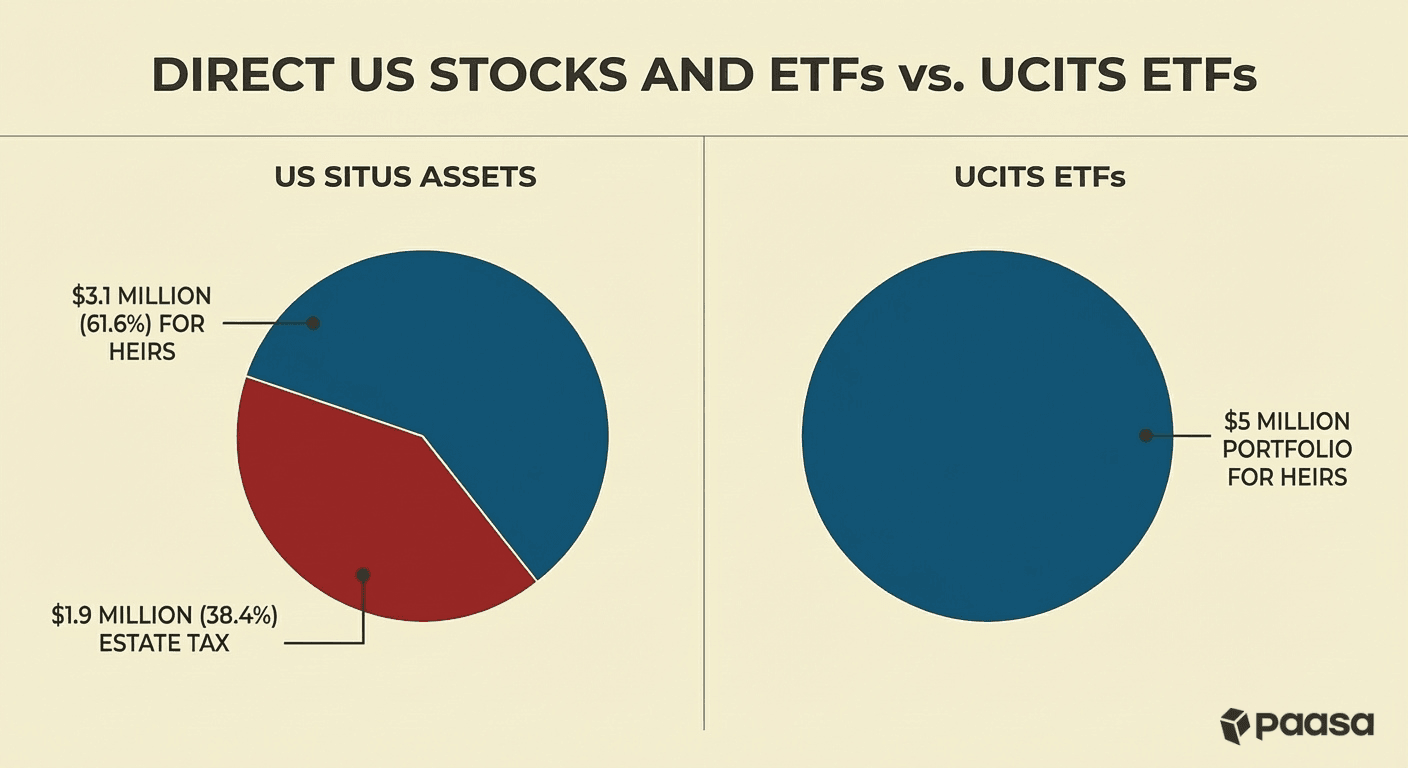

For Indian investors with significant exposure to the US markets, the estate tax acts as a massive wealth erosion mechanism.

While most investors focus on maximizing annual returns, they often overlook that the US estate tax can wipe out up to 40% of their US portfolio value upon death.

If you have built a portfolio of US-situs assets worth $5 million for your children, the estate tax will instantly claim nearly $1.9 million (38.4%) of that wealth.

The most effective way to protect your wealth is to specifically structure your assets to avoid the US estate tax.

When done right, this lets you have exposure to the US market and its growth potential, while entirely avoiding the problem of US estate tax and domicile status determination.

The US estate tax applies based on the "situs" or location of the asset, regardless of which company you invest in. If you hold US stocks or US-domiciled ETFs directly, the IRS views these as assets situated in the United States and taxes them accordingly.

However, you can invest in the exact same companies without triggering this tax by using UCITS ETFs.

UCITS ETFs are investment funds regulated by the European Union and are typically domiciled in Ireland. Because UCITS ETF are not domiciled in the US, these funds are legally considered non-US assets.

By simply switching from a US-domiciled ETF (like VOO) to an Ireland-domiciled UCITS ETF (like VUSA), you completely shield your heirs from the 40% US estate tax liability. You get the exact same exposure to US companies, but without the risk of the IRS claiming a portion of your wealth.

Use our UCITS Screener to discover and compare UCITS-compliant investment instruments.

Will I have to pay taxes while restructuring?

Yes, you will have to pay taxes if you sell your assets in the US and purchase UCITS ETFs with the proceeds.

Even with the tax hit, switching to UCITS ETFs makes sense as:

- The capital gains tax you will have to pay is lower than the estate tax (up to 40%), especially for stock or ETF units that fall under the long term capital gains classification.

