After years of concentrated dominance by the Magnificent 7 technology stocks, 2025 marked a watershed moment in global capital allocation.

Institutional money is on the move, and understanding these flows is critical for positioning portfolios for the next market cycle.

This analysis examines where the world's biggest pools of capital are flowing, from US small caps to emerging market equities and the evolving role of digital assets.

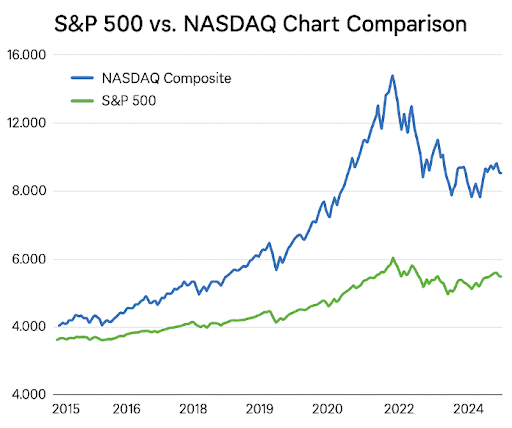

The S&P 500 and NASDAQ charts show that while headline indices remain elevated, recent gains have been increasingly concentrated in a narrow set of mega-cap stocks.

This divergence signals maturing leadership, where upside momentum is slowing at the index level even as liquidity begins rotating into broader segments of the market, setting the stage for style and regional diversification rather than a full risk-off move.

Table of contents

- Part 1: The Valuation Gap That Changed Everything

- Part 2: The Emerging Markets Renaissance

- Part 3: Europe's Quiet Strength

- Part 4: Commodities - The Silent Companion to Equity Liquidity

- Part 5: Cryptocurrency's Institutional Maturation

- Final Recommendations: Preparing for the Next Cycle

Part 1: The Valuation Gap That Changed Everything

For years, the Magnificent 7 stocks dominated market returns.

Their collective weight in the S&P 500 reached approximately 40%, creating a concentration unprecedented in modern markets. However, this dominance masked a critical dynamic: passive 401(k) flows were mechanically pushing these stocks higher regardless of fundamentals, while the rest of the market languished at historically cheap valuations.

The average US worker contributes $8,500 annually to a 401(k), with 71% allocated to equities—approximately $6,000 per person flowing into the stock market, much of it through passive index funds.

By late 2025, the valuation differential reached extremes. Based on the preferred EV/EBIT metric, the Russell 2000 small-cap index traded near its lowest level versus the Russell 1000 large-cap index in 25 years. This valuation chasm set the stage for a dramatic reversal.

Small Caps: The Comeback Story of 2025

The Russell 2000 hit an all-time high on December 10, 2025, reaching an intraday peak of 2,576.31. This marked the culmination of a 13.5% surge since August 2025, significantly outpacing the S&P 500's 6.9% gain over the same period. The primary catalyst? Federal Reserve rate cuts.

Why Small Caps Are Winning:

- Earnings Growth Acceleration: Small-cap earnings are projected to grow 22% in 2026 versus 15% for large caps

- Valuation Compression: Trading at historically low multiples relative to large caps, offering significant upside potential

- Domestic Focus: Less exposed to international trade tensions and tariff uncertainties that plague multinational corporations

The rotation from mega-cap tech to small caps represents one of the most attractive risk-reward opportunities in years. With valuations at 25-year lows relative to large caps and earnings growth accelerating, small caps are positioned for multi-year outperformance.

Part 2: The Emerging Markets Renaissance

Asia-Pacific: The New Growth Engine

Emerging markets ETFs posted their fourth-best month for inflows in November 2025, taking in over $7 billion. The rolling six-month flow figure reached near-record levels, signaling a fundamental shift in investor sentiment. What's driving this surge?

South Korea: The Semiconductor Powerhouse

South Korea's KOSPI surged 76% in 2025, posting its best annual performance since 1999 and outperforming all major global indices.

The Korean market's explosive performance was driven by several converging factors. Samsung Electronics and SK Hynix led the charge, benefiting from insatiable demand for AI-related semiconductors. Semiconductor exports reached all-time highs, with shipments growing 22% year-over-year. The country posted its largest trade surplus since 2017, reaching $709.7 billion in total exports.

