When you remit money to your global brokerage account in order to invest in overseas stocks and ETFs, you have to pay an upfront tax on the transaction in the form of Tax Collected at Source (TCS).

A thorough understanding of the applicable TCS rates, how the TCS is calculated, exactly who needs to pay TCS, and other regulations around TCS can help you with compliance and cash flow planning.

Table of Contents

- What is TCS?

- What is the TCS rate applicable on foreign investments?

- Who exactly is subject to this TCS?

- How is TCS different from TDS?

- Is there a way to avoid TCS?

- Can I withdraw money sent abroad for investment and spend it without remitting back to India?

- How to claim back the TCS paid?

What is TCS?

TCS (Tax Collected at Source) is an advance tax collected by the government of India over and above the transaction value when you perform specific financial transactions, such as remitting money abroad.

When you remit money abroad for foreign investments (like buying US stocks or real estate) under the Liberalised Remittance Scheme (LRS), your bank acts as an agent for the government. They collect this extra percentage over and above your transaction amount and deposit it with the tax department against your PAN.

This amount then appears as a tax credit in your Form 26AS (your tax passbook), which you can use to pay your final tax bill or claim as a refund when you file your returns.

“TCS is not an additional fee. It is simply a pre-payment of your annual income tax liability.

Example

Suppose you want to remit ₹25 Lakhs for an overseas investment, and a TCS rate of 20% is applicable on this specific transaction.

Here is how the bank calculates the total amount to be debited from your account:

| Amount | Note |

Transaction Value (A) | ₹25,00,000 | The amount you want to send abroad. |

TCS Payable @ 20% (B) | ₹5,00,000 | Collected over and above the investment amount. |

Total Amount Debited (A+B) | ₹30,00,000 | The final amount deducted from your bank account. |

The ₹5 Lakhs is not deducted from the money you are sending. Instead, it is collected as an additional fee.

The recipient still gets the full ₹25 Lakhs worth of foreign currency, but a total of ₹30 Lakhs is deducted from your account.

What is the TCS rate applicable on foreign investments?

For Indian residents investing in global stocks and ETFs, the Tax Collected at Source (TCS) rate is 20%, applicable only on amounts exceeding ₹10 Lakhs in a financial year.

This means that for the first ₹10 Lakhs you remit abroad in a year, there is zero TCS. The 20% tax applies only to the portion of your remittance that crosses this threshold.

How the limit is calculated

The ₹10 Lakh limit is cumulative for the entire financial year (April 1 to March 31). It applies to the total of all your LRS transactions combined, not just investments.

This means if you have already used ₹4 Lakhs for a family trip and ₹2 Lakhs for a gift, you have utilized ₹6 Lakhs of your limit. If you then transfer money for investments, the exemption will only apply to the remaining ₹4 Lakhs before the 20% tax begins.

Example

Suppose you plan to invest ₹40 Lakhs in US ETFs this year. You make this investment in a single transaction and have not sent any other money abroad this year.

Here is how the tax is calculated:

Particulars | Amount |

Total Investment Amount (A) | ₹40,00,000 |

Exemption Limit (B) | ₹10,00,000 |

Amount Subject to TCS (C = A - B) | ₹30,00,000 |

TCS Payable @ 20% (D = C * 20%) | ₹6,00,000 |

Total Funds Debited (E = A + D) | ₹46,00,000 |

The ₹6 Lakhs you paid as TCS will appear in your Form 26AS, and you can claim it as a refund when you file your returns.

For more information on the TCS rates applicable when sending money abroad for different purposes under the Liberalised Remittance Scheme (LRS), read our detailed guides here:

- Complete LRS Guide for Indians

- LRS for Global Investments: Stocks, ETFs, Real Estate & More

- How to Send Money Abroad for Education under LRS

- LRS Guide for Medical Treatment Abroad

- LRS for Travel - Guide for Indians

- LRS for Maintenance of Family Overseas

- How Indians Can Buy Property Abroad Under LRS

- Avoid FEMA Violations in Gifts and Donations (LRS Rules)

Who exactly is subject to this TCS?