- When you sell your US holdings, you will have to pay capital gains tax on the current value of your assets. But the 40% estate tax will be levied upon the appreciated value of your investments, leading to a much higher tax bill.

You can take another approach and keep your US holdings as is, and only redirect future investments into non-US domiciled structures.

But when you run the numbers, it makes much more sense to rebalance your portfolio and move away from US-situs assets, even when it results in a tax bill.

Let’s see how the returns look for both approaches.

Example

Suppose you are an Indian tax resident who currently holds $500,000 in US assets and plans to hold them for 25 years.

The Current Status:

- Total Portfolio Value: $500,000

- Short Term Capital Gain (STCG) Portion: $200,000 value ($40,000 profit). Taxed at 39% if sold today (30% slab + 25% Surcharge + 4% Cess).

- Long Term Capital Gain (LTCG) Portion: $300,000 value ($150,000 profit). Taxed at 12.5% if sold today.

You have the option of retaining your current US assets and only redirecting future investments, or selling your US holdings and moving everything to estate tax free structures.

If you sell everything today to move into UCITS ETFs, you trigger an immediate tax bill in India:

| Current Value | Profit | Tax Rate | Tax Payable | Net Funds for Reinvestment |

STCG Portion | $200,000 | $40,000 | 39% | $15,600 | $184,400 |

LTCG Portion | $300,000 | $150,000 | 12.5% | $18,750 | $281,250 |

Total | $500,000 | $190,000 | N/A | $34,350 | $465,650 |

If you sell everything and move to UCITS ETFs, you pay $34,350 in taxes today and your capital drops to $465,650.

Now, let's compare the final wealth your family receives for both approaches.

For both scenarios, we assume a modest 10% Year-on-Year (YoY) growth over the next 25 years.

- Scenario A: You switch to UCITS today (starting with $465,650).

- Scenario B: You keep the full $500,000 in US assets and your heirs pay Estate Tax later (calculated at an effective rate of 38.6%).

| Scenario A: Switch to UCITS | Scenario B: Stay in US Assets |

Starting Capital | $465,650 (Post-tax) | $500,000 (Pre-tax) |

Value after 25 Years (Compounded at 10% YoY) | $5,045,175 | $5,417,353 |

Estate Tax Calculation | $0 (UCITS are exempt) | $2,067,938 (38.6% in this case) |

Final Inheritance | $5,045,175 | $3,349,415 |

The difference in final inheritance between these two approaches is $1.69 Million ($5.04 Million vs $3.35 Million). For biggest portfolios, the estate tax hit will be even higher.

Paasa’s advisory service provides tailored guidance on restructuring your assets, helping you bypass the US estate tax while optimizing your transition to minimize the upfront tax impact and meet your financial goals. Feel free to reach out to us for personalized advice.

Common questions Indians have about the US estate tax

Is contributing to 401k a bad idea because of the estate tax if one never intends to pursue US GC or citizenship?

Having your assets in non-US situs structures is better if you do not plan to permanently settle in the US.

If you are domiciled in the US and intend to stay there permanently, a 401(k) is a good idea because you qualify for the higher US resident exemption.

However, if you plan to return to India, the 40% estate tax hit on your US-situs 401(k) effectively wipes out any income tax advantages the account originally provided.

What happens to the estate tax if my child is a US citizen?

The citizenship of your child is irrelevant for tax calculation purposes.

Estate tax is levied on the 'Estate' of the deceased, not on the person receiving the inheritance. If you are considered a non-resident for estate tax purposes, your estate will be subject to the estate tax with a $60,000 exemption.

Even if your child is a US citizen, the IRS will deduct the 40% tax from your estate first, and your child will only inherit the remaining balance.

Are there any US state estate taxes?

Yes. States like New York, Massachusetts, and Washington levy their own separate estate taxes on non-residents who own tangible property (like real estate) within their borders. However, there are no state estate taxes on investments like US stocks and ETFs

Will a will made in India accepted by the US broker?

Not automatically. US financial institutions rarely accept a foreign will without a court order.

If you only have an Indian will, your heirs will likely have to go through a legal process called "Ancillary Probate" in a US court to validate it. This often requires hiring a US attorney and paying significant fees.

To avoid this complication, it is advisable to create multiple wills; each one dealing exclusively with money or property located in the country of situs (i.e., one will for your Indian assets and a separate will strictly for your US assets).

How Paasa helps in wealth management

Paasa is the platform used by global Indian Investors, HNIs, and tech professionals with RSUs to manage and diversify their wealth across global markets and reduce exposure to the US Estate Tax via UCITS ETFs.

Paasa also offers a comprehensive advisory layer that keeps your portfolio compliant and makes tax filing hassle free with:

- Dedicated relationship manager

- Ongoing remittance, FEMA and tax advisory

- Ongoing tax loss harvesting and rebalancing

- End of year tax documents

If you are an Indian tax resident or NRI who wants to structure your assets for long term growth while keeping your future goals like investments, global travel, or your children's education in focus, feel free to reach out to our team of experts.

Disclaimer

This article is intended solely for information and does not constitute investment, tax, or legal advice. The material is based on public sources and our interpretation of prevailing regulations, which are subject to change. Global investments carry certain risks, including currency risk, political risk, and market volatility. Past performance does not predict future outcomes. Please seek advice from qualified financial, tax, and legal professionals before acting.