Beyond semiconductors, Korea is experiencing broader-based growth:

- Defense & Aerospace: Companies like Hanwha Aerospace surged on military spending contracts, including a KRW 103 billion lunar lander propulsion system

- Corporate Reform: Government-led initiatives to narrow the 'Korean Discount' through stronger minority shareholder protections

- Shipbuilding Boom: Shipbuilding exports grew 25%, driven by global energy transition and LNG vessel demand

India: The Long-Term Structural Story

While India's Sensex experienced a 24% correction from its September highs, this pullback has created attractive entry points. The long-term structural drivers remain intact and compelling:

- Demographic Dividend: Young and growing population with expanding middle class

- Economic Growth: Projected 6-7% annual GDP growth over the next decade

- Supply Chain Shifts: Benefiting from companies diversifying away from China

- Valuation Reset: Price-to-earnings ratio now trading at one standard deviation below 10-year average versus S&P 500

Active EM fund positioning in India sits at the 0-1st percentile, suggesting institutional money is severely underweight. The recent correction has created what many analysts view as a compelling buying opportunity ahead of the anticipated 13-14% earnings growth in 2026-2027.

China and Hong Kong: The Stimulus-Driven Rally

Hong Kong's Hang Seng Index jumped 42% in 2025, while mainland China's CSI 300 gained 14%, marking a dramatic reversal from years of underperformance.

The Chinese market's resurgence was catalyzed by significant government stimulus packages and technological breakthroughs. The launch of DeepSeek's AI model—touted as a ChatGPT rival built for far less cost—reinvigorated faith in China's tech sector. Chinese investors responded enthusiastically, buying $2.9 billion worth of Hong Kong stocks in a single day in early 2025, the biggest purchase since 2021.

Key considerations for China exposure:

- Valuation Support: MSCI China trading at 11x forward P/E, cheap relative to history

- Strong Momentum: Price action and technical indicators showing sustained strength.

- Policy Support: Ongoing stimulus measures and regulatory reforms supporting market stability

Brazil and Latin America: Commodity-Driven Strength

Brazil's Bovespa surged 33% in 2025, benefiting from the global commodity upcycle and relatively high interest rates that attracted fixed income flows. The Brazilian market represents a unique combination of commodity exposure, high-yield bond opportunities, and equity upside.

Outlook for Korea and Brazil: While both markets have experienced strong rallies, expect consolidation rather than sharp corrections. Korea's semiconductor exposure and corporate reforms provide fundamental support, while Brazil's commodity-linked economy benefits from the ongoing energy transition and infrastructure buildout.

Part 3: Europe's Quiet Strength

The European Equity Renaissance

While emerging markets grabbed headlines, European indices delivered impressive returns that flew under many investors' radars. The performance was broad-based across major economies:

Index | 2025 Performance | Key Drivers |

Germany DAX | +19.7% | Defense stocks, industrial recovery, corporate governance |

UK FTSE 100 | +21.5% | Mining sector, retail strength, business activity expansion |

Italy FTSE MIB | +31.5% | Best year since 1998, banking sector strength |

France CAC 40 | +10.1% | Luxury goods, aerospace, financial services |

The European rally was supported by several converging factors. December seasonality proved particularly strong, with the DAX averaging a 2.18% return historically in December with a 73% win rate. The EURO STOXX 50 posted a 2.12% average return from mid-December through year-end, rising 76% of the time.

Key themes driving European strength:

- Defense Spending Boom: Russia-Ukraine tensions drove massive increases in defense budgets, with the EU signing off on a €150 billion arms fund

- Banking Sector: UK's Nationwide reporting 30% jump in annual profit, reflecting healthy mortgage and deposit growth.

- Investment Thesis: Europe offers a combination of reasonable valuations, improving fundamentals, and secular growth drivers in defense and industrial sectors. The DAX, CAC, and FTSE indices provide diversified exposure to global growth with lower correlation to US tech volatility.

Part 4: Commodities - The Silent Companion to Equity Liquidity

Commodities tend to move alongside global liquidity, not against it.

Current tailwinds include Infrastructure spending and supply-side constraints in metals and energy

For investors:

- Commodities act as inflation protection

- They diversify equity-heavy portfolios

- Liquidity flows here tend to be trend-driven and persistent

This is not a short-term trade — it’s a cycle-level allocation.

Part 5: Cryptocurrency's Institutional Maturation

From Speculation to Strategic Allocation

The cryptocurrency market underwent a fundamental transformation in 2025. What was once viewed as speculative fringe investing evolved into a legitimate institutional asset class. This shift was driven by regulatory clarity, infrastructure development, and unprecedented capital inflows.

The ETF Revolution

BlackRock's iShares Bitcoin Trust (IBIT) established itself as the dominant force, attracting nearly $100 billion in assets under management and controlling 61% of the Bitcoin ETF market. The success of spot Bitcoin ETFs marked what many consider the most significant product launch in cryptocurrency history.