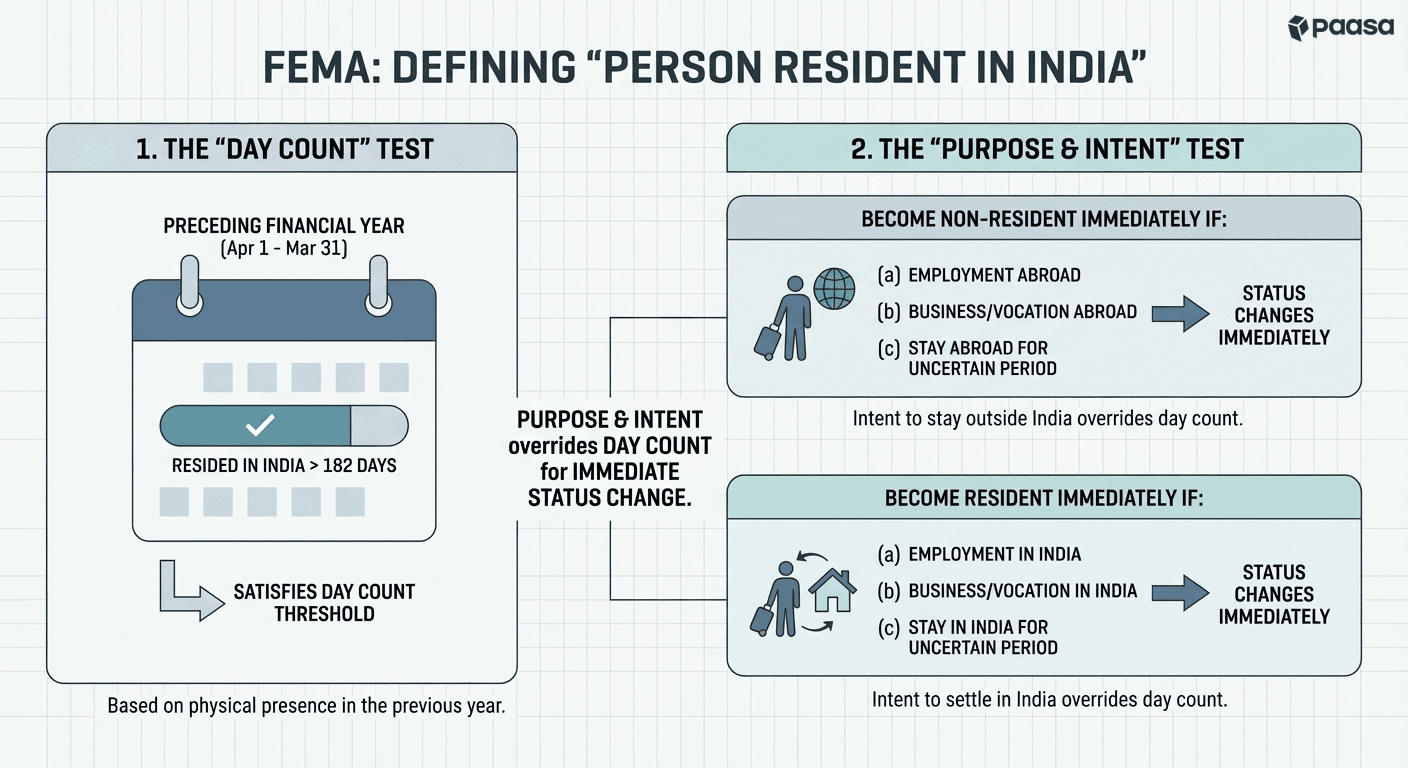

TCS on foreign remittances applies to "Persons Resident in India" as defined under the Foreign Exchange Management Act (FEMA).

The definition of a resident under FEMA is distinct from the Income Tax Act.

While tax residency is typically based on the number of days you spend in India in the current year, FEMA looks at a combination of your physical presence in the preceding year and your intention for the current stay.

For FEMA regulations, a "Person Resident in India" is defined by a two-part test:

1. The "day count" test

You must have resided in India for more than 182 days during the course of the preceding financial year (April 1 to March 31).

2. The "purpose & intent" test

Even if you satisfy (or fail) the day count test, your status changes immediately if your intent changes. The definition explicitly excludes or includes people based on their purpose:

- You become a non-resident immediately if: You leave India for:

- (a) Taking up employment outside India,

- (b) Carrying on a business or vocation outside India, or

- (c) Any other purpose indicating your intention to stay outside India for an uncertain period.

- You become a resident immediately if: You come to or stay in India for:

- (a) Taking up employment in India,

- (b) Carrying on a business or vocation in India, or

- (c) Any other purpose indicating your intention to stay in India for an uncertain period. (This means if you return to India to settle down, you become a resident immediately, regardless of whether you spent 182 days here last year.)