Key institutional adoption metrics:

- ETF Flows: $16 billion in net inflows for Bitcoin spot ETFs, with total AUM rising 16% to $120 billion

- Digital Asset Treasuries: 196 public companies now hold Bitcoin, collectively raising $29 billion for crypto treasury purchases

- Institutional Share: 24.5% of Bitcoin ETF assets now held by institutional investors, up from previous years

- Stablecoin Growth: $46 trillion in annual stablecoin transactions, rivaling Visa and PayPal in payment volumes

Beyond Bitcoin: The Expanding Crypto Universe

While Bitcoin dominated headlines, the broader crypto ecosystem demonstrated significant maturation:

- Ethereum Integration: BlackRock and UBS using Ethereum for tokenized assets, bridging traditional finance and blockchain

- Infrastructure Development: Major fintechs like Circle, Robinhood, and Stripe developing blockchain payment rails

- Regulatory Progress: SEC streamlining approval process from 270 days to 75 days for crypto ETF products

- Real-World Assets: Tokenization of securities, commodities, and real estate gaining institutional traction

The Cautionary Note

Despite institutional validation, cryptocurrency remains highly volatile and correlates increasingly with risk assets rather than serving as a hedge. During the tariff crisis of April 2025, Bitcoin's correlation with the S&P 500 exceeded 0.80 while its correlation with gold declined to -0.75, demonstrating its behavior as a high-beta risk asset.

Investment Strategy: Positioning for the Next Cycle

The Core Thesis: Diversification and Rotation

The capital flow patterns of 2025 reveal a clear message: the era of concentrated mega-cap tech dominance is giving way to a broader, more diversified market environment. This creates both opportunities and imperatives for portfolio construction.

Sector-Specific Opportunities

Sector/Theme | Geographic Exposure |

Semiconductors & AI Infrastructure | South Korea (Samsung, SK Hynix), Taiwan |

& Aerospace | Europe (Germany, France), South Korea |

Commodities & Energy Transition | Brazil, diversified commodity indices |

Financial Services & Banking | Europe (UK, Italy), India |

E-commerce & Technology | India, China, select US small caps |

Industrial & Manufacturing | Germany (DAX), South Korea (shipbuilding) |

We will talk in depth around these sector-specific bets in our upcoming blogs.

Risk Management Considerations

While the rotation thesis is compelling, several risks warrant monitoring:

- Tariff Volatility: US trade policy remains unpredictable, with potential for renewed tariff escalation affecting export-dependent economies.

- AI Bubble Concerns: Semiconductor valuations vulnerable if AI adoption disappoints or competition intensifies.

- Currency Risk: Emerging market exposure carries currency volatility—consider hedged positions for large allocations.

- Geopolitical Tensions: China-Taiwan, Russia-Ukraine, and Middle East conflicts could disrupt market stability

Final Recommendations: Preparing for the Next Cycle

The liquidity flows of 2025 have established clear directional trends that are likely to persist into 2026 and beyond. The rotation away from concentrated mega-cap tech into broader market leadership represents a structural shift rather than a temporary phenomenon.

Key Takeaways:

Embrace the Rotation:

The Magnificent 7's dominance is waning as passive flows mechanically pushed valuations to unsustainable levels. Small caps, emerging markets, and European equities offer superior risk-reward at current valuations. Underweight concentrated tech exposure in favor of broader diversification.

Active Management Matters:

The dispersion in returns across geographies, sectors, and market capitalizations creates an ideal environment for active managers. Passive index exposure to small caps and emerging markets may underperform thoughtful security selection. Consider allocating to experienced active managers with regional expertise.

Advisors at Paasa can help you smartly allocate and diversify your portfolio.

The Bottom Line

Global capital is moving. The question isn't whether to participate in this rotation, but how to position portfolios to capture the opportunity while managing downside risks.

For investors willing to look beyond the familiar comfort of mega-cap tech, the next market cycle promises compelling returns. The liquidity is there. The fundamentals support the thesis. Now is the time to reposition.

About Paasa

Paasa is the platform used by global Indian Investors, NRIs, and family offices to diversify their wealth across global markets using equities, commodities, UCITS ETFs, are more.

What sets Paasa apart is its India-facing compliance layer:

- FEMA and LRS compliance embedded into every transaction.

- Tax reporting and analytics built for Indian investors (LTCG, STCG, dividend tax, TCS tracking).

- End-to-end support for remittance structuring, reconciliation, and compliance queries.

Whether it’s commodities, equities, UCITS funds, managed strategies, or even helping you protect your RSUs from estate tax, Paasa provides a single transparent platform for global portfolios with the confidence that India-specific compliance is taken care of.

Disclaimer

This article is intended for information only and does not constitute investment, tax, or legal advice. The material is based on public sources and our interpretation of current regulations, which may change. Investing in global markets entails risks, including currency risk, political risk, and market volatility. Past performance does not predict future outcomes. Please seek advice from qualified financial, tax, and legal professionals before acting.