The Act specifically notes that if you come to India for a purpose other than employment, business, or staying for an uncertain period (e.g., a specific holiday, medical treatment, or study course), you generally do not become a resident, provided your stay remains defined and temporary.

If you are a resident Indian using the Liberalised Remittance Scheme (LRS) to send money abroad, you are subject to these TCS rules.

Who is not subject to TCS?

- NRIs (Non-Resident Indians): NRIs do not use the LRS to send money abroad. Instead, they remit funds from their NRO or NRE accounts, which are governed by different RBI regulations. Therefore, the 20% TCS on LRS does not apply to them.

- Foreign Entities: Foreign companies or foreign citizens (who are not FEMA residents) are not subject to LRS limits or TCS.

How will the bank know when I become a FEMA resident?

The bank determines your residency status based on self declarations and the type of bank account you hold. They do not track your physical location or count your days in the country.

- Resident Savings Account: If you hold a standard savings account, the bank treats you as a Resident. Any international transfer from this account is automatically classified under LRS, triggering the applicable TCS.

- NRE/NRO Account: If you hold an NRE or NRO account, the bank treats you as a Non-Resident. Transfers from these accounts do not fall under LRS.

It is your legal obligation to inform your bank whenever your residency status changes.

- If you return to India: You must convert your NRE/NRO accounts into Resident Savings accounts. Once this conversion happens, you will be able to use LRS, and TCS will apply to your remittances.

- If you move abroad: You must convert your Resident Savings account into an NRO account. Once this is done, you stop using LRS, and TCS will no longer apply to your transfers.

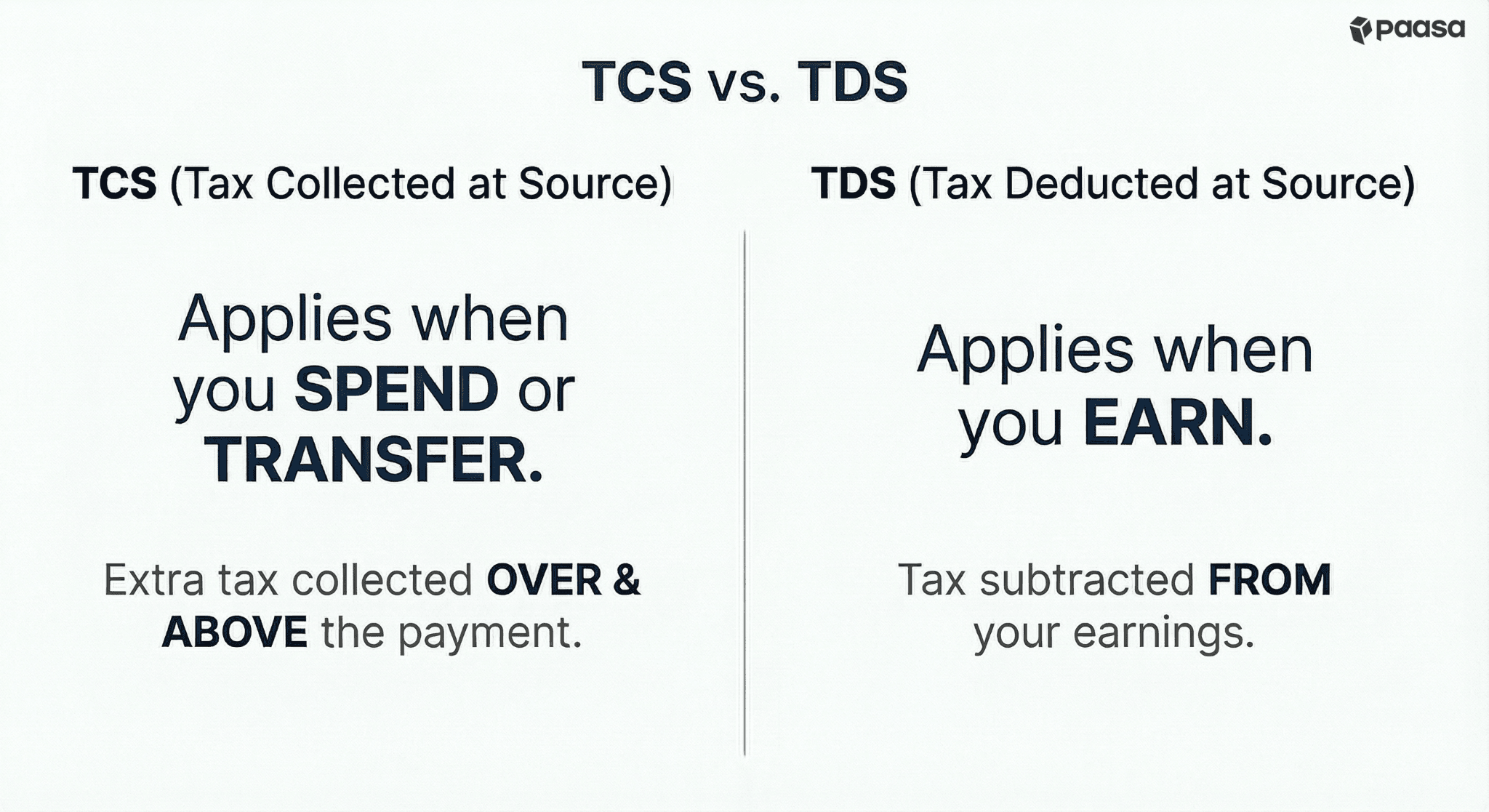

How is TCS different from TDS?

While TCS (Tax Collected at Source) and TDS (Tax Deducted at Source) are both methods used by the government to collect tax in advance, they work in opposite ways and apply to different types of transactions.

The fundamental difference lies in the direction of the cash flow:

- TCS applies when you Spend or Transfer: It is an extra tax collected from you over and above the bill amount when you make specific high-value payments (like buying a luxury car or sending money abroad).

- TDS applies when you Earn: It is a portion of your income (like salary, interest, or rent) that is subtracted from your earnings before you receive the money.

Here is a breakdown of the key differences:

| TCS (Tax Collected at Source) | TDS (Tax Deducted at Source) |

Core concept | Tax collected by the receiver/seller from the payer. | Tax deducted by the payer from the receiver's income. |

Who bears the tax? | The person making the payment (Buyer/Remitter). | The person receiving the payment (Earner/Seller). |

Cash flow impact | Requires extra cash upfront in your account (Transaction Value + Tax). | Reduces the final amount hitting your account (Gross Income - Tax). |

Nature of transaction | Spending, Purchasing, or Remitting funds. | Earning Income (Salary, Interest, Fees). |

Note: Both TCS and TDS are "Advance Taxes" deposited against your PAN. You can claim credit for both when you file your annual Income Tax Return.

Example

Suppose you work as an independent consultant in India. You invoiced a client ₹55 Lakhs for a project you just wrapped up. You intend to invest the post-tax proceeds abroad in UCITS ETFs through Paasa.

Stage 1: Earning the money (TDS)

Your client deducts 10% tax (under Section 194J) before paying you. This reduces your immediate cash inflow.

| Amount | Note |

Gross Invoice Value (A) | ₹55,00,000 | The total fee you billed the client. |

TDS Deducted (B) | ₹5,50,000 | 10% tax deducted under Section 194J. |

Net Received in Bank (A-B) | ₹49,50,000 | The actual money that lands in your account. |

Stage 2: Remitting the money (TCS)

You decide to remit the full ₹49.50 Lakhs you received. Now, the bank collects tax over and above this amount.

| Amount | Note |

Remittance Amount (C) | ₹49,50,000 | The amount you want to invest abroad. |

TCS Exemption Limit (D) | ₹10,00,000 | No TCS applies on the first ₹10 Lakhs. |

Amount Liable for TCS (C-D) | ₹39,50,000 | TCS is calculated only on this balance. |

TCS Payable @ 20% (E) | ₹7,90,000 | Extra amount collected by the bank. |

Total Funds Needed (C+E) | ₹57,40,000 | Total balance required to execute the trade. |

TDS is deducted when you receive the payment, while TCS is collected as an extra fee over and above the transaction amount when you use your money to purchase something.

The ₹5.5 Lakhs (TDS) and ₹7.9 Lakhs (TCS) are not extra costs. They are advance tax payments sitting in your name. When you file your ITR, you can claim this entire ₹13.4 Lakhs as a tax credit or a refund.

Is there a way to avoid TCS?

No. If you are a resident Indian under FEMA regulations, TCS is mandatory once your remittances exceed ₹10 Lakhs.

However, if you are not an Indian resident according to FEMA, the LRS rules (and therefore TCS) do not apply to you.

For Non-Resident Indians (NRIs)

NRIs are not governed by the Liberalised Remittance Scheme (LRS). Instead, they follow separate RBI regulations for sending money out of India:

- From NRE / FCNR Accounts: There is no upper limit on repatriation. You can transfer any amount freely without LRS limits or TCS.

- From NRO Accounts: You can remit up to USD 1 Million per financial year. This is subject to certain tax clearance (Form 15CA/15CB) but is not subject to the 20% TCS that applies to LRS.

So, if you move abroad and your status changes to NRI, you essentially "exit" the TCS regime because you stop using the LRS route for your transfers.

Can I withdraw money sent abroad for investment and spend it without remitting back to India?

Yes.

As long as the money was originally remitted for a legitimate purpose (like investment) and used for that purpose, you are allowed to use the proceeds for other permitted expenses abroad without bringing the money back to India first.

This is an efficient strategy for frequent travellers as:

- If you bring the money back, you pay forex charges to convert USD to INR. Then, when you travel later, you convert INR to USD/EUR again and pay 20% TCS again.

- If you spend it directly by withdrawing the sale proceeds to a foreign bank account, you avoid the double forex conversion cost and TCS.

⚠️ Important conditions:

- Tax on Gains: Even if the money never hits your Indian bank account, you must still calculate the profit from the stock sale and pay Capital Gains Tax in India.

- The 180-Day Rule: According to FEMA rules, you cannot keep "idle" cash abroad indefinitely. If you sell an investment, you must either reinvest it or use it within 180 days. If you don't use it, you must repatriate the funds back to India.

How to claim back the TCS paid?

Since TCS is an advance tax, claiming it back is a standard part of filing your annual Income Tax Return (ITR).

The process is straightforward because the tax department already has a record of the payment linked to your PAN.

Step 1: Verify the Credit

Before filing, log in to the Income Tax Portal and check your Form 26AS (Annual Information Statement). Your bank is required to deposit the TCS and report it here. You should see the bank's name, the amount of transaction, and the TCS collected.

Step 2: File your ITR

When you file your return , there is a specific column for "Tax Collected at Source."

- In most cases, this data will auto-populate from your Form 26AS.

- If it does not, you can manually enter the details.

Step 3: Refund or Adjustment

Once the system accounts for the TCS, one of two things will happen:

- Offset: If you owe taxes (e.g., on your salary or capital gains), the TCS amount is subtracted from your bill. You only pay the remaining balance.

- Refund: If your total tax liability is lower than the TCS (and other taxes) you have already paid, the government will refund the excess amount to your bank account with interest.

Pro-Tip: Improving Cash Flow

You do not strictly have to wait until the end of the year to get the benefit of TCS.

If you are liable to pay Advance Tax (because your total tax liability exceeds ₹10,000), you can use the TCS amount to offset your quarterly advance tax installments.

For example, if you owe ₹15 lakh as an Advance Tax installment in September, but you have already paid ₹15 lakh as TCS on a foreign remittance in August, you can adjust this amount and pay zero Advance Tax for that quarter.

How Paasa helps in Taxation

Paasa is the platform used by global Indian Investors, NRIs, and family offices to diversify their wealth across global markets like US, UK, China, Singapore, Switzerland, and beyond.

Paasa offers a comprehensive advisory layer that keeps your portfolio compliant and makes tax filing hassle free with:

- Dedicated relationship manager

- Ongoing remittance, FEMA and tax advisory

- Ongoing tax loss harvesting and rebalancing

- End of year tax documents

What type of documents does Paasa provide to file taxes?

At the end of the financial year, Paasa provides a ready-to-file tax package containing:

- Capital Gains Report: A clear breakdown of Short-Term vs. Long-Term capital gains, calculated specifically according to the 24-month holding rule for unlisted shares.

- Dividend & Interest Reports: Consolidated statements showing exactly how much income you earned and the tax withheld abroad, making it easy to fill Schedule FSI.

- Schedule FA Report: This is typically the hardest part of the ITR. We provide a report with the Peak Value and Closing Value of your assets in INR, calculated using the mandatory SBI TT Buying Rates, so you can simply copy-paste the numbers into your tax return.

We believe that global taxation should not come at the cost of your peace of mind. If you are investing in global equities and have doubts around taxation, FEMA, LRS, or compliance, feel free to reach out to our team.

Disclaimer

This article is intended solely for information and does not constitute investment, tax, or legal advice. The material is based on public sources and our interpretation of prevailing regulations, which are subject to change. Global investments carry certain risks, including currency risk, political risk, and market volatility. Past performance does not predict future outcomes. Please seek advice from qualified financial, tax, and legal professionals before acting.